Private credit is gaining traction in Canada, offering higher yields than traditional fixed-income products like GICs or public corporate bonds. This asset class involves loans directly negotiated between lenders and businesses, bypassing public markets. It appeals to high-net-worth Canadians and institutions like pension funds for its portfolio diversification and income potential. However, it comes with risks such as liquidity mismatches, sector concentration, and valuation opacity. Canadian investors are increasingly allocating 10–25% of their portfolios to private markets, with private credit playing a key role. To navigate this complex space, due diligence and professional advice from private bankers in Alberta or other regions is essential.

Key Points:

- Growth Drivers: Stricter bank regulations post-2008, demand for higher yields, and floating-rate loans.

- Market Size: Canadian private credit managers oversee $20–30B, while institutions hold $180B.

- Strategies: Direct lending, asset-based finance, and infrastructure credit are popular.

- Risks: Liquidity issues, opaque valuations, and sector-specific vulnerabilities.

- Investor Access: Through closed-end funds, evergreen funds, and interval funds, often tailored for RRSP or TFSA eligibility.

Private credit has evolved into a mainstream component of diversified portfolios, but careful planning and expert guidance are crucial for success.

Cross-border investment strategies in private credit with Fernando Martinez, IMCO

sbb-itb-e9c03dd

Key Growth Drivers and Market Trends

Canadian Private Credit Market: Key Stats & Growth Trends 2025

Global and Canadian Market Growth

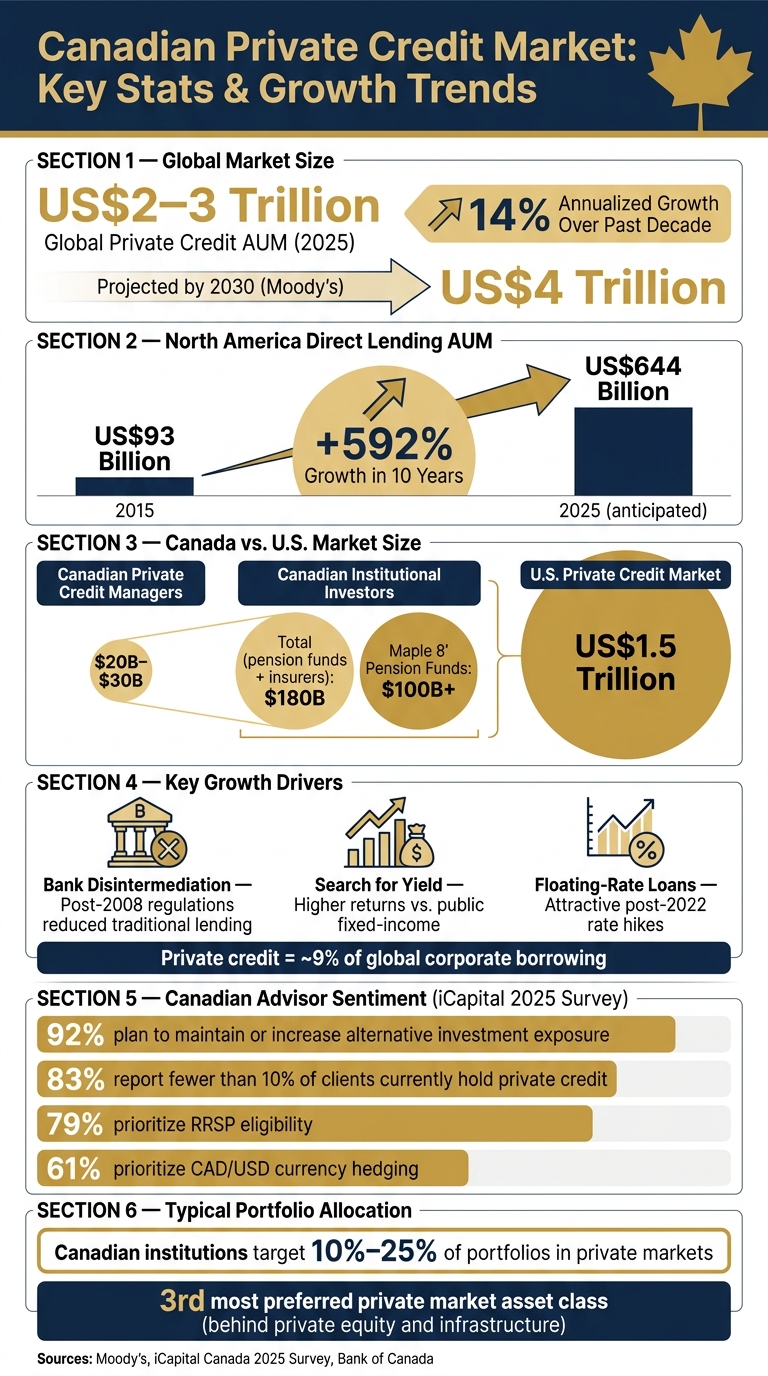

Over the past decade, private credit assets under management (AUM) globally have grown at an annualized rate of about 14%, reaching an estimated value of US$2–3 trillion. In North America, direct lending AUM soared from US$93 billion in 2015 to an anticipated US$644 billion by the end of 2025. Looking further ahead, Moody's predicts that global private credit could climb to nearly US$4 trillion by 2030, fuelled by increasing financing demands and a shift toward asset-backed lending.

"Private credit AUM is set for explosive expansion - potentially nearing $4 trillion by 2030 - driven by surging global financing needs [and] a structural shift toward asset‑backed lending." - Moody's

In Canada, the private credit market remains relatively small compared to its U.S. counterpart. Canadian private credit managers currently oversee between $20 billion and $30 billion, a fraction of the US$1.5 trillion U.S. market. However, Canadian institutional investors, including pension funds and life insurers, hold an estimated $180 billion in private credit. Notably, the "Maple 8" pension funds account for more than $100 billion of this total as of 2025.

These figures highlight the broader forces shaping the growth of private credit globally and within Canada.

Macro Drivers Behind Private Credit Growth

Several key factors have driven the global expansion of private credit. First, bank disintermediation has played a major role. After the 2008 financial crisis, stricter banking regulations led traditional lenders to pull back from certain markets, creating opportunities for non-bank lenders. Second, the search for yield has attracted investors to private credit, which often provides higher returns than public fixed-income products. Finally, floating-rate loans have gained appeal. Many private credit loans have variable interest rates, which became especially attractive following interest rate hikes after 2022. Today, private credit represents about 9% of corporate borrowing worldwide, marking its transition from a niche product to a key funding source.

