Finding the right wealth advisor in Canada can feel overwhelming, especially if you have over $1 million in investable assets. Here's what you need to know:

- Who they are: Wealth advisors specialize in managing and preserving significant assets, offering tailored strategies for high-net-worth individuals.

- Types of advisors: Options include financial planners, investment advisors, portfolio managers, private bankers, and insurance advisors. Each serves different financial needs.

- Regulations: Advisors must be registered with provincial regulators or organizations like CIRO. Use tools like the CSA National Registration Search to verify credentials.

- Qualifications: Look for designations such as CFA, CFP, or TEP, which demonstrate expertise in areas like investment management or estate planning.

- Fees: Common fee models include asset-based fees (0.5%-1.5%), flat fees (~CA$10,000/year), hourly rates (CA$150–CA$400+), or commissions. Transparency is key - review annual fee reports.

- Services: High-net-worth services include tax planning, estate management, philanthropic strategies, and private banking.

- Finding the right fit: Evaluate experience, client fit, and communication style. Ensure they understand your goals and provide personalized advice.

Start by defining your financial goals, verifying credentials, and comparing advisors to find someone who aligns with your needs. Proper planning with the right advisor can lead to long-term financial success.

Stenner Wealth Partners+: For High Net-Worth Investors

sbb-itb-e9c03dd

Wealth Advisors in Canada: What You Need to Know

Choosing the right wealth advisor involves understanding their services and the regulations that govern their work. Here's a closer look at the different types of advisors and the oversight mechanisms in Canada.

Types of Wealth Advisors and What They Do

The term "financial advisor" is broad and applies to various roles in Canada, including those working at banks, as investment brokers, or as insurance agents.

- Financial planners: They create detailed plans for retirement, tax strategies, and estate planning.

- Investment advisors: Also called Registered Representatives, they focus on securities like stocks, bonds, and mutual funds, offering buy-and-sell guidance.

- Portfolio managers: These professionals have the authority to make investment decisions and execute trades for you without needing your approval for each action.

- Mutual fund dealers: Their expertise is limited to mutual funds and sometimes ETFs.

- Insurance advisors: They specialize in risk management products, such as life insurance, segregated funds, and annuities.

- Private bankers: Working for major Canadian banks, they cater to high-net-worth clients by combining banking, credit, and wealth management services. These services often require a minimum asset level of $1 million or more.

| Advisor Type | Primary Focus | Common Products |

|---|---|---|

| Financial Planner | Long-term goals, tax, estate | Financial plans, RRSPs, TFSAs |

| Investment Advisor | Security selection & monitoring | Stocks, bonds, ETFs, mutual funds |

| Portfolio Manager | Discretionary portfolio management | Full range of securities |

| Insurance Advisor | Risk management & estate | Life insurance, annuities, seg funds |

| Private Banker | Integrated banking & wealth services | GICs, RRSPs, TFSAs, credit solutions |

These roles operate under a strict regulatory framework to ensure investor protection.

How Wealth Advisors Are Regulated in Canada

Wealth advisors in Canada are subject to a multi-layered regulatory system involving both national and provincial authorities. The Canadian Investment Regulatory Organization (CIRO), created from the merger of the Investment Industry Regulatory Organization of Canada (IIROC) and the Mutual Fund Dealers Association of Canada (MFDA), oversees investment and mutual fund dealers. CIRO operates under the coordination of the Canadian Securities Administrators (CSA), which spans all provinces and territories. In Quebec, the Autorité des marchés financiers (AMF) manages securities and insurance oversight locally.

"In Canada, anyone trading securities or in the business of advising clients on securities must be registered with the provincial or territorial securities regulator, unless an exemption applies." - Canadian Securities Administrators

To ensure your advisor is properly licensed, use the CSA's National Registration Search tool. You can also consult CIRO's disciplined persons list to check for any past regulatory actions or complaints.

