Donor-Advised Funds (DAFs) in Canada offer a straightforward way to donate to charity while optimizing tax benefits. Here's what you need to know:

- What is a DAF? A DAF is a charitable account managed by a registered charity. You donate assets, get an immediate tax receipt, and recommend grants to charities over time.

- Tax Benefits: Contributions are eligible for federal and provincial tax credits, with a limit of 75% of your net income annually (unused credits can be carried forward for five years). Donating appreciated securities eliminates capital gains tax.

- Flexibility: DAFs allow you to donate during high-income years and decide on grants later, making them ideal for tax planning and legacy giving.

- Compliance: Grants must go to CRA-approved qualified donees. Sponsors retain control over fund disbursements, though donor recommendations are considered.

- Eligible Contributions: Cash, publicly traded securities, private company shares, ecologically sensitive land, and other assets can be donated, each with specific tax rules.

DAFs simplify structured giving while providing tax advantages and long-term impact. Ready to dive deeper? Let’s explore the details.

Tax Rules and Regulations for DAFs

Charitable Donation Tax Credit

When you contribute to a Donor-Advised Fund (DAF), you get an official tax receipt right away, even if you decide to distribute the funds later. The receipt reflects the eligible amount of your donation, which is the fair market value (FMV) of your gift minus any benefits you might receive in return.

This eligible amount qualifies for non-refundable tax credits at both the federal and provincial/territorial levels. You can claim donations up to 75% of your net income in a given year. If your contribution exceeds this limit, you can carry the unused portion forward for up to five years. This flexibility makes DAFs particularly helpful during years when your income is higher than usual. You can make a larger donation, claim the tax credits strategically over time, and recommend grants to charities at your own pace.

Here’s an important detail: if the benefit you receive is considered nominal - meaning it’s less than the lesser of 10% of the gift’s FMV or $75 - it does not reduce your eligible amount or affect the immediate tax receipt.

Next, let’s look at how donating appreciated assets can maximize tax advantages.