Let’s now turn to developments specific to Canada’s private credit landscape.

Canadian-Specific Developments

Canada’s private credit market has grown steadily but at a more measured pace compared to the U.S., partly due to the stability of its domestic banking system. Unlike the U.S., where retail demand spurred rapid growth post-2008, Canada’s expansion has been largely driven by institutional players.

A notable example of this institutional activity occurred in February 2026, when pension giants OMERS and BCI acquired a US$1.4 billion portfolio of Blue Owl loans at 99.7 cents on the dollar. This transaction reflects the disciplined, large-scale investment strategies typical of Canadian institutions. At the same time, the iCapital Canada 2025 Private Markets Survey revealed that 92% of wealth managers plan to either maintain or increase their exposure to alternative investments. This underscores private credit's growing role in institutional portfolios.

As the market matures, the emphasis has shifted from rapid growth to creating stable and defensible allocations. Institutions now typically aim for private markets to make up 10% to 25% of their portfolios. While private credit was once the leading alternative asset class in Canada, it now ranks third behind private equity and infrastructure. This shift reflects its evolution into a standard component of diversified portfolios.

"Private credit – it's certainly present in Canada. It hasn't grown as rapidly in Canada as it has in some other places, but it's certainly something to keep an eye on." - Tiff Macklem, Governor, Bank of Canada

Private Credit Strategies and Structures

Main Private Credit Strategies

Private credit strategies come in various forms, each offering a unique balance of risk and return. This variety is one reason why the asset class appeals to so many Canadian investors. Building a diversified portfolio often involves combining multiple strategies to spread risk and enhance potential returns.

Direct lending is the most widely used strategy. It involves providing senior secured loans directly to mid-market businesses, bypassing traditional banks. With interest rates levelling out, returns in this category have settled into the high-single-digit range, a shift from the higher returns seen previously. In Canada, direct lending portfolios often focus on multi-tenant real estate borrowers, which sets them apart from their U.S. counterparts.

Asset-based finance (ABF) and specialty finance focus on lending against specific assets like aircraft, auto loans, or mortgages instead of relying on a company's general cash flows. This approach can offer a layer of protection during economic slowdowns. On the other hand, mezzanine and hybrid debt instruments are positioned lower in the capital structure than senior loans. While they carry more risk, they also offer the possibility of higher yields.

A growing area of interest in Canada is infrastructure and energy credit, particularly projects involving Indigenous equity partnerships. For example, in May 2025, the Canada Indigenous Loan Guarantee Corporation backed a $400 million guarantee to assist 36 First Nations in acquiring a 12.5% stake in Enbridge's Westcoast natural gas pipeline. This transaction, valued at approximately $715 million, highlights the increasing relevance of such investments.

