For high-net-worth Canadians, standard insurance policies often fall short when it comes to protecting significant assets like private businesses, investment properties, and multi-million-dollar portfolios. Advanced insurance strategies help manage estate taxes, provide liquidity, and ensure smooth wealth transfers. Here's a quick guide to the best options:

- Whole Life Insurance: Offers lifelong coverage, tax-free death benefits, and tax-sheltered cash value growth. Ideal for covering estate taxes and preserving wealth.

- Universal Life Insurance: Combines insurance with investment flexibility, allowing policyholders to grow funds tax-free while addressing estate planning needs.

- Term Life Insurance: Affordable, time-limited coverage for specific needs like mortgage protection or business loans.

- Corporate-Owned Life Insurance (COLI): Helps business owners grow corporate funds tax-efficiently while securing wealth for future generations.

- High-Net-Worth Property Insurance: Protects luxury assets like estates, fine art, and collector vehicles with higher limits and broader coverage.

- Umbrella Liability Insurance: Extends liability protection up to $100 million, covering risks like lawsuits and global incidents.

- Global Health Coverage: Ensures access to premium healthcare worldwide, filling gaps left by provincial health plans.

- Specialty Coverage: Tailored for luxury items, offering agreed-value payouts and protection for unique risks.

Each policy serves a specific purpose, from reducing tax burdens to protecting physical assets. Consult financial, legal, and insurance advisors to create a plan that aligns with your goals.

How Canadians Are Using Life Insurance as an Investment

sbb-itb-e9c03dd

1. Whole Life Insurance for Estate and Tax Planning

Whole life insurance continues to dominate as the leading permanent insurance option for affluent Canadians, accounting for 80% of all permanent insurance sales in Canada during the first quarter of 2025. Unlike term insurance, it provides lifelong coverage, builds cash value, and guarantees a tax-free death benefit for beneficiaries.

The primary draw for high-net-worth estates is its timing advantage. According to Section 70(5) of the Income Tax Act, the CRA treats all capital property as if it were sold at fair market value upon death, which can result in significant capital gains taxes. As Nizam Shajani, CPA, CA, TEP of Shajani CPA, explains:

"The problem is not the tax - it's the timing. Your executor must come up with cash quickly to pay this tax bill."

The death benefit from a whole life policy provides immediate, tax-free funds, helping executors cover these liabilities without the need to liquidate assets like family businesses or investment properties. For couples, a joint last-to-die policy is particularly effective, as it pays out after the second death - right when the final capital gains taxes are due.

Additionally, the cash value within the policy grows tax-sheltered under Section 148 of the Income Tax Act, making it a valuable tool alongside fully utilized RRSPs and TFSAs. Vanessa Smith, an Insurance Advisor at PolicyAdvisor, highlights this benefit:

"A whole life policy's ability to build cash value on a tax-advantaged basis while simultaneously providing estate liquidity makes it particularly valuable for those facing maximum marginal tax rates."

This tax-sheltered growth enhances its role in preserving long-term wealth.

For business owners, the benefits extend even further. A corporate-owned whole life policy allows premiums to be paid with lower-taxed corporate dollars. Upon death, the death benefit flows through the Capital Dividend Account (CDA), enabling the corporation to distribute funds to shareholders entirely tax-free. This approach integrates estate planning with corporate financial strategies, aligning personal and business interests. For a 45-year-old male seeking $5 million in coverage, premiums typically range from $35,000–$45,000 per year for a life-pay structure or $60,000–$80,000 per year for a 20-pay plan. Current dividend scale interest rates from major Canadian insurers are as follows:

| Insurer | 2025 Dividend Scale Interest Rate |

|---|---|

| Equitable Life | 6.40% |

| Manulife | 6.35% |

| iA Financial Group | 6.35% |

| RBC Insurance | 6.30% |

| Sun Life | 6.25% |

| Canada Life | 5.75% |

To maximize the benefits of a whole life policy, it's essential to structure ownership and beneficiary designations carefully with professional guidance. Naming a preferred beneficiary, such as a spouse or child, instead of the estate, can also offer creditor protection for both the cash value and the death benefit. This thoughtful planning makes whole life insurance a cornerstone for advanced estate strategies.

