Families with connections to Canada and the US face complex estate planning challenges due to differences in tax systems, legal rules, and compliance requirements. Here's what you need to know:

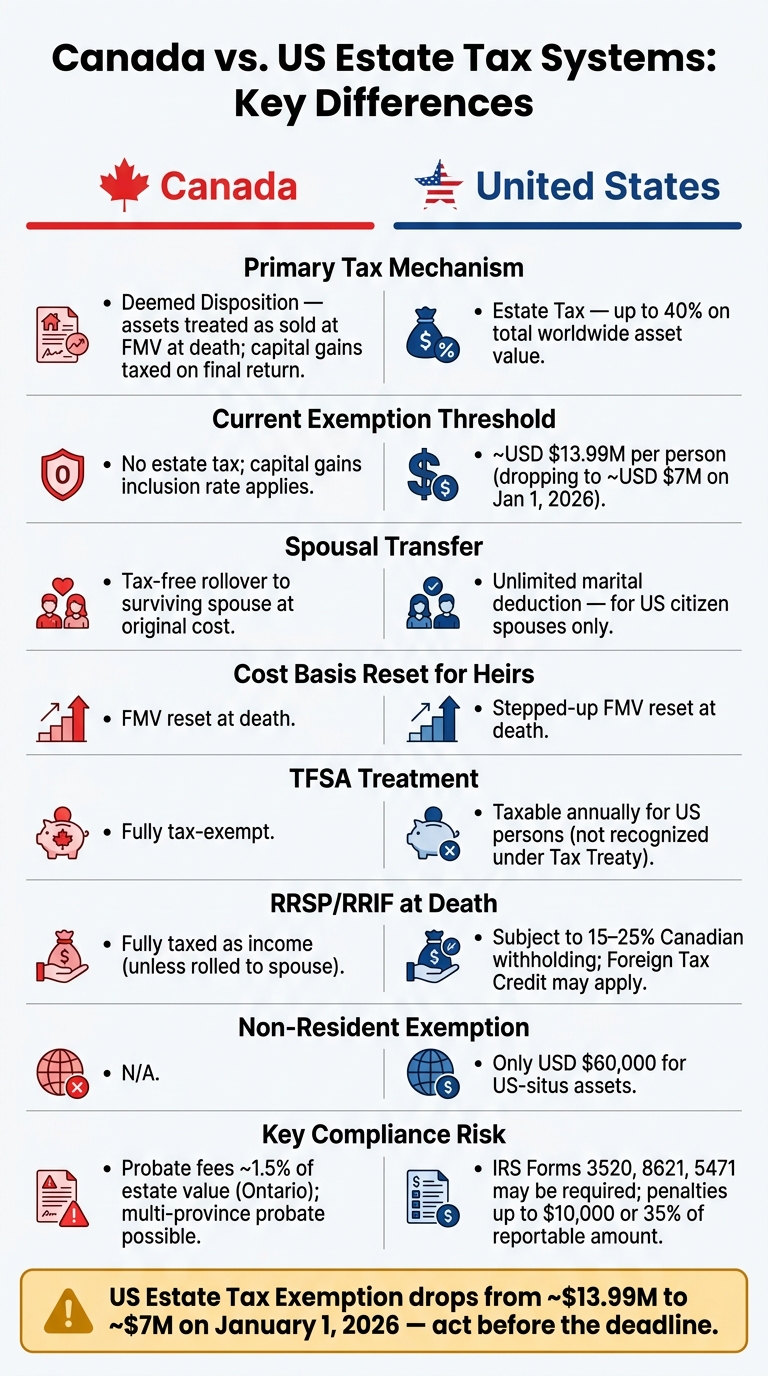

- Canada taxes capital gains through a "deemed disposition" system, treating assets as sold at fair market value upon death.

- The US imposes an estate tax on the total value of assets, with rates up to 40%, but allows exemptions (currently ~USD $13.99M, dropping to ~USD $7M in 2026).

- Timing differences between the countries can lead to double taxation and liquidity issues.

- Registered accounts like RRSPs and TFSAs create additional hurdles for US-resident heirs due to conflicting tax treatments.

- Mixed-citizenship families and heirs residing in different countries may face unique complications, from compliance costs to disputes over liabilities.

Quick Overview of Key Differences:

| Feature | Canada | United States |

|---|---|---|

| Primary Tax Mechanism | Deemed disposition (capital gains) | Estate tax on total asset value |

| Spousal Transfer | Tax-free rollover to a surviving spouse | Unlimited deduction for US citizen spouses |

| Cost Basis for Heirs | FMV reset at death | FMV reset at death |

| TFSA Treatment | Tax-exempt | Taxable annually for US persons |

| Non-Resident Exemption | N/A | Only US$60,000 for US-situs assets |

To navigate these complexities, families should consider coordinated wills, specialized planning for registered accounts, and expert advice from cross-border professionals. Early preparation is key to avoiding costly disputes and ensuring smoother estate transitions.