These strategies are accessed through various investment structures, each with its own set of benefits and considerations.

Investment Structures for Canadian Investors

The way investors access private credit plays a key role in determining factors like liquidity, tax implications, and currency exposure. Here's a breakdown of common structures:

| Structure | Liquidity | Primary Investor Base | Key Feature |

|---|---|---|---|

| Closed-End (Vintage) Fund | Illiquid (7–10+ years) | Institutional | Long-term capital, no redemption risk |

| Evergreen Fund | Semi-liquid (periodic) | Wealth management | Continuous deployment, potential for gating |

| Interval Fund | Scheduled (quarterly/semi-annual) | Retail/wealth | Rule-based, systematic liquidity |

| Business Development Company (BDC) | Quarterly/publicly traded | Retail | High transparency, use of leverage |

Among these, evergreen funds have gained traction in the Canadian wealth management space. They allow investors to enter and exit periodically rather than locking up their capital for a fixed term. For instance, RBC Phillips Hager & North Investment Counsel uses three perpetual BDCs - Oaktree Strategic Credit Trust (OSCT), Blue Owl Credit Income Trust (BOCIT), and Blackstone Private Credit Fund (BCRED) - to provide private credit access. Meanwhile, interval funds offer a more structured option with systematic, rule-based liquidity.

For Canadian retail investors, two essential features are registered account eligibility and CAD‑denominated or hedged share classes. These reflect Canada's regulatory and currency-specific needs. Notably, 79% of Canadian advisors prioritize RRSP eligibility, and 61% consider CAD/USD currency hedging a key factor.

Building a Diversified Private Credit Portfolio

Once you understand the strategies and structures, the next step is integrating them into a diversified portfolio effectively.

Canadian wealth managers generally allocate 10% to 25% of a portfolio to private markets, with private credit forming a key component alongside private equity and infrastructure. This allocation reflects private credit's established role in Canadian investment strategies.

When it comes to manager selection, 54% of Canadian advisors prefer working with two managers per asset class, striking a balance between diversification and administrative simplicity. Leading global managers like Blackstone, KKR, and Brookfield are often favoured for their strong governance and operational expertise. Key indicators of portfolio health include the percentage of non-accrual loans (loans where borrowers have stopped payments) and payment-in-kind (PIK) notes (which defer interest payments rather than paying them in cash).

"Private credit is a legitimate and attractive asset class - if you play it well and play it smartly. It's not attractive if you lose half your capital." - Sean O'Hara, Chief Investment Strategist, Obsiido Alternative Investments Inc.

Experts recommend blending direct lending with ABF to mitigate concentration risk across different credit cycles. Additionally, dedicating at least 15 to 20 hours of due diligence to any specific strategy before investing is considered essential for navigating this complex asset class.

Risks, Regulation, and Due Diligence

Main Risks in Private Credit

Private credit offers attractive returns but comes with specific risks that Canadian investors need to understand before committing their capital.

One of the biggest challenges is liquidity mismatch. Many funds aimed at retail investors allow periodic redemptions, but the loans they invest in are illiquid. When too many investors request withdrawals at once, funds may impose restrictions or delays - known as "gating." Cases like Bridging Finance, Romspen, and Cortland in Canada highlight how single-name concentration can lead to such redemption halts. To manage this, most funds limit quarterly withdrawals to 5% of net asset value (NAV) to avoid forced asset sales.

Another concern is valuation opacity. Unlike publicly traded loans, private loans are valued internally and typically updated only quarterly. This lack of transparency can hide declining credit quality, especially during periods of market stress. For context, public credit funds holding similar assets have sometimes been valued 30% to 50% lower than their private counterparts.

Sector concentration is another risk to watch. Around 20% of private credit portfolios are tied to software companies, a sector that could face challenges from AI-driven disruption. While default rates in private credit generally range between 1% and 3%, "shadow defaults" - where unpaid interest is quietly added to the loan principal instead of being declared - are becoming a growing concern. These can obscure the true financial health of a portfolio.

| Risk Factor | What It Means | Why It Matters in Canada |

|---|---|---|

| Liquidity Mismatch | Fund redemption terms don't align with loan maturities | Can lead to gating and limited withdrawals |

| Valuation Opacity | Internally priced assets updated quarterly | May hide losses and create outdated valuations |

| Sector Concentration | Heavy exposure to software/tech sectors | Could be impacted by AI-related disruptions |

| Shadow Defaults | Unpaid interest added to principal | Masks borrower distress from investors |

Regulatory and Systemic Considerations

These risks underline the need for strong regulatory frameworks. Both the Bank of Canada and the Office of the Superintendent of Financial Institutions (OSFI) have identified private credit as a key risk to Canada’s financial stability in their 2026 outlooks.