Capital Gains and Donations of Appreciated Assets

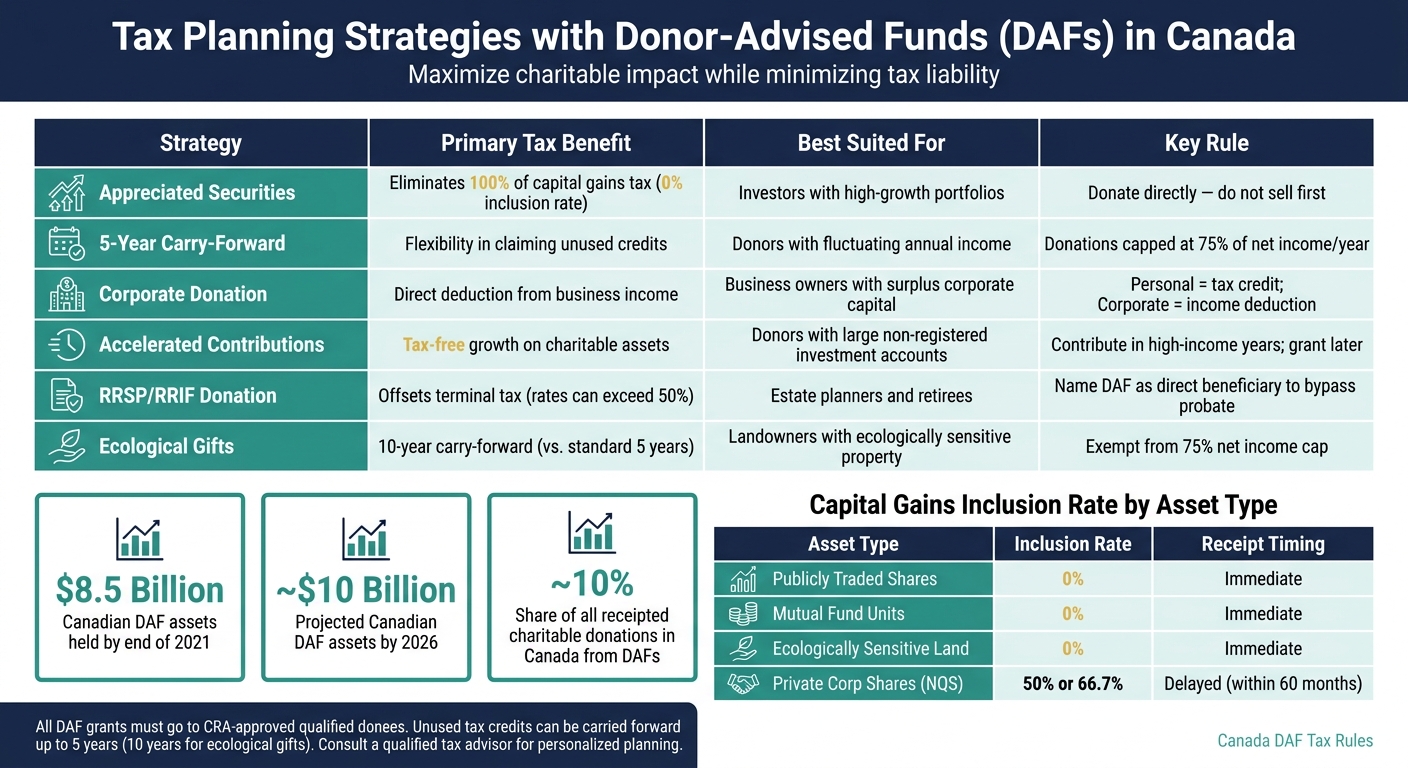

Donating appreciated assets directly to a DAF can be a smart tax move. If you contribute publicly traded securities - such as stocks, mutual fund units, or segregated fund interests - directly to the DAF, the capital gains inclusion rate drops to 0%. This means you won’t pay tax on the appreciation, but you’ll still receive a full tax receipt for the FMV of the securities at the time of the donation.

In contrast, selling securities first triggers capital gains tax at the standard inclusion rate (usually 50% or 66.7%), which reduces both your donation amount and the corresponding tax credit. Donating the assets directly is almost always the better choice.

| Asset Type | Capital Gains Inclusion Rate | Receipt Timing |

|---|---|---|

| Publicly Traded Shares | 0% | Immediate transfer |

| Mutual Fund Units | 0% | Immediate transfer |

| Private Corp Shares (Non-Qualifying) | Standard (50% or 66.7%) | Delayed until sold by charity |

| Ecologically Sensitive Land | 0% | Immediate transfer |

For private company shares, which are considered non-qualifying securities (NQS), the DAF sponsor typically cannot issue a tax receipt until the shares are sold or reclassified as qualifying securities. This must happen within 60 months of the donation. If you’re thinking about donating private shares, it’s best to consult a professional for tailored advice.

Now, let’s explore the rules governing how DAF sponsors manage their disbursements.

Disbursement Quota Rules for DAF Sponsors

DAF sponsors, which are usually registered as public foundations, must follow specific rules about how much they spend on charitable activities or grants each year. This is known as the disbursement quota (DQ).

The DQ is calculated based on the 24-month average value of non-charitable assets. The rates are as follows:

- 3.5% on the first $1 million of non-operational assets

- 5% on amounts above $1 million

This tiered system ensures that a significant portion of the funds is used actively for charitable purposes, rather than being held in long-term endowments. It also supports effective tax planning through DAFs.

Since 2022, DAF sponsors have been allowed to meet their DQ by granting funds to non-qualified donees. However, this requires rigorous due diligence and detailed documentation. Sponsors must maintain records that show the purpose of each grant and how the recipient used the funds.

sbb-itb-e9c03dd

Eligibility and Contribution Rules for Donors

Who Can Contribute to a DAF?

Knowing who can contribute to a Donor-Advised Fund (DAF) is crucial for taking full advantage of its tax benefits. In Canada, individuals, corporations, and estates are eligible to open and contribute to a DAF. Spouses can also contribute jointly. No additional registration is required, provided the minimum donation is met.