2. Universal Life Insurance for Flexible Wealth Strategies

If whole life insurance is about stability, universal life (UL) insurance is about adaptability. It gives policyholders more control, especially when it comes to managing investments. For high-net-worth Canadians who have already maxed out their RRSP and TFSA contributions, UL offers a valuable third option for tax-deferred growth. Extra funds invested in the policy grow in a tax-sheltered account, where interest and gains accumulate more efficiently. This unique flexibility makes UL a standout choice for managing wealth and premiums.

One of UL's biggest advantages is its investment flexibility. Unlike whole life insurance, where the insurer handles the participating fund, UL allows policyholders to choose how their savings are invested. Options include daily interest accounts, GIC-style guaranteed interest accounts, or market-linked managed accounts. For example, Equitable Life offers a 0.75% annual bonus starting in the first year, and Manulife eliminates management fees on certain managed accounts.

Another benefit is the ability to adjust contributions. Policyholders can contribute as little as necessary to keep the policy active or as much as the Income Tax Act allows. This means that a business owner experiencing a challenging year can scale back payments and then increase contributions during better financial times. Death benefits can also be tailored to estate planning needs, with options like level protection (whichever is greater: the coverage amount or policy fund value) or increasing protection (the coverage amount plus the accumulated fund value).

For estate planning, the joint last-to-die structure is particularly effective. It pays out after the second spouse’s death, which is when substantial tax liabilities - such as capital gains on family cottages or taxes on RRSP/RRIF assets - are due. This tax-free death benefit can provide immediate funds, preventing heirs from having to sell assets to cover taxes. Business owners can also use UL for estate equalization, leaving a business to one child while using the policy's payout to provide an equivalent inheritance to other children.

As Nizam Shajani, CPA, CA, TEP, LL.M (Tax), explains:

"Life insurance, used strategically, becomes more than a policy - it becomes a pillar of intergenerational wealth planning."

Additionally, UL policies allow for collateral lending, enabling policyholders to borrow up to 50% of the policy's cash value. This approach provides access to funds without triggering a taxable event, making it a useful tool for supplementing retirement income or financing new investments - all while the policy’s cash value continues to grow tax-deferred.

3. Term Life Insurance for High-Value, Time-Limited Needs

Term life insurance is a practical solution for Canadians looking for coverage over a specific period - often 10, 20, or 30 years. Its straightforward nature makes it especially appealing for addressing time-sensitive financial obligations.

One of the primary reasons people choose term life insurance is for debt protection. For instance, if you have a significant business loan or a mortgage on a secondary property, a term policy ensures that these debts don’t become a burden on your estate. The death benefit, paid as a tax-free lump sum, goes directly to your named beneficiaries. This not only bypasses probate but also avoids provincial fees. By doing so, it helps preserve your wealth and keeps your estate intact, even in unexpected situations.

As Nizam Shajani, CPA, CA, TEP, LL.M (Tax) of Shajani CPA puts it:

"Term insurance is best used when you need short-term coverage (e.g., during business expansion or while paying off a mortgage)."

Term life insurance is also a valuable tool for business continuity planning. It’s commonly used to fund buy-sell agreements, ensuring that surviving partners can purchase a deceased partner’s shares without putting a strain on the company’s cash flow. Additionally, it mitigates key-person risk during critical growth phases, providing financial stability until a permanent succession plan is established. If a corporation owns the policy and is the beneficiary, the premiums are not considered a taxable benefit to the shareholder. This makes term insurance a targeted and efficient way to address specific business needs while preparing for unexpected transitions.

Another advantage of term policies is their conversion options, which provide added flexibility. Most term policies allow for conversion to permanent insurance - such as whole or universal life - without requiring new medical underwriting. This feature ensures that even if your health changes, you can still secure long-term coverage to meet evolving estate planning goals. However, policies with coverage exceeding $5 million typically involve detailed medical and financial underwriting.

In short, term life insurance offers a tailored approach for addressing short-term financial obligations while maintaining the flexibility to adapt to future needs.