Title protection for wealth advisors can vary by province. For example, "Financial Planner" is a legally protected title requiring specific credentials in some regions, while in others, it can be used more freely. It's always a good idea to verify the qualifications behind any title, not just the title itself.

How to Evaluate an Advisor's Qualifications

Once you’ve familiarized yourself with the types of advisors and their regulatory frameworks, the next logical step is determining whether a specific advisor is equipped to handle your unique financial situation.

Key Designations for High-Net-Worth Advisors

Beyond regulations, an advisor’s qualifications play a significant role in their ability to manage high-net-worth portfolios. Each professional designation represents specific expertise, so it’s important to choose credentials that align with your financial needs rather than being impressed by a string of letters after someone’s name.

"The professional designations an advisor has earned reflect their skill set. To uphold their designations, advisors must fulfill certain ongoing education and training requirements." - iA Private Wealth

Here’s a breakdown of some of the most relevant designations in Canadian wealth management:

| Designation | Full Name | Primary Area of Expertise |

|---|---|---|

| CFA | Chartered Financial Analyst | Investment analysis and portfolio management |

| CFP | Certified Financial Planner | Comprehensive planning (tax, estate, retirement) |

| CIM | Chartered Investment Manager | Discretionary portfolio management |

| CSWP | Chartered Strategic Wealth Professional | High-net-worth wealth management |

| CLU | Chartered Life Underwriter | Estate planning and wealth transfer |

| TEP | Trust and Estate Practitioner | Trusts and estate planning |

| MTI | Estate and Trust Professional | Estate and trust management |

| CAIA | Chartered Alternative Investment Analyst | Private equity and alternative investments |

If your focus is on complex estate planning or business succession, a CFP or TEP would be a good fit. For advanced portfolio strategies or discretionary management, look for a CFA or CIM. Additionally, in Ontario, only those with credentials approved by the Financial Services Regulatory Authority (FSRA) can legally use the titles "Financial Advisor" or "Financial Planner" - a practice that’s expanding to other provinces.

Assessing Experience and Client Fit

An advisor’s credentials are just one part of the equation. You’ll also want to evaluate their experience working with clients in situations similar to yours - whether you’re a business owner planning a succession, managing cross-border assets, or overseeing multi-generational wealth.

Titles like "Senior Wealth Advisor" often signal years of experience and the management of substantial client portfolios, which is critical for high-net-worth individuals. At many Canadian firms, this title typically requires at least five years of experience and responsibility for managing over $40 million in client assets. However, since job titles aren’t standardized across the industry, it’s worth asking about the specific responsibilities tied to these roles.

To vet an advisor effectively, take these steps:

- Confirm their registration status using the CSA's National Registration Search.

- Check for any disciplinary actions.

- Ask how many clients they currently manage - an advisor with hundreds of accounts may struggle to provide personalized service.

- Request references from clients with similar financial profiles. Most reputable advisors will be happy to provide these.

"When it comes to ultra-high-net-worth wealth management in Canada, it's essential that you work with a firm with specialists who understand your situation and have helped similar individuals or families." - Tiffany Woodfield, TEP, Associate Portfolio Manager, SWAN Wealth Management

Understanding these qualifications sets the foundation for exploring fee structures and the personalized services that advisors offer.