Once contributions are made, they are irrevocable. This means the assets are immediately transferred to the DAF sponsor. Donors, however, retain the ability to recommend grant recipients, shift their giving priorities over time, and even involve family members in their charitable activities. Tax lawyer St. John McCloskey of Clark Wilson LLP elaborates:

"While it's rare that a foundation wouldn't honour the recommendations of a donor, the fund is advised ‐ not directed ‐ by the donor."

Now, let’s examine the types of assets that can be donated.

Types of Eligible Contributions

DAFs accept a variety of assets, not just cash. Here’s a breakdown of common contribution types along with their associated tax and valuation guidelines:

| Contribution Type | Tax/Valuation Rule |

|---|---|

| Cash | The eligible amount is the cash value minus any advantage received. |

| Publicly Traded Securities | Zero per cent capital gains inclusion rate; valued at fair market value on the date of donation. |

| Private Company Shares | Requires detailed valuation and specialized tax planning. |

| Ecologically Sensitive Land | Not subject to the standard 75% net income cap; offers a 10-year carry-forward for tax credits. |

| Certified Cultural Property | Valued by the Canadian Cultural Property Export Review Board; no capital gains are applied. |

| Life Insurance/RRSP/RRIF | Can be donated through estate designation, with proceeds deemed a gift by the estate. |

For employee stock options, donating the shares within 30 days of exercising the options may qualify for an additional tax deduction. Timing is especially important in these cases.

Accurate valuation is critical to ensure the proper issuance of tax receipts.

Valuation and Receipting Requirements

Tax receipts are calculated based on the eligible amount of your gift, which is determined by the fair market value (FMV) of the donated property minus any advantage received. According to the CRA, FMV is defined as the highest price obtainable in an open market. This value plays a key role in determining donation limits and tax credits.

For non-cash gifts exceeding $1,000 in value, the CRA advises obtaining a professional, independent appraisal to establish FMV. For donations under $1,000, the charity itself may assess the value. The tax receipt must be issued to the legal owner of the asset at the time of the donation.

However, if the benefits received by the donor exceed 80% of the FMV, the CRA reserves the right to deny the tax receipt. In cases of estate donations, estates that qualify as a Graduated Rate Estate (GRE) may have the advantage of allocating tax credits across several tax years for added flexibility.

Philanthropy as a Strategy: Optimizing charitable giving and legacy building for HNW Canadians

Compliance and Grantmaking Restrictions

These compliance and grantmaking restrictions build upon the tax benefits and eligibility requirements, ensuring that Donor-Advised Fund (DAF) operations adhere to regulatory standards.

Donor Advisory Privileges and Legal Limits

When you contribute to a DAF, the funds are no longer under your legal control. Instead, the host foundation assumes ownership and control. Your role is limited to making non-binding recommendations, often referred to as "precatory" wishes. However, the foundation has the right to accept or reject these suggestions if they conflict with its charitable objectives or internal policies.

The Canada Revenue Agency (CRA) enforces strict rules: only the sponsoring organization can control how funds are disbursed. If you retain legal control over the funds, the donation is not eligible for a tax receipt.

Next, let’s explore the restrictions that apply to grantmaking, ensuring compliance with these regulations.

Grantmaking to Qualified Donees

CRA rules also impose strict conditions on who can receive grants. Generally, DAF grants can only be made to qualified donees, which include registered charities, Canadian amateur athletic associations, registered municipalities, and certain foreign universities. Donors cannot direct funds to individuals, family members, or entities that are not qualified organizations.

Grants that result in any personal benefit to the donor or their close associates are strictly prohibited. For instance, if a grant results in receiving something of value - such as event tickets or a membership - the eligible donation amount is reduced. If the advantage exceeds 80% of the fair market value, the donation may not qualify for a tax receipt at all.

