Wealthy Canadians often pay more in banking fees than necessary due to complex financial structures and scattered accounts. The good news? There are ways to significantly reduce these costs without sacrificing premium services. Here’s a quick summary of actionable strategies:

- Consolidate Accounts: Group assets across family members or businesses to meet fee waiver thresholds (e.g., $3–$5M in assets).

- Negotiate Fees: Request better rates on private banking, foreign exchange (FX), and corporate banking fees.

- Use Dual-Currency Accounts: Avoid high FX markups (2–3%) by maintaining CAD-USD accounts for cross-border needs.

- Leverage Technology: Automate cash flow with tools like QuickBooks or Wealthica, and use no-fee digital accounts for idle cash.

- Review Regularly: Conduct annual fee reviews with your banker to ensure all eligible waivers are applied.

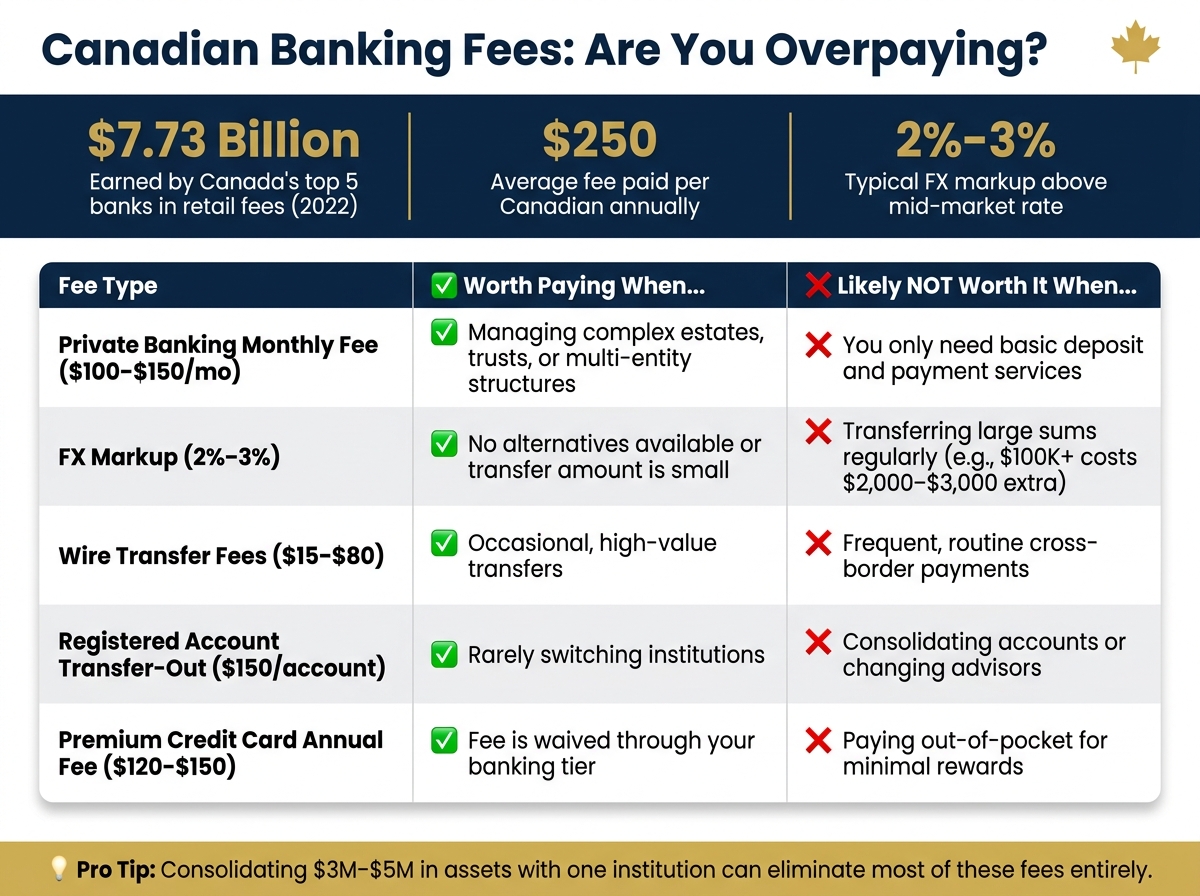

In 2022, Canada’s top banks earned $7.73 billion from retail fees, averaging $250 per Canadian. For high-net-worth individuals, private banking fees alone can range from $1,200–$1,800 annually, not including wealth management costs (0.5%–1.5% of assets). By restructuring your banking setup and using expert advice, you can cut unnecessary charges and maximize the value of your financial services.