"The issue is not private credit itself. It's how private credit will behave under stress." - Tiff Macklem, Governor, Bank of Canada

"A risk can be material and growing without being system-threatening." - Cory Harding, Spokesperson, OSFI

A significant concern is the close ties between private lenders and regulated banks, which include lending arrangements, warehousing, and risk transfers. Private credit accounts for about 5% of the consolidated loan portfolios of Canada’s "Big Six" banks. Stress in private credit markets could, therefore, have ripple effects across the broader financial system. However, the Financial Stability Board (FSB) raised concerns in May 2026 about Canada’s lack of detailed data compared to the U.S. and U.K., making it harder for regulators to oversee this growing market.

On the legal front, Canada has made notable changes. As of January 1, 2025, the criminal interest rate was reduced from an effective annual rate (EAR) of 60% to 35% APR. While this does not apply to commercial loans over $500,000 for business purposes, it has prompted lenders focusing on high-yield and distressed debt to adjust their pricing models. Additionally, amendments to the Investment Canada Act in March 2025 expanded national security reviews to include minority investments and asset acquisitions, which has implications for foreign-backed private credit funds engaged in equity-linked financing.

Due Diligence Best Practices

Navigating these risks requires solid due diligence, which is essential for Canadian investors considering private credit.

The first priority is manager selection. The gap in performance between top- and bottom-tier managers in private credit is significant, particularly during periods of market stress. Look for managers with experience across multiple credit cycles, a disciplined approach to underwriting, and conservative use of leverage.

Equally important is analysing the underlying loan characteristics. Investors should examine where loans are positioned in the capital structure, the quality of collateral, the strength of legal covenants, and the level of leverage employed. Keep an eye on rising non-accrual rates and payment-in-kind (PIK) notes, which can signal portfolio stress. On average, cash inflows from maturing loans and prepayments provide a natural liquidity buffer of 5% to 6% per quarter, which can help during periods of high redemption demand.

Canadian investors should also take two practical steps: confirm whether the fund is eligible for registered accounts like RRSPs or TFSAs and check if it offers a CAD-denominated or hedged share class. These factors are crucial, as 79% of Canadian advisors consider RRSP eligibility essential, and 61% prioritize CAD/USD currency hedging.

"Investors want both the upside from the illiquidity, and they want the yield premium. You have to pick one." - Philipp Soummer, Manager, Chronicle Wealth

Integrating Private Credit into Canadian Portfolios

How Private Credit Fits into Wealth Portfolios

Adding private credit to a portfolio can improve its overall stability and income potential. With all-in yields averaging around 10% and a standard deviation of 2.8% from 2010 to 2023 - compared to 8.1% for high-yield bonds and 8.2% for U.S. 10-year Treasuries - it offers a smoother alternative to many fixed-income investments.

"Private credit and other alternative investments help to smooth out returns over the long run because they are less correlated to traditional equity and fixed income products." - John Wilson, Co-CEO, Ninepoint Partners

Private credit's appeal grows further when considering Asset-Based Finance (ABF). These loans, secured by assets like mortgages or auto loans, provide diversification since they are less dependent on corporate earnings cycles than traditional corporate credit. For Canadians already invested in equities and government bonds, this low correlation makes private credit a strong stabilizer, contributing to a well-rounded portfolio.

Allocation Approaches for Canadian Investors

Wealth managers in Canada are increasingly recommending private market exposure in the range of 10% to 25%. However, retail investors are still catching up; 83% of Canadian advisors report that fewer than 10% of their clients currently hold private credit investments.

Practical considerations, like currency exposure, play a big role in allocation decisions. Most private credit funds are denominated in U.S. dollars, leading 61% of Canadian advisors to prioritize CAD/USD hedging. Using hedged share classes can protect against currency fluctuations, ensuring yield premiums remain intact. Additionally, placing private credit investments in tax-advantaged accounts like RRSPs or TFSAs - where eligible - can shield high-single-digit distributions from annual taxation. With these complexities in mind, expert advice becomes essential to make the most of private credit opportunities.

Working with a Private Banking Expert

Managing private credit investments takes time and expertise. Sean O'Hara, CIO of Obsiido Alternative Investments Inc., emphasizes:

"I put in 15 to 20 hours of upfront work on a given private credit strategy. If you don't have that time and decide to forgo private credit, that's a good decision."

