The Canada Revenue Agency (CRA) has introduced updated rules for donor-advised funds (DAFs) to improve transparency and ensure funds are actively benefiting charities. DAFs, which hold over $13 billion in assets across 250+ foundations, allow donors to contribute assets, receive tax receipts, and recommend grants to charities. However, the CRA emphasizes that the administering charity has sole control over fund decisions.

Key changes include:

- New Reporting Requirements: Charities must disclose DAF-related data on the updated Form T3010 (Version 24) and comply with stricter reporting on disbursement quotas (DQ).

- Tiered DQ Structure: Larger foundations face increased disbursement rates, with a 5% DQ for assets exceeding $1 million.

- Donor Influence Rules: Donors can only provide non-binding recommendations, and charities must avoid private benefits or improper fund use.

These guidelines impact donors, wealth managers, and foundations, requiring adjustments to giving strategies, reporting, and compliance processes.

Trailer: How do DAF’s Work?

sbb-itb-e9c03dd

Overview of Key Regulatory Changes

Canada has introduced notable updates to its donor-advised fund (DAF) framework, focusing on accountability and transparency. These changes primarily address three areas: revamped CRA reporting through an updated T3010 form, a tiered disbursement quota (DQ) system with stricter requirements for larger foundations, and clearer guidelines on donor influence and private benefit. The aim is to improve reporting, enforce stricter disbursement rules, and clarify the roles of donors and charities.

New CRA Reporting Requirements

Starting with fiscal periods ending on or after 31 December 2023, charities must use the updated Form T3010 Version 24. A newly added Section C18 requires charities to disclose whether they manage DAFs, along with details on the number of accounts and their total asset value. Additionally, charities must now report financial activities related to DAFs, such as the total amount donated into these accounts and the total amount granted out annually.

The form also includes changes to Schedule 8, which now handles DQ compliance calculations, and updates to Schedule 1, requiring charities to disclose non-spendable restricted funds like endowment capital subject to funder-imposed written trusts.

"These changes to the T3010 are giving policymakers better data to make evidence-based decisions. I'm all for that." - Kate Bahen, Managing Director, Charity Intelligence

Changes to the Disbursement Quota (DQ)

In addition to the reporting updates, the federal government has introduced a tiered DQ structure for fiscal periods beginning on or after 1 January 2023. The DQ rate remains at 3.5% for the first $1,000,000 of non-charitable property but increases to 5% for amounts exceeding that threshold. This applies specifically to the administering charity.

In the first year of implementation, foundations collectively disbursed an additional $711 million. However, 54% of affected foundations did not meet their new disbursement requirements during this period. To address potential shortfalls, charities can carry forward excess disbursements from the previous five years.

Donor Control and Private Benefit Rules

To ensure a clear separation of roles, the CRA has reinforced guidelines around donor influence and private benefit. While donors can offer advice on fund allocations, the charity must retain full authority over final decisions. Donor suggestions are strictly non-binding, and charities must avoid any arrangements where funds are directed to specific non-qualified donees.

The CRA’s anti-directed giving rule prohibits conditional gifts that act as conduits for specific non-charitable purposes. Furthermore, any private benefit resulting from a donation must be minimal and proportionate to the public good. As noted by Miller Thomson LLP, breaching this "conduit" rule could result in the charity losing its status.

To navigate these challenges, the CRA recommends a risk-based due diligence approach. Charities are encouraged to assess grants as low, medium, or high risk based on factors like the governance of the recipient and potential private benefit issues. Formal agreements and clear fund tracking are advised to mitigate risks.

What the New Rules Mean for Donors and Advisors

For Donors: Aligning with the New Rules

One of the most important changes for donors is understanding that once funds are contributed to a Donor-Advised Fund (DAF), they are irrevocable. From that point on, the sponsoring charity has full control over the funds. While donors can provide recommendations, the ultimate decision-making authority lies with the charity. These updates, shaped by the CRA guidelines introduced in 2023 and 2024, require donors to adapt their strategies and expectations.

To ensure your giving aligns with your values, it’s essential to review your DAF sponsor’s governing documents. Grants can only be recommended for purposes approved by the charity. Developing a multi-year giving strategy can help you better assess the impact of your donations while reducing the risk of violating the anti-directed giving rule.

These regulatory changes also bring a new level of complexity to the advisory process in charitable giving.

For Wealth Managers and Advisors

For wealth managers and advisors, the shift in CRA guidelines places a stronger emphasis on compliance and accountability. With donor direction becoming more restricted, advisors must guide clients not only on what they can give but also on how to structure and document their contributions.

One critical task is helping clients navigate the CRA’s five-step due diligence model:

- Determining how a grant supports the charity’s purposes

- Evaluating the level of risk involved

- Choosing the right accountability measures

- Collaborating effectively with the grantee

- Keeping detailed and accurate documentation

For grants exceeding $5,000 to non-qualified donees, advisors must ensure proper reporting on Form T1441. This includes key details like the grantee’s name, the purpose of the grant, the amount, and the country where the activity takes place. Additionally, advisors should examine the governance practices of DAF sponsors, ensuring there are written agreements, clear reporting structures, and separate tracking of funds. For foundations struggling to meet disbursement quotas, CRA Guidance CPC-029 provides information on applying for relief.