REVEALED: The Shocking Truth About Private Banking Fees

sbb-itb-e9c03dd

Understanding High Banking Fees in Canada

Canadian Private Banking Fees: When to Pay vs. When to Negotiate

Common Types of Banking Fees

Canadians, especially those with significant wealth, often face a range of banking charges. The most noticeable is the monthly account fee, which can range from about $4 for a basic chequing account to $30 for a premium retail account. For private banking, these fees jump to around $100 to $150 per month. Yet, hidden charges can quietly drain even more money.

One major example is foreign exchange (FX) markups. Canadian banks typically add a 2% to 3% margin above the mid-market exchange rate for currency conversions. For instance, converting $100,000 could cost an extra $2,000 to $3,000 in hidden fees. Wire transfers further add to the expense: CIBC charges $30 for outgoing wires of up to $10,000, $50 for amounts between $10,000.01 and $50,000, and $80 for amounts above $50,000. RBC’s outgoing wire fees range from $15 to $45, with incoming wires costing up to $17.

Other less obvious charges include registered account transfer-out fees - both TD and RBC charge $150 per account when transferring an RRSP or TFSA to another institution. NSF (non-sufficient funds) fees, which range from $45 to $50 per occurrence, and wire investigation or recall fees of about $35 per request, also contribute to the overall cost.

"Canadian banks have done a very good job of extracting as many fees out of people as possible." - Alain de Bossart, Managing Director, North Economics

Next, let’s explore when these fees might actually deliver enough value to justify their cost.

When High Fees Are Worth Paying

Understanding the types of fees is one thing, but deciding whether they’re worth paying is another. The key is to evaluate whether the benefits you receive align with the costs.

Take private banking fees, for example. At $100 to $150 per month, these fees make sense if your financial needs are complex. For managing estates, trusts, holding companies, or cross-border assets, having a dedicated private banker can save time and help avoid costly mistakes.

"Private banking is most valuable for clients with complex financial affairs or for those that are looking for a dedicated banker to work with." - Christopher Liew, CFA, CFP®

Certain services, like customized credit structures, can also offset these fees. For example, Scotiabank’s Total Wealth Credit Solution offers preferred lending rates, which could save more in interest than the annual cost of private banking. Many private banking plans also include estate planning, tax strategies, and succession advice at no additional charge, potentially saving thousands in professional fees.

However, fees often lose their value in simpler situations. Paying a high monthly fee just to hold deposits or accepting a 2–3% FX markup on regular business transfers, when cheaper options exist, rarely makes sense. Here’s a quick breakdown of when fees are worth paying versus when they’re not:

| Fee Type | Worth Paying When... | Likely Not Worth It When... |

|---|---|---|

| Private banking monthly fee ($100–$150) | Managing complex estates, trusts, or multi-entity structures | You only need basic deposit and payment services |

| FX markup (2–3%) | No alternatives are available or the amount is small | Transferring large sums regularly |

| Wire transfer fees ($15–$80) | Occasional, high-value transfers | Frequent, routine cross-border payments |

| Registered account transfer-out ($150) | Rarely switching institutions | Consolidating accounts or changing advisors |

| Premium credit card annual fee | Fee is waived through your banking tier | You're paying it out-of-pocket for minimal rewards |

Strategies to Cut Banking Fees

When it comes to managing wealth effectively, minimizing banking fees is a smart move for affluent Canadians. Here's how you can take control of your banking costs.