4. Corporate-Owned Life Insurance for Business Owners

Canadian business owners have a strategic option to grow their corporate funds while minimizing taxes: corporate-owned life insurance (COLI). Instead of keeping surplus corporate funds in taxable passive investments, these can be redirected into an exempt permanent life insurance policy. This approach not only allows the funds to grow tax-deferred but also helps preserve corporate capital and secure wealth for shareholders.

One of the standout benefits of COLI is the tax-free death benefit received by the corporation when the insured passes away. What makes this especially useful is how it enhances corporate financial planning. The portion of the death benefit that exceeds the policy's adjusted cost basis (ACB) is credited to the Capital Dividend Account (CDA). From there, the corporation can pay out tax-free capital dividends to Canadian-resident shareholders. Varun Sehgal, CPA of Think Accounting, explains it clearly:

"The CDA credit related to insurance is the death benefit minus the policy ACB immediately before death."

Another important advantage of COLI is its role in protecting the Small Business Deduction (SBD). Passive investment income over $50,000 annually reduces eligibility for the SBD, but gains within a life insurance policy are excluded from this calculation. This ensures the corporation retains access to lower tax rates. Alison Hughes, Director of National Distribution at Lawyers Financial, highlights this point:

"Gains inside a permanent life insurance policy aren't considered passive income, so there's no impact on your small business deduction."

The potential financial benefits are significant. For example, BMO Life Assurance Company estimated that allocating $500,000 of corporate surplus into COLI could result in a net after-tax estate advantage of nearly $1 million over 20 years.

Beyond tax savings, COLI is also a key tool for business continuity planning, particularly for funding buy-sell agreements. When a business partner passes away, surviving partners often need immediate funds to buy out the deceased’s shares without disrupting the business or involving outside parties. As Faran Umar-Khitab, Partner at Gowling WLG, explains:

"The surviving partner of a closely held small business may not want a third party or the deceased's family members to step in... Using life insurance proceeds to buy out the shares often makes sense."

To maximize the benefits of COLI, the corporation must both own the policy and be the named beneficiary. This setup avoids triggering a shareholder benefit. Additionally, businesses must file Form T2054 with the CRA and confirm the policy’s ACB with the insurer to avoid a steep 60% penalty tax on overstated CDA balances. Given the complexities involved, working with a licensed insurance advisor, CPA, and legal counsel is crucial for proper implementation.

5. High-Net-Worth Property and Casualty Coverage

After discussing strategies for life and corporate insurance, it’s equally important to focus on protecting physical assets through specialized property and casualty insurance.

Standard home and auto policies work fine for most households but often fall short when it comes to high-value assets. For instance, a typical homeowner’s policy might cap jewellery coverage at $2,500, whereas a high-net-worth (HNW) policy could remove that limit entirely. As Miller Insurance Brokers puts it:

"High net worth insurance isn't simply a variation on ordinary personal insurance with higher coverage limits and higher premiums. Instead, it's about recognizing that people with large assets have unique needs."

Unlike standard policies, which factor in depreciation when paying out claims, HNW policies offer agreed-upon values for vehicles and uncapped replacement costs for homes. This ensures that in the event of a total loss - whether it’s a collector car or a fire-damaged estate - there’s no dispute over depreciation. For homes valued between $1,500,000 and $10,000,000 in Canada, these policies guarantee the property can be rebuilt to its original specifications with no cap on costs. Some even waive deductibles entirely for losses exceeding $50,000.

HNW policies also extend coverage to items like fine art, rare wine, jewellery, and watches. These scheduled floaters account for risks such as appreciation, transit, and storage - essential for collectors, with two-thirds of HNW collections valued above $500,000. For luxury vehicles, policies may allow you to choose your repair shop and ensure factory-original parts are used. Additionally, properties held in trust - a common estate planning tool for affluent Canadians in Alberta - can be explicitly named in the policy.

This type of insurance plays a crucial role in wealth preservation by preventing the need to sell off assets to cover unexpected losses. Adam Hoopes, CFP®, of Creative Planning, highlights this point:

"Insurance shouldn't exist in isolation, especially for high-net-worth individuals. When strategically coordinated with your wealth, estate and tax planning, coverage can offer better protection and value."

