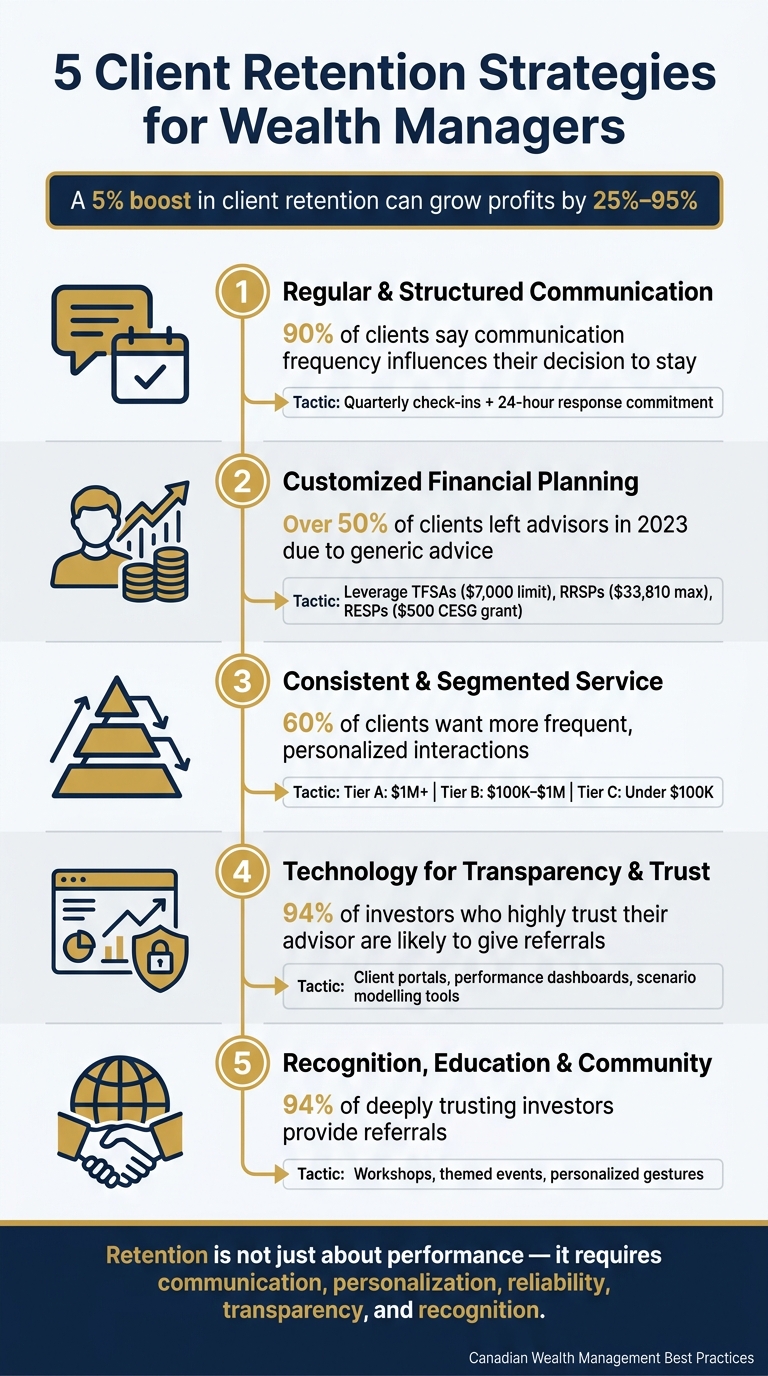

Client retention is critical for wealth managers in Canada. Building long-term relationships not only reduces costs but also increases profits - just a 5% boost in retention can grow profits by 25% to 95%. Here’s what matters most:

- Frequent and meaningful communication: 90% of clients value regular updates. Use structured schedules, personalized outreach, and digital tools like client portals to keep them engaged.

- Tailored financial advice: Over half of clients leave advisors due to generic advice. Address personal goals using tools like RRSPs, TFSAs, and RESPs for tax efficiency and retirement planning.

- Consistent service delivery: Segment clients into tiers and adapt services to their preferences. Trust builds when clients feel prioritized.

- Transparent use of technology: Tools like client portals and performance dashboards enhance clarity and trust while meeting privacy standards.