Optimizing Account Structures

One of the simplest ways to reduce fees is by consolidating your assets. Many Canadian banks waive private banking fees once your investable assets reach a certain level - typically between $3 million and $5 million with the same institution. For example, Scotiabank reduces its $150 monthly fee by half for clients with $750,000 in investable assets.

Another useful tactic is grouping family assets under a single banking plan. This allows spouses, parents, or adult children to share fees rather than paying individually. If you own a professional corporation or holding company, ask your private banker to include those entities under your plan. Many banks will absorb corporate banking fees (often $20 or more per month) as part of their private banking packages.

Reducing Foreign Exchange and Cross-Border Costs

Foreign exchange fees can add up quickly, especially for those with cross-border financial activities. Retail FX markups at Canadian banks generally range from 2% to 3% above the mid-market rate. To avoid these costs, consider maintaining a CAD-USD dual-currency account. These accounts often include USD chequing and credit card services, eliminating the standard 2.5% foreign transaction fee on U.S.-dollar purchases.

For larger currency transfers, compare your bank's exchange rate with the mid-market rate, which you can easily find on Google or financial news platforms. If the markup seems excessive, negotiate for a preferred FX spread. Private banking clients often have the leverage to secure better rates, so it's worth bringing this up before making significant transfers.

Negotiating Banking Fees

Negotiation is a powerful yet underused tool. Private bankers often have flexibility when it comes to fee structures, especially if you consolidate more assets and services with their institution.

| What to Negotiate | Suggested Approach |

|---|---|

| Monthly private banking fee | Consolidate assets to meet waiver thresholds (typically $750K to $5M, depending on the bank) |

| Premium credit card annual fee | Request a waiver as part of your banking tier benefits |

| FX spreads on large transfers | Ask for a preferred rate, referencing your total relationship value with the bank |

| Corporate/holding company fees | Request these fees be bundled into your private banking package |

Don't forget to schedule an annual fee review with your private banker. Banks may not automatically apply all eligible waivers, so it's important to check. If you have significant credit facilities, such as a mortgage or line of credit with the same bank, use that as additional leverage to negotiate lower administrative and FX fees.

"Though expensive, private banking is often worth the price for individuals who demand a high degree of service, want ongoing professional advice for no extra charge and have their assets held in sophisticated structures that require professional management." – Frederick, Authoritative Source

Using Private Banking to Offset Fees

Private banking fees might seem hefty at first glance, but when used wisely, they can actually help you save on other costs.

Core Benefits of Private Banking

Private banking clients enjoy perks like better foreign exchange rates, lower borrowing costs, and waived annual credit card fees. On top of that, they get priority service, including access to a dedicated banker. For those with more complex financial needs, private banks offer tailored credit solutions using alternative collateral like investment portfolios, life insurance policies, and even luxury items such as yachts or aircraft. For example, CIBC Private Banking supports unique options like single-stock pledging, insurance-backed credit, and multi-currency liquidity solutions.

"We craft comprehensive personal and non-personal multi-currency liquidity solutions based on your short- and long-term needs." – Jonathan Hass, Managing Director and Head, CIBC Private Banking, Canada

This tailored approach helps reduce banking costs while maintaining the high level of service that high-net-worth individuals expect. However, these benefits come with specific entry requirements, which we’ll explore next.

Meeting Entry Thresholds

To access private banking in Canada, most of the Big Five banks require clients to have at least $1 million in investable assets or a total net worth of $3 million. For those with less liquid assets, alternative criteria might apply. For instance, TD Wealth allows clients to qualify with $2 million in total enterprise volume or $2.5 million in credit volume. This makes private banking an option for entrepreneurs and business owners who may not have large cash reserves.

While consolidating your assets with one institution can simplify your finances and reduce fees, it does come with risks, like limiting diversification. It’s worth weighing the savings against the potential downsides before deciding.