Here’s a quick comparison of standard and HNW policies:

| Feature | Standard Policy | High-Net-Worth Policy |

|---|---|---|

| Home Valuation | Actual Cash Value or capped replacement | Guaranteed Replacement Cost (uncapped) |

| Auto Valuation | Actual Cash Value (market value) | Agreed Value (set upfront) |

| Jewellery & Art Limits | Typically around $2,500 | Higher limits or eliminated entirely |

| Deductibles | Always applicable | Waived for large losses (e.g., >$50,000) |

| Liability Limits | Typically $1M–$2M | Often $5M–$50M+ |

| Claims Handling | Standard adjusters | Dedicated specialists; client's choice of shop |

To ensure your assets are fully protected, make it a habit to review your coverage with wealth and estate advisors regularly.

6. Umbrella and Excess Liability Insurance

High-net-worth property insurance is great for protecting physical assets, but it often falls short when it comes to covering legal or financial risks. That’s where umbrella and excess liability insurance come in - they act as a safety net, stepping in once the limits of your primary policies are reached.

In Canada, standard home and auto insurance policies typically cap liability coverage at $1 million to $2 million. While that might sound like a lot, it can be quickly drained in a serious legal dispute:

"With standard insurance policies typically capping at a $1 million liability limits, they often aren't enough to provide full asset protection in the event of a costly lawsuit, where you may be sued up to, and even beyond, your total net worth."

For high-net-worth individuals, umbrella policies can extend liability coverage from $1 million all the way up to $100 million. Experts recommend setting your umbrella limit to match your total net worth, including any income you expect to earn in the future. The cost? The first $1 million of coverage typically ranges from $300 to $500 annually, with lower incremental costs for each additional million.

These policies don’t just increase limits - they also cover risks that standard insurance often excludes. Think libel, slander, defamation, or even false arrest. And they’re not limited to Canada; umbrella insurance usually offers global protection, which is a big plus for frequent travellers or those with properties abroad. Legal defence costs - like lawyer fees, court expenses, and settlement negotiations - are also generally included, even if the lawsuit has no merit.

It’s also key to know the difference between umbrella and excess liability insurance. Umbrella policies provide broader coverage, filling gaps in your existing policies. Excess liability, on the other hand, simply increases the limits on risks already covered.

| Household Risk Profile | Common Umbrella Limits |

|---|---|

| Emerging High Net Worth | $1M – $5M |

| Established High Net Worth | $5M – $10M |

| Ultra High Net Worth | $10M – $100M+ |

Source: Wheeler & Taylor

This kind of extended liability insurance is an essential part of any wealth preservation plan. For households with domestic staff, it’s especially important to ensure that your umbrella policy includes coverage for employee-related liabilities.

7. Travel and Global Health Coverage for Affluent Canadians

When domestic health plans fall short, premium global coverage steps in to meet the needs of affluent Canadians who spend significant time abroad. Whether you're a snowbird escaping the winter, a business executive travelling for work, or an expatriate living overseas, standard provincial health coverage won't cut it. It doesn't cover things like specialist consultations, private hospital rooms, or complex medical procedures. As David Eline, Founder of Riviera Expat, puts it:

"For a high-net-worth professional operating on a global scale, a standard domestic health insurance policy is not merely insufficient; it is a significant, unacknowledged liability within your personal portfolio."

Just as you would protect your home or other assets with specialized insurance, premium travel coverage ensures your health and mobility are safeguarded across the globe.

International Private Medical Insurance (IPMI) and premium travel plans address these gaps. Providers like Manulife and TD Insurance offer emergency medical benefits of up to CA$10 million per insured person. Meanwhile, Cigna's Platinum global plan goes even further, offering "Paid in Full" coverage for private hospital rooms, surgeons' fees, and intensive care without any per-claim limit. These plans provide access to any doctor or hospital worldwide and include concierge-level services to handle hospital admissions, medical travel, and even access to "Elite Navigator" physician advocates. For non-emergency situations, Cigna Global also offers 24/7 multilingual support and telehealth services through Teladoc.