Cross-Border Inheritance: What Canadian Beneficiaries Need to Know

sbb-itb-e9c03dd

How Canadian and US Estate Systems Differ

Canada vs. US Estate Tax: Key Differences at a Glance

Canada's Estate Planning Rules

Canada doesn’t have an estate tax. Instead, it uses a deemed disposition system. This means that when someone passes away, their assets are treated as if they were sold at fair market value (FMV) on the date of death. Any capital gains from this notional sale are taxed as income on the deceased's final tax return.

There are some key exceptions to this rule. For example, if assets are transferred to a surviving spouse, they roll over tax-free at their original cost. This defers the tax until the surviving spouse either sells the assets or passes away. However, registered accounts like RRSPs and RRIFs are fully liquidated and taxed as income upon death unless they are rolled over to a spouse. While TFSAs are tax-exempt in Canada, they can cause complications for families with US connections.

In Ontario, probate fees are approximately 1.5% of the estate’s value for amounts over $50,000. Estates with assets spread across multiple provinces - or both Canada and the US - might also need to go through separate probate processes in each jurisdiction.

US Estate Planning Rules

The US follows a completely different system. Instead of taxing capital gains, it imposes an estate tax on worldwide assets for citizens and residents, and on US-based assets for non-residents. Federal estate tax rates can go as high as 40%, but exemptions of up to US$15 million per person shield most estates from these taxes.

One advantage for US heirs is the stepped-up cost basis. This resets the value of inherited assets to their FMV at the time of death, allowing heirs to sell them later with minimal or no capital gains tax. The US also offers an unlimited marital deduction, but only if the surviving spouse is a US citizen. If the spouse is not a US citizen, this deduction doesn’t apply, which can result in a significant tax burden.

"The US estate tax system treats a non-US citizen surviving spouse very differently from a US citizen one. The unlimited marital deduction... doesn't apply when the survivor is a non-citizen." - Lucas Wennersten, Cross-Border Financial Advisor

US heirs inheriting Canadian accounts face additional challenges. The US does not recognize TFSAs as tax-exempt under the US-Canada Tax Treaty, which means US citizens or residents must pay tax annually on earnings within the TFSA. Furthermore, Canadian mutual funds and ETFs are classified as Passive Foreign Investment Companies (PFICs) under US tax law, requiring complex IRS reporting through Form 8621 and potentially facing high tax rates.

These differences in taxation and compliance create significant hurdles for families managing cross-border estates.

Where the Two Systems Create Problems for Families

The primary issue lies in timing and structure. Canada taxes assets immediately at death, while the US often defers taxes until the assets are sold or distributed. This mismatch can make it harder for estates to use foreign tax credits effectively, and families may struggle to find liquidity when they need it most.

Here’s a quick comparison of the two systems:

| Feature | Canada | United States |

|---|---|---|

| Primary Tax Mechanism | Deemed disposition (capital gains) | Estate tax on total asset value |

| Spousal Transfer | Tax-free rollover to a surviving spouse | Unlimited marital deduction for US citizen spouses only |

| Cost Basis for Heirs | FMV reset at death | FMV reset at death |

| TFSA Treatment | Tax-exempt | Taxable annually for US persons |

| Non-Resident Exemption | N/A | Only US$60,000 for US-situs assets |

US heirs of Canadian estates bear a heavier compliance burden. Depending on the assets inherited, they may need to file IRS Form 3520 for foreign trusts, Form 8621 for PFICs, or Form 5471 if they inherit shares in a Canadian private corporation. Missing Form 3520, for example, can lead to penalties of $10,000 or 35% of the gross reportable amount. These compliance demands not only add stress but can also lead to family disputes and liquidity challenges, further complicating cross-border estate planning.

Understanding these differences is a critical first step before diving into strategies for managing cross-border estates effectively.

Family Dynamics in Cross-Border Estates

Mixed-Citizenship Families and Inheritance

Mixed-citizenship families often encounter complex inheritance issues. Take this example from 49th Parallel Wealth Management (2026): David, a US citizen living in Toronto, holds a $1.6M RRSP. If his Canadian spouse, Sarah, passes away first, David inherits her TFSA. However, under US tax laws, the TFSA loses its tax-exempt status, turning into a taxable asset for him. This change can heavily impact the overall tax burden on the estate.

Another challenge comes with the US marital deduction. When a Canadian spouse leaves assets directly to their US-citizen partner, the US-taxable estate of the surviving partner increases significantly. For instance, MNP (2023) documented Peter, a Canadian with a $21.3M net worth, married to Cathy, a US citizen. If Peter had left his assets outright to Cathy, her estate might have faced a US tax bill ranging from $1.4M to $3.7M upon her death. Using a spousal trust instead could have kept those assets out of her taxable estate entirely.