Here’s a quick look at how consolidating assets can unlock savings:

| Institution | Investable Assets Threshold | Alternative Qualification | Monthly Fee |

|---|---|---|---|

| RBC | $1,000,000+ | $3M+ net worth | ~$100 (rebate of $75 at $1M+) |

| TD | $1,000,000+ | $2M+ enterprise volume or $2.5M+ credit volume | ~$100 (waived at $3M–$5M) |

| Scotiabank | $750,000+ | Not specified | $150 (reduced to $75 at $750K+) |

Using Find Wealth Experts and Private Bankers in Canada

Once you understand the benefits and entry requirements, the next step is finding the right expert. Find Wealth Experts and Private Bankers in Canada is a free resource that lets you compare private bankers and wealth specialists by province. Whether you’re looking for help with cross-border planning, business succession, or custom credit solutions, this directory can help you make an informed choice before committing to a partnership.

Using Technology and Automation to Lower Costs

Private banking offers expert advice and tailored credit solutions to help reduce fees, but controlling daily costs often comes down to leveraging technology. Let’s explore how digital banking, automated cash management, and consolidated lending can make a real difference.

Digital Banking for High Balances

Traditional bank accounts don’t do much for your money, offering minimal interest on idle cash. In contrast, digital-first platforms like EQ Bank and Wealthsimple provide no-fee accounts with interest rates between 2.25% and 4.50%, far surpassing what most big banks offer. Wealthsimple even addresses deposit protection concerns with up to $1 million in CDIC coverage for clients holding $500,000 or more in assets.

A smart approach is to use no-fee digital accounts for operational cash to earn competitive interest rates, while relying on private banking for more complex needs like credit management, preferred FX rates, and investment solutions. These two strategies can complement each other seamlessly.

Thanks to Canada's Consumer-Driven Banking Framework, introduced in 2026, Open Banking now allows you to securely link accounts across multiple institutions. This means you can manage all your financial relationships through one easy-to-use interface.

"Fintechs have shown what a fairer, faster system can deliver for Canadians: fewer and lower fees, the ability to move money faster and more transparency." – Andrew Chau, Co-founder and CEO, Neo Financial

Automated Cash-Flow Management

Small fees can pile up quickly, even with recent changes. For example, non-sufficient funds (NSF) fees are capped at $10 as of March 2026, but avoiding them entirely is still the best strategy. Setting up $100 low-balance alerts and automated sweeps can help prevent overdrafts while moving idle cash into high-interest sub-accounts.

If you’re juggling business and personal finances, linking your banking platform to accounting software like QuickBooks or Xero via API can simplify real-time cash flow management. Automated payment scheduling through these tools can also help you capture early-payment discounts. Missing a 2% discount on a $10,000 invoice costs $200 - and if you miss five such discounts a month, that’s $12,000 annually.

Consolidating Credit Cards and Lending

Streamlining your credit cards and lending under a single private banking relationship is one of the easiest ways to cut fees. Many Canadian private banks waive annual fees on multiple premium credit cards, and sometimes extend those waivers to family members, once your assets meet their required threshold.

Private banking also offers access to portfolio-secured lines of credit, which come with lower interest rates compared to unsecured loans. Tools like Wealthica, a free Canadian aggregator, let you monitor your assets and liabilities across institutions in real time. This ensures you have a clear understanding of your borrowing costs before making financial decisions.

If you’re planning to consolidate accounts or shift lending, don’t forget to review automatic payments and direct deposits beforehand. Transfer-out fees for registered accounts like RRSPs and TFSAs have climbed to about $150 per account at major banks in 2025/2026. A little preparation can help you sidestep these unnecessary costs.

Building a Personal Fee Reduction Plan

Reviewing Current Banking Costs

The first step in cutting down on banking fees is taking a close look at what you're currently paying. Gather statements from all your accounts - personal chequing, savings, investment accounts, holding companies, and family trusts. Add up monthly service fees, credit card annual fees, wire transfer charges, and foreign exchange spreads. These costs can quietly accumulate, potentially reaching thousands of dollars annually.

Once you’ve calculated your total fees, compare them to the fee waiver thresholds at your bank. If you’re close to meeting those thresholds, consider consolidating assets to eliminate unnecessary charges. With this information, you’ll be better equipped to rethink how your banking arrangements are structured.