Fee Structures and Services Explained

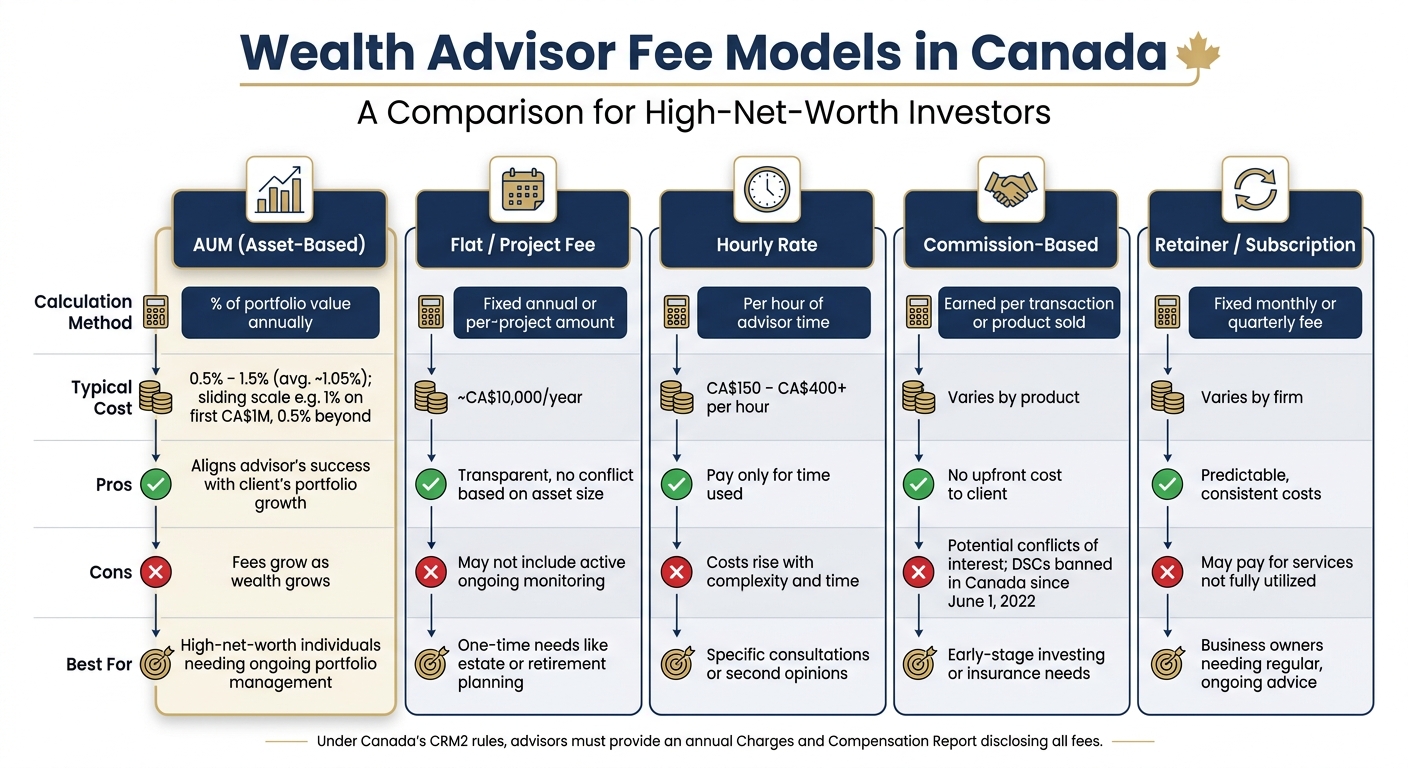

Wealth Advisor Fee Models in Canada: A Side-by-Side Comparison

Understanding how advisor fees work can help you avoid unexpected costs and evaluate the value of the services provided.

Common Fee Models in Canadian Wealth Management

In Canada, wealth management fees often follow an asset-based pricing model (AUM), where advisors charge between 0.5% and 1.5% of the assets they manage annually. On average, this fee is about 1.05%. Many advisors use a sliding scale, such as charging 1% on the first CA$1 million and 0.5% on amounts beyond that. This approach ties an advisor’s compensation to the growth of your portfolio, aligning their success with yours.

Other fee models cater to different needs. Flat fees, for instance, are often around CA$10,000 annually and cover comprehensive planning. Hourly rates, ranging from CA$150 to over CA$400 per hour, are better suited for one-time consultations or second opinions. Commission-based models, where advisors earn money per transaction, require caution due to potential conflicts of interest. It's also worth noting that deferred sales charges (DSCs) have been banned in Canada since 1 June 2022.