- Recognition and education: Personal touches, financial workshops, and community events strengthen loyalty and encourage referrals.

These strategies help wealth managers maintain strong client relationships, reduce turnover, and stand out in a competitive market.

5 Client Retention Strategies for Wealth Managers: Key Stats & Tactics

Advisors: Are You Losing Clients Without Knowing It? Here’s How to Stop It.

sbb-itb-e9c03dd

1. Regular and Structured Client Communication

How often you communicate with clients can make or break your relationship with them. In fact, nearly 90% of clients say the frequency and quality of communication influence their decision to stay with an advisor and provide referrals. This makes it clear: consistent and meaningful interaction is non-negotiable.

"Having annual portfolio reviews isn't going to cut it right now with most clients as they want to know that you've got their financial back." - Wealth Professional

To keep clients engaged, consider scheduling quarterly or bi-annual check-ins. Beyond these regular touchpoints, include personalized outreach for major life events like a business sale, inheritance, or retirement. During times of market turbulence, step up with proactive updates to help clients avoid emotional, spur-of-the-moment decisions.

A structured service calendar can be a game-changer here. It ensures clients know exactly when to expect portfolio reviews, tax planning reminders, and market updates throughout the year. This approach not only builds trust but also sets clear service milestones. Pairing this with standardized meeting agendas guarantees that every review is thorough and leaves clients with a solid understanding of their financial standing. Additionally, committing to a clear response time - such as answering client questions within 24 hours - further reinforces your reliability.

Leverage tools like client portals, newsletters, and mobile platforms to offer 24/7 access to portfolio performance. These digital solutions align perfectly with the expectations of high-net-worth clients. During onboarding, take the time to ask clients about their preferred communication frequency and channels. This ensures your approach matches their needs and complements the other retention strategies you'll explore later.

"People remember how you made them feel - before they remember how you managed their money." - Joey Hagner, GCG Advisory Partners

2. Customized Financial Planning and Advice

A cookie-cutter approach to financial advice just doesn’t cut it - clients want solutions that fit their unique situations. In fact, over half of advisory clients in 2023 reported leaving their advisors because the advice didn’t match their personal goals or needs. Offering tailored financial planning turns short-term transactions into meaningful, long-term relationships.

Personalized planning starts with understanding what truly matters to each client. This involves digging into their core financial motivations. Are they worried about saving for a child’s education? Planning an exit strategy for their business? Or perhaps focused on preserving wealth for future generations? These conversations reveal the emotional underpinnings that influence every financial decision they make.

As Theodore Roosevelt famously said:

"People don't care how much you know until they know how much you care." – Theodore Roosevelt

In Canada’s diverse financial environment, personalized strategies often involve leveraging tools like TFSAs, RRSPs, and RESPs to meet specific tax and retirement needs. For instance:

- A young professional might benefit from a TFSA (with a $7,000 limit in 2026) for tax-free growth and an RRSP (2026 maximum: $33,810) for immediate tax savings.

- Parents saving for their child’s education could use an RESP and contribute $2,500 annually to qualify for the $500 Canada Education Savings Grant (CESG).

- Those nearing retirement often need a well-thought-out RRSP decumulation strategy to minimize tax exposure for their household.

Consider a real-world example: In Fall 2025, Nancy Grouni of Objective Financial Partners helped Bonnie and Todd Kelly create an RRSP decumulation plan to optimize their tax situation before retiring in 2026. Similarly, in August 2025, Hannah McVean provided Faisal Dosani and his wife with a detailed retirement strategy, incorporating government programs and advanced planning techniques.

These customized plans not only help clients stay focused on their long-term goals but also reduce the likelihood of impulsive reactions to market volatility. When clients see how tools like TFSAs, RRSPs, or RESPs fit into a broader, personalized strategy, they’re more likely to stay the course - and less likely to leave their advisor.

For those looking to create tailored financial plans, working with experienced professionals can make all the difference. The Find Wealth Experts and Private Bankers in Canada directory connects you to experts across the country who can help craft strategies that truly resonate.

3. Consistent and Segmented Client Service

Delivering consistent service that aligns with client needs is just as important as offering tailored advice. Even the best-personalized strategies can fall flat if the service itself feels erratic. Studies show that nearly 90% of clients place a high value on how often they’re contacted. For high-net-worth (HNW) clients, dissatisfaction doesn’t usually stem from one poor quarter - it’s the gradual loss of trust over time. This happens when clients feel they’re treated more like a revenue source than individuals with unique goals.