Restructuring Banking Relationships

After identifying your fees, it’s time to decide how to streamline your banking relationships. Consolidating your assets with a single private banking partner can help you qualify for fee waivers and better pricing. One strategy to explore is household grouping. Some private banking plans allow families - including parents, spouses, or adult children - to share monthly fees, which can spread the cost while giving everyone access to premium benefits.

Additionally, check whether your banking package includes waivers for business account fees (which can exceed CA$20 per month) and premium credit card annual fees, which often range from CA$120 to CA$150 per card.

"Though expensive, private banking is often worth the price for individuals who demand a high degree of service, want ongoing professional advice for no extra charge and have their assets held in sophisticated structures that require professional management." - Frederick, Expert cited in Genymoney.ca

Working with Experts to Cut Costs

Once your banking relationships are streamlined, the next step is to leverage expert support. Choose a private banker who works with a team of specialists, such as tax planners, estate experts, and investment advisors. Look for professionals with designations like CFA (Chartered Financial Analyst) or CFP (Certified Financial Planner).

A skilled private banker does more than manage your accounts. They can negotiate lower mortgage and loan rates, secure preferred foreign exchange pricing, and waive fees for services like wire transfers and safety deposit boxes.

If you’re unsure where to begin, check out the directory at Find Wealth Experts and Private Bankers in Canada (privatebankers.ca). This resource connects you with vetted private banking professionals across provinces, helping you find someone who understands the unique needs of high-net-worth Canadians.

Conclusion

Banking fees in Canada can add up to thousands of dollars each year. For wealthier Canadians, the financial impact can be even more substantial. In fact, in 2022, the five largest banks in Canada collectively earned CA$7.73 billion in extra non-interest profit, which works out to an average of CA$250 per Canadian.

But here’s the good news: there are practical ways to cut or even eliminate these fees. For instance, maintaining asset levels between CA$3–5 million can waive monthly fees. Pair this with comprehensive tax, estate, and succession planning, and you can significantly enhance the value of private banking vs traditional banking services.

Experts also stress the importance of leveraging technology and expertise:

"As we look towards 2030, the emphasis on personalized data-driven portfolio allocation remains critical. Canadian wealth managers who harness technology and multi-disciplinary expertise... will lead in delivering sustainable client success." - Andrew Borysenko, Wealth Manager and Portfolio Strategist

To stay ahead, working with knowledgeable professionals is essential. The directory at Find Wealth Experts and Private Bankers in Canada (privatebankers.ca) is a valuable resource, connecting you with experienced private bankers and wealth managers who understand the unique financial challenges faced by high-net-worth individuals in Canada.

FAQs

How do I know if private banking fees are worth it for me?

Private banking fees can make sense if your net worth exceeds $3 million or if you have intricate financial needs, such as estate planning, tax strategies, or managing investments. The fees, which usually fall between 0.5% and 1.5% of your assets each year, might be worth it if the tailored advice, convenience, and expert guidance align with your financial goals. Take time to evaluate your priorities and speak with a private banker to determine if it’s the right fit for you.

What should I ask my banker to waive or discount?

It's worth having a conversation with your banker to see if some fees can be reduced or even waived. These could include account maintenance charges, transaction fees, foreign exchange markups, or minimum balance penalties. If you're using private banking services, you might also want to ask about custom fee structures or discounts based on your assets or the strength of your banking relationship.

The key here is to be direct. If you manage significant assets or have a more complex financial setup, banks are often open to negotiating fees. It never hurts to ask!

How can I cut FX costs on CAD–USD transfers?

If you're looking to cut down on FX costs for CAD–USD transfers, there are a few strategies worth considering. Multi-currency accounts and zero-FX corporate cards can help reduce unnecessary fees. Some platforms also let you lock in favourable exchange rates or offer little to no FX markups, which can make a big difference over time.

For larger transfers - say, amounts over $100,000 CAD - you might even qualify for waived fees, which adds up to even greater savings. The key is to focus on transparent, cost-efficient options that give you the most bang for your buck.