That said, including the United States in your coverage area can significantly raise premiums - often by 40% to 60%. If you rarely visit the U.S., excluding it from your plan can help keep costs manageable.

This type of global coverage complements a well-rounded estate strategy, ensuring you're protected no matter where you are.

| Feature | Standard Travel Insurance | Premium Global Health (IPMI) |

|---|---|---|

| Emergency Medical Limit | Typically CA$1M–CA$5M | Up to CA$10M or "Paid in Full" |

| Hospital Room | Semi-private or ward | 100% private room coverage |

| Provider Choice | Limited to emergency facilities | Any doctor or hospital, worldwide |

| Routine & Specialist Care | Not included | Included (diagnostics, wellness, specialists) |

| Evacuation & Repatriation | Basic medical transport | Full evacuation, crisis response, companion travel |

| Billing | Reimbursement required | Direct billing |

For frequent travellers, multi-trip annual plans are a practical choice. These plans cover unlimited trips within a year, with individual trip durations of up to 60 or 100 days, depending on the provider. If you're planning to stay abroad for longer, single-trip plans can provide coverage for up to 365 days.

8. Specialty Coverage for Luxury Assets

When it comes to protecting high-value possessions, standard home insurance often falls short. Most policies cap coverage for jewellery and artwork at CA$5,000–CA$10,000 - far below the needs of affluent Canadians. For items like fine art, luxury watches, collector vehicles, yachts, or private wine cellars, specialized insurance is a must.

"Standard insurance policies simply aren't enough. If your home is valued over $1.5 million, or you own luxury vehicles, fine art, jewellery, or multiple properties, you need High Net Worth Insurance." - AIM Insurance

One standout feature of these policies is Agreed Value coverage. Unlike standard insurance, which pays out a depreciated amount, Agreed Value ensures you receive the full pre-determined amount in the event of a total loss - no depreciation involved. Some premium policies even offer payouts of up to 150% of the item's appraised value.

To stay properly insured, schedule appraisals every three to five years. This is especially important for items like jewellery, where rising gold prices can leave collections underinsured. Use certified appraisers from recognized organizations like the International Society of Appraisers or the Canadian Jewellers Association. For fine art, appraisals should include details about the artist, provenance, condition, and comparable sales data.

Specialty policies also provide coverage for unique risks such as mysterious disappearance, damage during transit, or even wine spoilage. Plus, they offer worldwide protection - whether your assets are displayed in a gallery, in transit, or stored at a secondary property. Premiums usually range from 1% to 3% of the appraised value, depending on the asset type and security measures in place.

Another smart move is keeping a detailed digital inventory of your assets. Include high-resolution photos, purchase receipts, serial numbers, and certificates of authenticity, and back everything up in secure cloud storage.

| Feature | Standard Home Insurance | Specialty Luxury Policy |

|---|---|---|

| Jewellery/Art Limits | CA$5,000–CA$10,000 | High limits; scheduled or blanket options |

| Valuation Method | Actual Cash Value (depreciated) | Agreed Value – no depreciation |

| Market Appreciation | Not covered | Up to 150% of itemized value |

| Deductibles | Standard deductible applies | Often CA$0 for scheduled items |

| Geographic Scope | Primarily on-premises | Worldwide, including transit |

| Loss Types Covered | Theft, fire | All-risk, including mysterious disappearance |

| New Acquisitions | Must be added immediately | 90-day automatic coverage window |

Specialty coverage is an important part of broader wealth management strategies, often coordinated through private bankers in British Columbia or other provinces, ensuring that your most prized possessions are protected no matter where they are or what risks they face.