This level of diligence - examining underwriting standards, capital structure, PIK note exposure, and liquidity terms - is where private banking professionals add real value. For most investors, the key question isn't if they should include private credit but how to do it effectively. A knowledgeable advisor can tailor strategies to your specific financial situation. If you're seeking expert guidance, Find Wealth Experts and Private Bankers in Canada offers a province-by-province directory of professionals specializing in private credit and wealth management strategies.

Conclusion

Key Takeaways

Private credit in Canada has evolved far beyond its early days as a niche investment option. Now, with a growing consensus among Canadian advisors targeting a 10–25% allocation for private markets, it's clear that private credit is becoming a standard feature in diversified portfolios. The commitment of Canadian wealth managers to increasing alternative allocations underscores this shift, signalling that private credit is no longer a fringe strategy but a mainstream component.

However, the path forward is not without challenges. Issues like liquidity mismatches, widening performance gaps between managers, and heightened scrutiny from OSFI and the Bank of Canada demand careful navigation. Interestingly, private credit now ranks as the third most preferred private market asset class, following private equity and infrastructure. This shift reflects its growing role within a broader investment strategy rather than a standalone focus. As Bank of Canada Governor Tiff Macklem aptly noted:

"There is a need for additional 'guardrails' to ensure retail investors fully understand restrictions around redemptions and ability to access their cash."

These insights provide a framework for understanding the opportunities and challenges shaping the future of private credit in Canada.

The Road Ahead for Private Credit in Canada

The future of private credit in Canada offers a mix of expanding opportunities and notable risks. Beyond traditional middle-market direct lending, new avenues like asset-based finance (ABF), specialty finance, and infrastructure debt (including data centres) are gaining traction. On a global scale, retail allocation to private credit is expected to grow at an impressive annual rate of nearly 80%, potentially reaching US$2.4 trillion by 2030. Closer to home, a unique opportunity emerges as 40% of Canadian mortgages are set to mature in 2026, creating a funding gap that private lenders are well-suited to fill.

Still, risks persist. The increasing use of payment-in-kind (PIK) loans and the heavy concentration of direct lending portfolios in the software sector - estimated at 21% - highlight areas that demand vigilance as AI continues to reshape industries. Selecting experienced managers is more important than ever as performance disparities widen.

A disciplined approach is key. Investors should focus on understanding redemption terms, confirming registered account eligibility, and partnering with managers who have demonstrated success across full credit cycles. For those ready to act, connecting with a qualified private banking expert is a critical step. The Find Wealth Experts and Private Bankers in Canada directory offers a province-by-province guide to advisors who specialize in private credit, making it easier to take the next step with confidence.

FAQs

How do I know if a private credit fund can gate withdrawals?

When determining if a private credit fund can restrict withdrawals, start by examining its subscription documents. These documents detail the fund's redemption policies, including any limits on withdrawals (like quarterly caps), required notice periods, and whether the manager has the power to temporarily suspend redemptions. Don’t rely on marketing materials alone - even if the fund is described as "semi-liquid", such descriptions are not definitive. Gating mechanisms are built into the fund's structure to safeguard unitholders during periods of market turbulence. Always operate under the assumption that liquidity is conditional, not guaranteed.

What should I check to spot valuation risk or “shadow defaults”?

To spot potential valuation risks or shadow defaults, keep an eye out for signs of financial strain, even if a company appears to meet the terms of its credit agreements. Some key red flags to monitor include:

- Frequent use of payment-in-kind (PIK) interest: This can signal cash flow issues, as it allows borrowers to delay cash payments by issuing more debt instead.

- Maturity extensions or amend-and-extend transactions: These moves often indicate difficulty in meeting repayment obligations on time.

- Repeated sponsor support: Actions like equity injections or covenant waivers may suggest underlying financial instability.

- Liquidity stress: Warning signs include restrictions on withdrawals or the depletion of liquid assets.

- Increasing non-accrual loans or distressed restructurings: These often occur before outright payment failures and highlight deeper financial troubles.

By keeping these factors in mind, you can better assess the financial health of an entity and identify potential risks early.

How can I access private credit in my RRSP or TFSA without taking on U.S.$ currency risk?

You can include private credit in your RRSP or TFSA by selecting funds that focus on Canadian investments and operate in Canadian dollars. These funds typically provide loans to Canadian businesses or invest in local assets, helping you sidestep risks tied to U.S. currency fluctuations. Make sure the fund qualifies for RRSPs and TFSAs and is designed specifically for the Canadian market. For tailored advice on adding these investments to your accounts, reach out to a wealth management professional.