The key to avoiding this erosion of confidence lies in effective segmentation. This approach goes beyond basic demographics, considering factors like life stage, risk tolerance, financial understanding, and communication preferences. For example, clients can be grouped into profiles such as:

- The Delegator: Prefers concise updates and minimal back-and-forth.

- The Validator: Values frequent communication and active involvement in decisions.

- The Tech-Savvy Client: Leans towards digital tools and asynchronous updates.

By tailoring your service approach to these profiles, interactions feel deliberate and meaningful rather than generic. This kind of segmentation not only personalizes the client experience but also strengthens long-term loyalty.

To put segmentation into action, a tiered service structure can help:

| Tier | Assets | Approach |

|---|---|---|

| Tier A (Platinum) | $1M+ (HNW/UHNW) | Quarterly meetings, proactive tax and estate planning, direct team access |

| Tier B (Gold) | $100K–$1M (Mass Affluent) | Semi-annual meetings, simplified planning, digital updates |

| Tier C (Silver) | Under $100K | Annual meetings, automated communications, standard models |

Kipp Cormier, Head of Financial Advisor Sales at Envestnet, explains the importance of this balance:

"Standardisation doesn't make service impersonal. It makes it dependable."

Consistency doesn’t end with segmentation - it’s also about listening to clients. Regular satisfaction surveys can help gauge whether your communication frequency meets expectations. Research shows that 60% of clients want more frequent, personalized interactions. Joe Buhrmann, Advisory Financial Planning Practice Management Consultant at eMoney Advisor, underscores the value of feedback:

"Use periodic surveys to gauge client satisfaction and make improvements based on their input. This will show your clients that you are committed to understanding and meeting their needs effectively and allow you to tailor your services to their preferences."

4. Using Technology to Build Transparency and Trust

Technology plays a key role in fostering trust by making services more transparent and accessible in real time. It doesn’t replace the personal touch of wealth management but complements it by enhancing visibility and reliability. Secure client portals, for example, allow clients to monitor their financial plans whenever they want, offering a layer of transparency that builds confidence. According to Statista Market Insights, clients increasingly expect "greater transparency and access to information, as well as digital tools and platforms that enable them to monitor and manage their investments more effectively". This shift towards digital tools not only reassures clients but also introduces innovative ways to provide clarity on their investments.

Data analytics tools take transparency a step further by turning reports into proactive guidance. A lack of transparency can hurt client retention, while trust has a direct impact on growth - 94% of investors who "highly trust" their advisor are likely to provide referrals. Platforms like Addepar simplify the process by consolidating public and private investment data into a single dashboard. Similarly, Orion Advisor Tech offers automated rebalancing and customizable performance reports through branded client portals. Tools like eMoney Advisor and RightCapital go even further, using scenario modelling to demonstrate how changes, such as adjusting savings rates or shifting asset allocations, might affect long-term goals. These tools make complex financial concepts easier to understand, strengthening the advisor-client relationship.

"Technology features like client portals and data analytics tools will help you upgrade your client experience and serve your clients better." - Joe Buhrmann, Advisory Financial Planning Practice Management Consultant, eMoney Advisor

While these digital advancements enhance the client experience, they must also meet rigorous data privacy standards. In Canada, regulatory expectations for investment counselling firms are set to increase by 2026, requiring a careful balance between adopting advanced tools and maintaining compliance. When implementing CRM platforms or automated reporting tools, it’s essential to ensure they are specifically designed for regulated, relationship-focused businesses. This involves obtaining informed consent for data collection, using secure and encrypted systems, and treating compliance as a core component rather than an afterthought. By doing so, firms can ensure their technology not only enhances service but also safeguards client trust.

To strengthen your digital approach while staying compliant with Canadian regulations, consider connecting with local experts through Find Wealth Experts and Private Bankers in Canada.

5. Client Recognition, Financial Education, and Community Building

Strengthening client loyalty goes beyond structured communication and tailored planning. It thrives on personal connections, meaningful education, and a sense of community.