Comparison Table

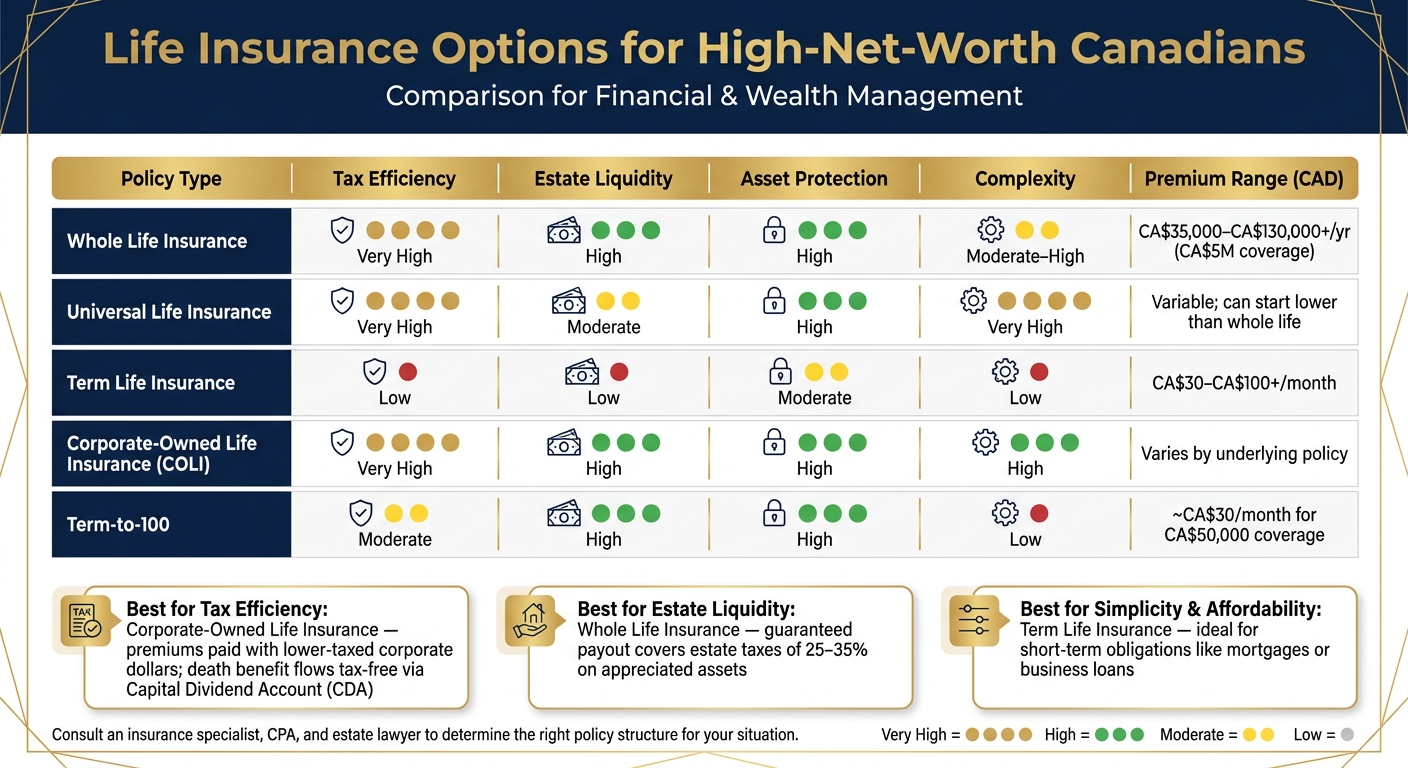

Life Insurance Options for High-Net-Worth Canadians: Policy Comparison

Here’s a quick look at different life insurance options for high-net-worth Canadians. This table highlights the key features of each policy type, focusing on areas like tax efficiency, estate liquidity, asset protection, complexity, and premium costs. It’s a handy summary to complement the details provided earlier.