"Good advisors earn their compensation by providing significant value to clients." - iA Private Wealth

Here’s a quick breakdown of the most common fee models:

| Fee Model | Calculation Method | Pros/Cons | Best For |

|---|---|---|---|

| AUM (Asset-Based) | Percentage of portfolio (0.5%–1.5%) | Pros: Aligns interests. Cons: Fees increase with wealth growth. | High-net-worth individuals needing ongoing management. |

| Flat / Project Fee | Fixed amount (e.g., CA$10,000/year) | Pros: Transparent, no asset size conflict. Cons: No active monitoring. | One-time needs like estate or retirement planning. |

| Hourly Rate | Per hour (CA$150–CA$400+) | Pros: Pay only for time used. Cons: Costs rise with complexity. | Specific consultations or second opinions. |

| Commission-Based | Per transaction or product sale | Pros: No upfront cost. Cons: May lead to conflicts of interest. | Early-stage investing or insurance needs. |

| Retainer / Subscription | Fixed monthly or quarterly fee | Pros: Predictable costs. Cons: May pay for unused services. | Business owners needing regular advice. |

Thanks to Canada’s Client Relationship Model Phase 2 (CRM2) rules, advisors are required to provide an annual "Charges and Compensation Report" that details all fees and their allocation. Reviewing this report each year ensures you understand exactly what you're paying for.

Services Tailored to High-Net-Worth Individuals

For high-net-worth individuals, wealth management goes far beyond simply picking investments. Advisors often provide a suite of services designed to address every aspect of your financial life.

Key offerings include tax planning (such as strategies for capital gains optimization, income splitting, or cross-border compliance for U.S.-connected clients), estate and trust services (like creating family trusts, drafting complex wills, or offering executor support), and philanthropic strategies (including donor-advised funds or private foundations). For those with CA$30 million or more in assets, family office services are available, providing centralized management for everything from investments to administrative tasks like bill payments and record-keeping. Additionally, private banking services, often available through institutions like TD or RBC, provide access to high-value credit products and specialized lending for clients with at least CA$1 million in investable assets.

While many of these services are included in standard AUM fees, more intricate tasks - like setting up a private foundation or managing detailed cross-border tax issues - may incur additional charges. It’s always a good idea to confirm which services are covered and which might come with extra fees.

Investment Approach and Relationship Fit

After reviewing the fees and services offered by a financial advisor, the next step is to see if their investment philosophy and working style align with your personal goals and preferences. This is a crucial part of ensuring a productive and effective partnership.

Investment Philosophy and Portfolio Customization

A key question to ask is: “What is your approach to planning and portfolio construction?” The response can reveal a lot about how an advisor operates. A solid investment philosophy should go beyond generic advice and reflect how all aspects of your financial situation - like taxes and long-term objectives - are interconnected.

You’ll also need to decide between two main types of accounts: Advisory Accounts and Managed (Discretionary) Accounts. In an advisory account, the advisor provides recommendations, but you have the final say on every decision. In contrast, a managed account allows a registered Portfolio Manager to make decisions on your behalf, guided by your Investment Policy Statement (IPS). This document outlines your goals, risk tolerance, and any specific constraints. Keep in mind that some firms require a minimum of CA$250,000 to open a discretionary managed account.

For high-net-worth clients, a customized investment strategy becomes even more important. Look for advisors who use open architecture, meaning they can access investments across the entire market rather than being restricted to proprietary products. Tax-aware strategies, such as direct indexing and tax-loss harvesting, are particularly valuable given that combined federal-provincial marginal tax rates in Canada can exceed 53% for portfolios over CA$5 million. Additionally, access to alternative assets like private equity, private credit, and real estate signals a more tailored approach to wealth management.

"Good wealth planning isn't about offering oversimplified sound bites. It involves looking closely at your whole financial picture and how all the pieces connect, then developing coordinated, personalized strategies that fulfill your unique needs." - iA Private Wealth

But beyond the strategy itself, the way you collaborate and communicate with your advisor is just as critical.