While digital tools and regular check-ins are helpful, lasting relationships are built on genuine human interaction. Recognizing clients as individuals - not just account numbers - makes a huge difference. Small gestures like sending handwritten Thanksgiving cards, acknowledging milestones like a child’s graduation, or gifting a book that aligns with a client’s hobbies show that you’re paying attention. These thoughtful acts don’t cost much but signal that the relationship extends beyond quarterly reviews.

Providing financial education is another way to build trust. When clients understand the reasoning behind your recommendations, they’re more likely to stay engaged and confident in your advice. Hosting webinars, in-person workshops, or panel discussions featuring experts like CPAs or estate attorneys can add real value. Tailoring these sessions to address topics like family financial security or managing retirement during inflation can deepen their relevance. Combined with personal recognition, this approach helps transform professional relationships into lasting partnerships.

Creating a sense of community takes loyalty to another level. Instead of just hosting a standard client appreciation dinner, consider themed events like wine tastings, virtual Q&A sessions, or networking evenings. These shared experiences can strengthen bonds and foster a sense of belonging. Clients who feel part of a community are also more likely to refer others. In fact, 94% of investors who deeply trust their advisor are inclined to provide referrals. As Michael Featherman from WealthManagement.com notes:

"The HNW clients who stay... are staying because their advisor has become genuinely difficult to replace."

For those committed to a relationship-first approach, combining personalized communication with community-building efforts is key. Find Wealth Experts and Private Bankers in Canada can connect you with professionals who specialize in Canadian wealth management.

Conclusion

Retaining clients in wealth management hinges on consistent, thoughtful practices. The five strategies discussed in this article address different aspects of the client relationship: how often you communicate, how personalized your advice is, how dependable your service remains, how transparently you use technology, and how effectively you acknowledge and educate your clients. Together, these strategies create a strong foundation for lasting relationships.

The real strength of these approaches lies in their cumulative effect. Regular communication helps bridge gaps in expectations. Tailored financial advice shows clients they’re valued as individuals. Reliable, segmented service fosters trust. Technology enhances transparency and can even identify opportunities before clients inquire. Finally, recognizing clients and providing education elevates the relationship from purely professional to one that feels indispensable. As the Select Advisors Institute explains:

"Retention today isn't just about performance. Clients expect proactive communication, a clear planning process, coordinated tax strategy, and a consistently high-touch experience."

In 2023, over half of advisory clients switched providers, yet 94% of investors who deeply trust their advisor are likely to give referrals. These strategies - focused on communication, personalisation, reliability, transparency, and client recognition - are what set successful advisors apart.

For Canadian wealth managers operating in a competitive environment shaped by growing interest in holistic advice, ESG factors, and digital clarity, implementing these practices is critical. They separate thriving firms from those struggling to keep pace. To strengthen your client relationships or connect with experts, explore the Find Wealth Experts and Private Bankers in Canada directory, offering province-specific listings of Canadian wealth specialists.

FAQs

How do I set a client communication schedule that actually works?

Creating a solid communication schedule for your clients is all about finding the right mix of regularity and relevance. Start by setting up a timeline that works for each client - this could mean quarterly updates, semi-annual reviews, or something else that aligns with their preferences and needs.

Make sure every interaction counts. Be proactive in reaching out, listen carefully to what they have to say, and provide advice that’s tailored to their unique situation. Flexibility is also key - be ready to adjust your approach if circumstances change.

Use a variety of communication methods, like email, phone calls, or video meetings, to make sure you’re always easy to reach. When done consistently, this approach helps build trust and strengthens client loyalty over time.

What’s the easiest way to personalize advice with RRSPs, TFSAs, and RESPs?

The simplest way to tailor advice on RRSPs, TFSAs, and RESPs is by matching strategies to a client’s life stage, income, and goals. For example, TFSAs are perfect for flexible savings due to their tax-free growth, while RRSPs focus on deferring taxes, making them ideal for retirement planning. On the other hand, RESPs are specifically designed to help save for children’s education. By carefully evaluating each client’s financial situation, you can suggest the right contributions and investment options to meet their specific needs.

Which client portal features build the most trust without privacy risks?

Providing real-time access to financial data and transparent communication tools are key features of a client portal that can help establish trust. These tools keep clients informed and engaged, giving them confidence in the process while ensuring their sensitive information remains secure.