Beyond citizenship, the residency of heirs plays a key role in determining the tax impact of an inheritance.

How Heir Residency Affects Estate Distribution

After navigating citizenship concerns, residency adds another layer of complexity to inheritance outcomes. Where an heir resides at the time of inheritance can dramatically affect the taxes they face. A Canadian-resident heir and a US-resident heir inheriting the same assets from the same estate can end up with vastly different after-tax results.

"The US tax system follows its citizens - everywhere. Unlike Canada, the United States taxes its citizens and permanent residents on their worldwide income, regardless of where they live or where the assets originate." - Cardinal Point Wealth Management

For example, a US-resident heir inheriting Canadian mutual funds might face PFIC classification, which leads to high tax rates and requires annual Form 8621 filings. Meanwhile, a Canadian-resident sibling inheriting the same funds avoids these complications. Similarly, if a US heir inherits 10% or more of a Canadian private corporation, the company could be classified as a Controlled Foreign Corporation (CFC). This could result in the heir being taxed on the corporation’s earnings, even if no dividends are distributed.

Practical barriers also arise. Canadian investment advisors are generally not allowed to advise US-resident executors or beneficiaries unless they are SEC-licensed. This restriction often leads financial institutions to freeze access to accounts for US-resident heirs.

Common Disputes Over Asset Distribution

Beyond citizenship and residency, specific assets can ignite family conflicts. One frequent issue is the RRSP tax trap. In Canada, when an RRSP is left directly to a named beneficiary, the beneficiary receives the full amount, but the estate is responsible for paying the associated income tax. For example, Allan Madan, CPA (2025), shared a case where a US citizen in Toronto named his daughter Anna as the direct beneficiary of a $1M RRSP. Anna received the entire $1M, but the estate faced a $500,000 tax bill in Canada, potentially forcing the sale of family assets.

"The estate, not the beneficiary, pays this tax [on RRSPs]... This can cause cash-flow problems: the estate might need to sell other assets, like John's house, to cover the CRA tax bill." - Allan Madan, CPA, CA

Another source of tension is compliance costs. Cross-border filings, such as IRS Form 3520 for foreign trust distributions or Form 5471 for inherited shares in Canadian private corporations, can be expensive. Families often argue over whether these costs should be charged to the specific heir responsible for triggering them or absorbed by the estate as a whole. When heirs are spread across two countries, with different tax liabilities and varying net inheritances, deciding what’s fair becomes a contentious issue. These disputes highlight the importance of aligning cross-border estate plans to prevent conflicts before they arise.

How to Plan a Cross-Border Estate Effectively

Aligning Wills Across Both Countries

It's rare for a single will to cover assets in two countries effectively. The solution? Create separate but coordinated wills: one for your Canadian assets and another for your US-based holdings, like American real estate or US investment accounts. Without a US-specific will, your family might face a lengthy IRS "transfer certificate" process, which can take over a year to complete.

One common pitfall is the standard revocation clause found in many Canadian will templates. This clause automatically cancels all prior wills, which could unintentionally invalidate your US will. If that happens, your American assets might end up being distributed under provincial intestacy rules instead of your intended plan.

Choosing the right executor is just as critical. For example, naming a US-resident child as the sole executor could shift the estate's "mind and management" to the US. This could lead the CRA to classify the estate as non-resident, causing it to lose its Graduated Rate Estate (GRE) status and face taxation at the highest marginal rates. To avoid this, appoint majority Canadian-resident co-executors to maintain Canadian tax residency.

"A foreign Will alone may not effectively administer U.S. assets, while a U.S. Will drafted in isolation can unintentionally disrupt an existing foreign estate plan." - Allison E. Dolzani, Ruchelman PLLC

Managing Canadian Accounts for US-Resident Heirs

Once your wills are coordinated, the next step is addressing how Canadian registered accounts are handled for US-resident heirs:

- TFSAs lose their tax-exempt status for US persons and become fully taxable.

- RRSPs and RRIFs are subject to Canadian withholding tax: 15% on periodic payments and 25% on lump-sum withdrawals. However, US-resident heirs can claim a Foreign Tax Credit on their US tax return if the right paperwork is filed.

- PFIC issues arise with Canadian mutual funds or ETFs. These can trigger annual Form 8621 filings and punitive tax rates. To avoid this, consider liquidating these investments before death and reinvesting in individual securities or US-listed ETFs.

For larger estates, especially where one spouse is not a US citizen, a Qualified Domestic Trust (QDOT) might be necessary. Without a QDOT, US estate tax on assets exceeding the exemption threshold becomes payable immediately upon the Canadian spouse's death, as the unlimited marital deduction doesn't apply to non-US-citizen spouses.