| Policy Type | Tax Efficiency | Estate Liquidity | Asset Protection | Complexity | Premium Range (CAD) |

|---|---|---|---|---|---|

| Whole Life | High - tax-deferred growth + CDA access | High - guaranteed payout, no market risk | High - bypasses probate, creditor-shielded in trust | Moderate to High | CA$35,000–CA$130,000+/year for CA$5M coverage |

| Universal Life | High - investment-linked growth + CDA | Moderate - lapse risk if investments underperform | High - bypasses probate | Very High | Variable; can start lower than whole life |

| Term Life | Low - death benefit only, no cash value | Low - expires after term | Moderate - bypasses probate if beneficiary named | Low | CA$30–CA$100+/month for basic coverage |

| Corporate-Owned | Very High - pre-tax funding with tax-free CDA distribution | High - funds buy-sell agreements and estate taxes | High - supports business continuity | High | Varies by underlying policy (whole life or UL) |

| Term-to-100 | Moderate - permanent coverage, no cash surrender value | High - lifelong payout guaranteed | High - bypasses probate | Low | ~CA$30/month for CA$50,000 coverage |

Some key takeaways: Corporate-owned life insurance stands out for tax efficiency. Premiums are paid using lower-taxed corporate funds, and the death benefit flows through the Capital Dividend Account (CDA) tax-free to shareholders. Meanwhile, whole life insurance is a solid choice for estate liquidity. Its guaranteed payout ensures funds are available to cover estate taxes, which can hit 25–35% of appreciated asset values upon death.

Universal life insurance provides flexibility but requires active management to avoid issues like lapse risk. As Michael Bogress from Bogress Financial Group explains:

"For high‑net‑worth business owners, properly structured life insurance can be an integral part of corporate tax and estate planning... the benefits are highly dependent on structure, funding design, and coordination with legal and tax advisors."

On the other hand, term life insurance is the simplest and most affordable option. However, it’s better suited for short-term needs rather than long-term estate planning. For permanent wealth transfer goals, the added complexity of whole life or corporate-owned policies is usually worth considering.

Conclusion

The policies discussed earlier highlight how tailoring your insurance strategy is key to protecting and growing your wealth. The right choice depends on factors like your asset mix, corporate structure, and long-term legacy plans. Each policy serves a distinct purpose, and taking a close look at your overall financial situation is an essential first step.

Insurance, in this context, acts as a financial tool that shields growth from taxes, addresses estate liabilities, and ensures a smooth transfer of wealth. Without proper planning, the consequences can be steep - capital gains taxes alone can claim 25–35% of your appreciated asset values at the time of death.

The structure of your plan is as important as the product itself. To align your insurance strategy with your corporate structure, will, and shareholder agreements, it’s crucial to consult a combination of experts. An insurance specialist, CPA, and estate lawyer each bring unique expertise to the table, and no single professional can address all these aspects alone.

For those seeking qualified professionals, Find Wealth Experts and Private Bankers in Canada provides a province-by-province listing of private bankers and wealth specialists. By connecting with these experts, you can receive personalized advice tailored to your specific needs.

FAQs

Whole life or universal life - which fits my estate plan best?

Choosing between whole life insurance and universal life insurance comes down to whether you value stability or adaptability in your estate planning.

Whole life insurance is designed for those who prefer consistency. It features fixed premiums and steady cash value growth, making it a solid choice for long-term, predictable coverage. On the other hand, universal life insurance offers more flexibility. With adjustable premiums and investment opportunities, it’s better suited for individuals whose financial needs and goals may change over time. However, it does require ongoing attention to manage effectively.

How does corporate-owned life insurance pay out tax-free to shareholders?

When a corporation receives a life insurance death benefit, the amount is generally not subject to tax. To pass these funds along to shareholders residing in Canada, the corporation calculates a credit to its Capital Dividend Account (CDA). This is done by subtracting the policy's adjusted cost basis (ACB) from the death benefit. The credited portion can then be distributed as tax-free capital dividends, offering an effective way to transfer wealth. It's always wise to seek professional advice on handling these tax elections.

How much umbrella liability coverage do I actually need?

When determining how much umbrella liability coverage to carry, a solid rule of thumb is to match it to your total net worth. This ensures your assets are protected in case of a major claim. For added peace of mind, higher coverage limits are often suggested to guard against risks like future income garnishment.

Think about what you own - your home equity, investments, or other assets - and what liabilities you might face, such as owning multiple properties or having teenage drivers on your policy. The good news? Increasing your coverage typically comes at a reasonable cost. That’s why many high-net-worth Canadians opt for umbrella policies ranging anywhere from $1 million to $100 million.