In 2022, new legislation introduced the concept of "qualifying disbursements" to non-qualified donees (grantees). For grants exceeding $5,000 to non-qualified donees, written agreements and documented due diligence on risk factors are required.

| Risk Factor | Low Risk | High Risk |

|---|---|---|

| Grant Amount | Up to $5,000 | More than $50,000 |

| Grantee Track Record | Extensive | Newly established |

| Region | Inside Canada or stable | Conflict zone or unstable |

| Resource Type | Non-cash (e.g., textbooks) | Cash, cryptocurrency, or real property |

Cross-Border Giving Rules

Grantmaking beyond Canada introduces additional complexities. Foreign charities typically do not meet the Income Tax Act's definition of "qualified donees", meaning Canadian DAF sponsors cannot directly gift funds to U.S. or other foreign charities.

A notable 2025 Federal Court of Appeal case, Priority Foundation v. Canada (National Revenue), 2025 FCA 180, clarified this point. Justice Roussel stated:

"Article XXI of the Tax Convention did 'not operate to render a U.S. 501(c)(3) entity a "qualified donee" under the [ITA] for the purposes of allowing a Canadian registered charity to make a disbursement by way of gift to such an entity'."

For donors with U.S.-source income, the Canada–U.S. Tax Treaty provides some relief. You can claim a tax credit for gifts to U.S. charities, but only up to 75% of your net U.S.-source income reported on your Canadian tax return. Alternatively, you can donate to a Canadian-registered "Friends Of" organization, which acts as a qualified donee and channels funds to specific foreign entities.

Tax Planning with DAFs

Canada DAF Tax Strategies: Key Benefits & Rules at a Glance

Using DAFs for Long-Term Tax Efficiency

Donor-advised funds (DAFs) provide a flexible approach to tax planning, particularly when it comes to timing. One of their standout benefits is the ability to separate when you claim your tax deduction from when you actually distribute funds to charities. For instance, you could make a significant contribution in a high-income year - perhaps after selling a business or receiving a large bonus - claim the tax benefit right away, and then decide on charitable grants over the following years.

"A donor-advised fund separates the tax decision from the granting decision. You contribute now. Receive a donation receipt. Recommend grants later." - Shea Sanche, CFP, Founder, Insight Planning Wealth Management

The Canada Revenue Agency (CRA) allows you to carry forward unused charitable tax credits for up to five years. This is particularly useful if your donation exceeds 75% of your net income in a single year. For business owners, deciding whether to donate personally or through a corporation depends on where the funds are held and expected income levels. Personal donations result in non-refundable tax credits, while corporate donations provide a direct deduction from business income.

Another strategy involves donating appreciated securities directly. This approach eliminates capital gains tax and provides a full tax receipt. As noted earlier, this method can be a smart way to maximize the impact of your gift while minimizing taxes.

"Tax-efficient charitable giving in Canada is driven far more by asset selection, timing, and structure than by donation size." - Shea Sanche, Founder, Insight Planning

These tax strategies often work hand-in-hand with broader estate planning goals.

| Strategy | Primary Tax Benefit | Best Suited For |

|---|---|---|

| Appreciated Securities | Eliminates 100% of capital gains tax | Investors with high-growth portfolios |

| 5-Year Carry-Forward | Flexibility in claiming credits | Donors with fluctuating annual income |

| Corporate Donation | Direct deduction from business income | Business owners with surplus corporate capital |

| Accelerated Contributions | Tax-free growth on charitable assets | Donors with large non-registered investment accounts |

Estate Planning and Succession with DAFs

DAFs can also play a major role in reducing the tax burden on your estate. For example, RRSPs and RRIFs are fully taxable on the terminal return, with combined tax rates in some provinces exceeding 50% if the funds aren’t transferred to a spouse or dependent. Naming a DAF as the direct beneficiary of these plans allows you to bypass probate fees and offset terminal tax liabilities with a donation receipt.

If you’re withdrawing funds from an RRIF during your lifetime, filing CRA Form T1213 can help. This form eliminates the automatic 30% withholding tax on withdrawals over $20,000, ensuring the full amount is available for charitable contributions to your DAF. This strategy effectively converts taxable RRIF withdrawals into annual charitable donations.