Communication and Service Expectations

Regular and proactive communication is essential to keeping your financial plan on track, especially as your circumstances evolve. At a minimum, you should meet annually to review portfolio performance and reassess your goals. A great advisor won’t wait for you to reach out - they’ll initiate contact during significant market changes or other financial events.

From the start, establish how often you’d like updates, your preferred communication channels, and what success looks like for you. This could mean outperforming a benchmark or hitting a personal milestone, like reaching a specific retirement income. It’s also worth clarifying whether you’ll work with a single advisor or a broader team that includes specialists in areas like tax, estate, and investment planning.

Your engagement matters too. Keep your advisor informed about major life events - whether it’s starting a business, getting married, or receiving an inheritance - so they can adjust your plan accordingly. Under Canada's CRM2 rules, advisors must provide an annual report detailing charges and performance. With the upcoming CRM3 regulations, disclosure will go even further, requiring transparency on embedded fund costs such as Management Expense Ratios (MERs) and Trading Expense Ratios (TERs).

How to Find and Shortlist Wealth Advisors in Canada

Once you’ve figured out the type of services, fees, and working style you’re looking for in a wealth advisor, the next step is knowing where to search and how to narrow down your options. Taking a methodical approach ensures you start with the right regulatory and professional safeguards in place.

Where to Find Wealth Advisors

After you’ve evaluated the qualifications you’re looking for, use the Canadian Securities Administrators (CSA) tool to confirm an advisor's registration and check for any regulatory actions.

"In Canada, anyone trading securities or in the business of advising clients on securities must be registered with the provincial or territorial securities regulator." - Canadian Securities Administrators

Beyond the CSA, you can explore directories from organizations like FP Canada, Advocis, the Institute of Advanced Financial Planners (IAFP), and the Portfolio Management Association of Canada (PMAC). If you’re a high-net-worth individual, the privatebankers.ca directory is particularly useful. It lets you browse private wealth services by province, helping you find advisors with expertise in your specific region.

It’s also important to verify the advisor’s disciplinary history. You can do this through CIRO, CSA, or the Better Business Bureau (BBB). If you’re in Québec, check with the Autorité des marchés financiers (AMF). Ensuring the advisor has a clean regulatory record is a simple but crucial step.

How to Compare and Narrow Down Your Options

A two-stage process works best when narrowing down your list of potential advisors. Start with short phone or video calls with several candidates. These initial conversations help you get a feel for their background, professional designations, and overall approach. After this, select your top two or three choices for a more in-depth, 30-minute meeting to discuss your goals and assess compatibility.

During these meetings, ask about their experience, certifications like CFP or RFP, how they’re compensated, and how they approach client service. Request a sample of their CRM2 annual report, which outlines all charges and compensation. This report can give you a clear way to compare advisors. If they offer references, it’s worth reaching out to learn more about their long-term service and responsiveness. This process is essential for finding an advisor who aligns with your financial goals.

Conclusion

Picking the right wealth advisor is a major financial decision - possibly one of the most impactful you'll ever make. As iA Private Wealth aptly states:

"Choosing an Investment Advisor is one of most important long-term financial decisions you will make – perhaps even the most important."

To make an informed choice, start by defining your financial goals, understanding your risk tolerance, and deciding how involved you want to be in managing your finances. Next, verify the advisor's credentials, clarify how they are compensated, and review annual fee reports to ensure transparency.

But it’s not just about qualifications. The personal connection matters just as much. Look for someone who communicates effectively, asks the right questions, and works collaboratively with your accountant and lawyer. Research shows that Canadian investors who work with advisors tend to build much greater wealth over 15 years compared to those who manage their finances alone. However, this success depends on finding the right advisor - not just any advisor.

Taking a structured and thorough approach may take time, but it’s an investment that can yield long-term financial rewards.