In this changing regulatory landscape, having local expertise is more important than ever.

Working with Local Canadian Experts

Canada’s charitable sector is shaped by regional differences, including variations in giving cultures and the increasing use of complex assets like private company shares and appreciated securities. Navigating these provincial nuances requires the support of local legal and financial professionals who are well-versed in regional rules and the CRA’s evolving interpretations of the Income Tax Act.

For those seeking localized expertise, the Find Wealth Experts and Private Bankers in Canada directory offers a province-by-province guide to wealth management professionals. Whether you’re handling a complex securities donation in British Columbia or reviewing a DAF sponsor’s governance practices in Ontario, connecting with a local specialist can help ensure compliance and maximize the impact of your philanthropy.

Research and Policy Analysis: Key Findings

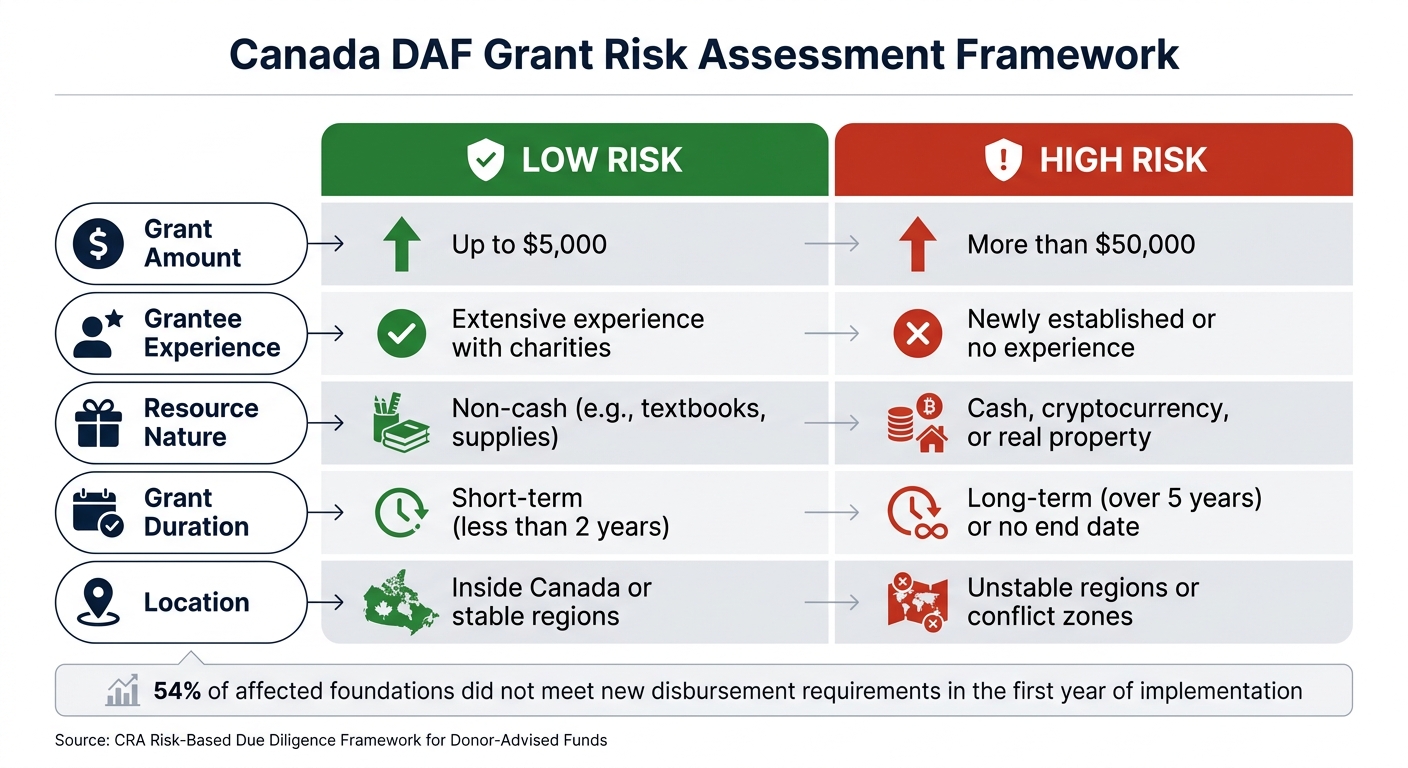

Canada DAF Risk Framework: Low vs High Risk Grant Factors

Benefits of Donor-Advised Funds

Donor-Advised Funds (DAFs) are becoming increasingly popular in Canada as a tool for charitable giving. By early 2026, there were more than 250 DAF foundations managing around 40,000 individual accounts nationwide. These funds offer a more affordable setup and allow donors to defer their charity designations.