To navigate these complexities, work closely with advisors who specialize in cross-border estate planning.

Working with Canadian Private Banking and Wealth Experts

Handling these account challenges requires guidance from professionals with expertise in both Canadian and US systems. Cross-border planning demands a deep understanding of how the rules in each country interact, which makes specialised knowledge essential.

"A Canadian accountant who has never dealt with IRS Form 3520 is not equipped to handle an RRSP inheritance by a US person." - Shiraz Ahmed, CEO, Sartorial Wealth

When choosing an advisor, look for dual registration - someone licensed in both Canadian provinces and the US (SEC registration) to ensure they can legally advise US-resident heirs. This step also helps prevent account freezes at Canadian financial institutions.

For families navigating these complex decisions, Find Wealth Experts and Private Bankers in Canada offers a directory of professionals across the country. This resource can help you find advisors with the cross-border expertise needed to coordinate wills, manage registered accounts, and address compliance challenges.

"The upfront cost of preparing two properly coordinated wills is almost always far less than the cost of untangling the problems that arise from using just one." - Phil Hogan, CPA, CA

Conclusion: Addressing Family Challenges in Cross-Border Estates

Cross-border estates bring significant risks due to the stark contrasts between Canadian and US tax systems. In Canada, taxes are applied to capital gains accrued at death through deemed disposition, while the US imposes an estate tax on the total value of worldwide assets. These differing approaches can result in double taxation and liquidity issues if not handled carefully.

Tax treatment of registered accounts like RRSPs and TFSAs further complicates matters. RRSPs can expose estates to substantial tax liabilities, while TFSAs offer no protection for heirs living in the US. Adding to the urgency, the current US estate tax exemption - approximately USD $13.99 million - is set to drop to around USD $7 million on 1 January 2026. Families with significant US-situs assets have a limited opportunity to adjust their estate plans before this reduction takes effect. Mixed-citizenship families face even more challenges, from QDOT requirements for non-citizen spouses to the risks posed by an executor’s residency, which could entirely change the tax treatment of the estate. Customizing estate plans to address these specific issues is crucial.

Preparation is the cornerstone of successfully navigating these complexities.

"The families who come through this cleanly are the ones who get organized early, build the right team, and resist the urge to make quick decisions under pressure. The families who struggle are the ones who assume it will work itself out." - Shiraz Ahmed, CEO and Portfolio Manager, Sartorial Wealth

Seeking advice early from professionals who understand both CRA and IRS regulations is what separates smooth estate transitions from costly disputes. For Canadian families facing these decisions, Find Wealth Experts and Private Bankers in Canada offers a directory of wealth advisors across the country, organized by province, to help you connect with experts in cross-border estate planning.

FAQs

How can I avoid double taxation on a Canada–US estate?

To navigate potential double taxation, it's important to consider Canada's deemed disposition rules and the U.S. estate tax. Both countries adjust the cost base of inherited assets to their fair market value at the time of inheritance, which means taxes typically apply only to gains made after the inheritance.

Options to manage this include:

- Claiming a foreign tax credit: You can offset U.S. estate taxes on your Canadian tax return.

- Using the Canada–U.S. Tax Treaty: This treaty provides mechanisms to reduce or eliminate double taxation.

- Exploring a Qualified Domestic Trust (QDOT): This tool can help defer or reduce U.S. estate taxes in certain situations.

For the best results, seek advice from tax and estate planning professionals who can tailor strategies to your specific circumstances.

What should I do if a US-resident heir will inherit my RRSP or TFSA?

When a U.S.-resident inherits a Registered Retirement Savings Plan (RRSP) or a Tax-Free Savings Account (TFSA) from Canada, navigating the tax rules on both sides of the border can get complicated. Here's what you need to know:

RRSPs: In Canada, RRSPs are subject to a "deemed disposition" tax on the deceased's final tax return. However, in the U.S., the focus is on taxing the withdrawals made by the heir. Additionally, the IRS treats RRSPs as foreign trusts, which means heirs are required to file forms like 3520 and 3520-A to report the account and avoid penalties.

TFSAs: Unlike in Canada, TFSAs don’t enjoy tax-free status in the U.S. Any growth within the account and withdrawals are considered taxable income under U.S. tax law.

To avoid costly mistakes or penalties, it's essential to consult a professional who specializes in cross-border tax matters. They can help ensure you're meeting the requirements in both countries while minimizing tax exposure.

Do I need two wills if I own assets in both Canada and the US?

Having two wills isn't always required, but it can make managing estates with assets in both Canada and the US much easier. By creating separate wills for each country, you can reduce legal complications and simplify the probate process in each jurisdiction. To avoid issues, each will should clearly specify which assets it covers and ensure it doesn't revoke the other. It's a good idea to consult with legal and tax professionals to see if this strategy aligns with your cross-border estate planning goals.