"For clients who are genuinely philanthropic, the RRIF donation strategy is often the most tax-efficient, simple and direct way to convert future taxes into charitable capital." - Canada Gives

Additionally, donation limits are more favourable in the final tax years. Estates classified as a Graduated Rate Estate (GRE) gain added flexibility, as donations can be applied retroactively to the year of the gift, earlier years of the estate, or the deceased's final two tax returns.

Finding the Right Wealth Experts for DAF Planning

The complexity of DAF strategies means that expert advice is essential. Effective planning requires careful coordination of asset selection, timing, corporate structures, estate documents, and CRA compliance. Working with knowledgeable professionals ensures these elements come together seamlessly.

"DAFs can provide donors with a quicker way to attain their philanthropic and tax-planning goals, without the headache, time, or expense of establishing and operating a standalone charity." - Miller Thomson LLP

If you’re ready to explore DAF strategies, consider consulting specialists who can guide you through the process. Find Wealth Experts and Private Bankers in Canada offers a directory of professionals by province. Whether you need a tax advisor skilled in Form T1213 filings, a portfolio manager experienced in transferring securities in-kind, or an estate lawyer to integrate a DAF into your succession plan, this resource can help you connect with the right expertise in your area.

Conclusion

Key Points to Remember

Donor-advised funds (DAFs) offer a tax-smart and flexible way to give to charity. Here’s a quick recap of the essentials:

- Immediate tax receipts: You get a charitable tax receipt right away, even if grants are made later.

- Avoid capital gains tax: Donating appreciated securities directly to a DAF means no capital gains tax, with a 0% inclusion rate.

- Carry forward unused tax credits: If your donation exceeds 75% of your net income in a year, you can carry forward tax credits for up to five years (or 10 years for ecological gifts).

- Grants go to qualified donees only: All distributions must comply with Canada Revenue Agency (CRA) rules, and the sponsoring charity has the final say.

- Preserve your legacy: Appointing a successor advisor ensures your philanthropic goals continue.

By the end of 2021, Canadian DAFs held $8.5 billion in assets, with projections suggesting this could grow to $10 billion by 2026. DAF contributions now account for almost 10% of all receipted charitable donations in Canada. These figures highlight the growing role of DAFs in Canadian philanthropy.

Understanding these basics equips you to make informed decisions about your charitable giving strategy.

Next Steps for Donors

Now that you have the fundamentals, it’s time to seek expert advice. Planning a DAF involves navigating tax laws, investment strategies, estate planning, and CRA rules. Even small decisions can have a big financial impact.

"I tell them they have the opportunity to give back in a tax-efficient and creative way, that can also be something they share with their family, helps them create a legacy and makes them feel good." - Mary Hagerman, Senior Portfolio Manager and Wealth Adviser, Raymond James

If you’re ready to explore how a DAF could work for you, check out the Find Wealth Experts and Private Bankers in Canada directory. It’s a province-by-province guide to professionals who can help you choose the right DAF sponsor and integrate charitable giving into your broader financial and estate plans.

FAQs

When does a DAF donation receipt get issued?

When you contribute to a donor-advised fund (DAF), the DAF sponsor issues a donation receipt once they receive your gift. This receipt, which identifies the recipient as the legal donor, is usually provided within the timeline set by the organization - commonly by February 28 of the following year. It's a good idea to confirm the exact timing directly with your DAF sponsor.

Can I donate private company shares to a DAF?

Yes, it’s possible to donate private company shares to a donor-advised fund (DAF). However, these shares are usually categorized as non-qualifying securities and must satisfy specific conditions to be eligible for a donation receipt. For instance, the donation might need to qualify as an "excepted gift" and involve an arm’s length transaction with the qualified donee. Be sure to review Canadian tax regulations to understand the exact requirements.

How can I give to U.S. charities through a Canadian DAF?

If you're using a Canadian donor-advised fund (DAF), you can recommend grants to U.S. charities, but only if the charity qualifies as a qualified donee under Canadian regulations. This process has to align with both CRA and IRS rules. The U.S. charity must also meet the specific criteria required for cross-border giving. It's essential to ensure all regulations are followed to stay compliant.