"DAFs can provide donors with a quicker way to attain their philanthropic and tax-planning goals, without the headache, time, or expense of establishing and operating a standalone charity." - Miller Thomson LLP

One of the standout features of DAFs is their ability to handle complex gifts - like private company shares or insurance policies - that smaller charities might struggle to process. This capability helps bridge gaps for organizations that lack the resources to manage such donations. DAFs also encourage families to engage in long-term, intergenerational philanthropy, fostering a shared commitment to giving over time.

However, despite these benefits, there are hurdles that need addressing.

Challenges and Regulatory Concerns

One key issue with DAFs lies in the timing of fund distribution. Donors benefit from immediate tax advantages, but charities often face delays in receiving the funds.

In 2023, DAFs in Canada had an average payout ratio of 9.7%, which drops to just 5.4% for those held by community foundations. With an average account size of $406,000 in 2021, smaller grassroots and Indigenous-led organizations often find these funds out of reach due to limited infrastructure. Another concern is the lack of detailed reporting - current CRA forms (like the T3010) don’t track disbursement rates for individual accounts, making it difficult to evaluate whether the funds are being actively used.

Best Practices for DAF Governance

To address these challenges, strong governance practices are critical. In October 2025, the Canadian Association of Gift Planners introduced five detailed guides to improve policy consistency across DAF foundations in Canada. Nicola Elkins from Benefaction Foundation and Malcolm Burrows from Aqueduct Foundation spearheaded this initiative, which emphasizes moving from rigid control to a more flexible, risk-based accountability model.

Effective governance starts with clear written agreements, well-defined investment policies, and transparent fee disclosures. Governing documents should explicitly support grant-making activities, and for grants to non-qualified donees, the CRA’s risk framework provides a helpful guideline. Below is a summary of key risk factors that influence the level of oversight required:

| Risk Factor | Low Risk | High Risk |

|---|---|---|

| Grant Amount | Up to $5,000 | More than $50,000 |

| Grantee Experience | Extensive experience with charities | Newly established or no experience |

| Resource Nature | Non-cash (e.g., textbooks, supplies) | Cash, cryptocurrency, or real property |

| Grant Duration | Short-term (less than 2 years) | Long-term (over 5 years) or no end date |

| Location | Inside Canada or stable regions | Unstable regions or conflict zones |

Looking ahead, the sector is gearing up for a likely federal review of the disbursement quota in 2027. Groups like Philanthropic Foundations Canada have already initiated Impact Taskforces to gather data and propose recommendations. Early findings suggest that the 2023 increase of the disbursement quota to 5% led to an additional $711 million being channelled into charitable initiatives across Canadian communities.

Conclusion and Next Steps

Key Takeaways for Stakeholders

The revised Canadian DAF guidelines clarify that donated funds are under the ownership and control of the registered charity, with donors limited to offering non-binding recommendations. It's crucial for advisors and foundations to ensure that governing documents explicitly define active charitable purposes. Additionally, grant-making must align with the CRA's risk-based due diligence framework. This is particularly important for grants exceeding $5,000 to non-qualified donees, which must be disclosed on Form T1441. Moving forward, potential regulatory changes could further influence how DAFs operate.

Future Regulatory Developments to Watch

With these updated guidelines in place, further adjustments in DAF regulations are likely. A key area to monitor is the treatment of unused DAF assets. Currently, there are no mandatory minimum spending requirements for individual DAF accounts, but this could change. To stay informed, review the CRA’s annual update to the Gifts and Income Tax guide (P113), which is typically released each January.

Connecting with Local Experts

Given the regional variations in DAF practices across Canada, consulting local experts is essential. Regulations and philanthropic strategies can differ significantly between provinces. To ensure compliance and optimize the impact of your philanthropic efforts, explore the Find Wealth Experts and Private Bankers in Canada directory for professional guidance tailored to your region.

FAQs

Do these CRA DAF rules change my tax receipt or donation timing?

When you contribute to a donor-advised fund (DAF) in Canada, the Canada Revenue Agency's guidelines ensure you receive an immediate charitable tax receipt. This is because your donation is considered irrevocable. However, it's important to note that no tax receipt will be issued when you recommend grants from the DAF to other charities.

For personalized guidance on managing your charitable giving, it's a good idea to consult with wealth advisors or private banking professionals who specialize in Canadian philanthropy. They can help you align your giving strategy with your financial goals.

How can I recommend grants without breaking the directed giving rules?

To comply with donor-advised fund (DAF) rules, it’s crucial to understand that your role is advisory, not directive. The registered charity overseeing your fund retains legal ownership and has the final say over all assets. Your recommendations must remain non-binding and should only involve registered charities. DAF assets cannot be used to support non-qualified donees, personal pledges, event tickets, or memberships. For specific advice, it’s a good idea to consult wealth experts or private bankers familiar with Canadian regulations.

What is the new disbursement quota for foundations with over $1,000,000?

Canadian registered charities and foundations are required to determine their disbursement quota by calculating a percentage of the average value of property that hasn't been used for charitable activities or administrative purposes over the past 24 months. For property valued above $1,000,000, the quota is set at 5%, while for the first $1,000,000, it stands at 3.5%.