Interest rates influence almost every aspect of financial planning, from investment returns to borrowing costs and retirement strategies. For Canadians, even small changes in rates can have a ripple effect on portfolios, cash flow, and long-term wealth goals. Here’s what you need to know:

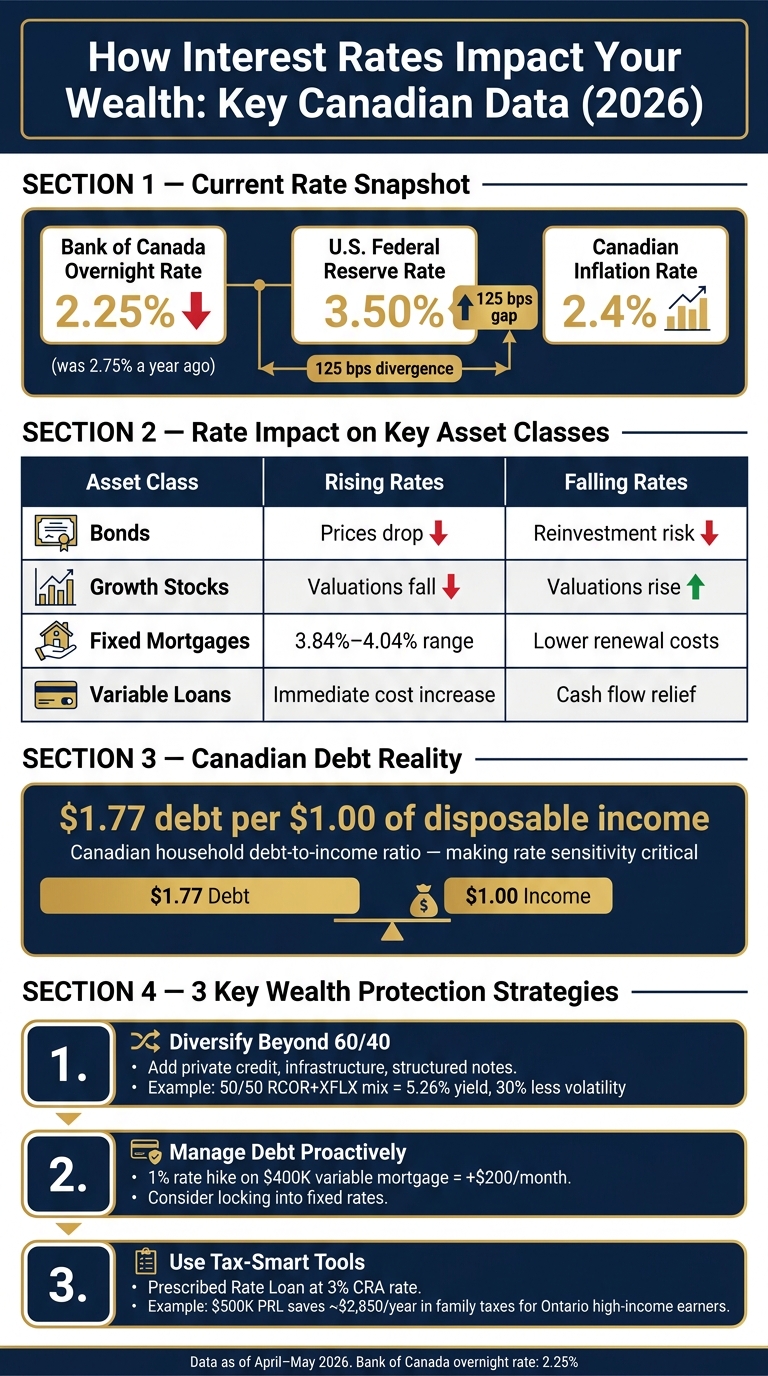

- Bank of Canada Rate: As of April 29, 2026, the overnight rate is 2.25%, down from 2.75% a year ago. Inflation sits at 2.4%.

- Mortgage Rates: Fixed mortgage rates are climbing, ranging between 3.84% and 4.04%, driven by higher bond yields.

- Currency Impact: A 125-basis-point gap between U.S. and Canadian rates (3.50% vs. 2.25%) affects the Canadian dollar (US$0.73), impacting cross-border portfolios.

- Investment Challenges: Rising rates lower bond prices and growth stock valuations, while falling rates introduce reinvestment risk for conservative investors.

- Borrowing Costs: Variable-rate products and mortgage renewals are becoming more expensive, affecting cash flow and debt strategies.

- Retirement and Estate Planning: Rate changes influence annuity pricing, estate freezes, and intergenerational wealth transfers.

Key Strategies to Manage Rate Fluctuations:

- Diversify: Go beyond traditional stock-and-bond portfolios by including private credit, infrastructure, or structured notes.

- Manage Debt: Prioritize paying down variable-rate loans or consider switching to fixed rates for stability.

- Revisit Plans: Use tools like laddered GICs and prescribed rate loans to adjust retirement and estate strategies.

With Canadian households carrying $1.77 in debt for every dollar of disposable income, reviewing and adjusting financial plans regularly is essential to stay ahead of rate changes. Working with private bankers in Alberta or other provinces can help align your investments, borrowing, and estate plans to navigate this evolving landscape.

How Interest Rates Impact Your Wealth: Key Canadian Financial Data (2026)

Practical Planning Tip: Retirement and Falling Interest Rates - Part 1

sbb-itb-e9c03dd

Challenges of Fluctuating Interest Rates

Fluctuating interest rates create unique challenges for high-net-worth Canadians. With significant capital spread across various asset classes, borrowing arrangements, and long-term strategies, these individuals often feel the effects more acutely.

Volatility in Investment Returns

Interest rate changes can shake up investment returns. For instance, when rates rise, bond prices drop. This happens because new bonds offer higher yields, making older ones less appealing in the market. Similarly, higher rates reduce the value of future earnings, which can weigh heavily on growth and technology stocks. A clear example of this was seen in Q1 2026: while the S&P 500 fell 4.3%, the S&P/TSX Composite gained 3.88%. This contrast highlights how Canada's market, with its focus on energy, materials, and financials, often fares better during rising-rate periods.

On the flip side, conservative investors face a different hurdle when rates drop. Maturing GICs and short-term investments must be reinvested at lower yields, creating reinvestment risk. This issue was particularly evident in early 2026, when credit markets offered tight spreads, leaving little reward for taking on corporate risk.

"Now's not the time to take the big duration bets. Now's not the time to kind of go too far down the risk spectrum where you're not getting paid to take on more risk." - Naveed Sunderji, Portfolio Manager, Franklin Templeton Fixed Income

These changes in investment returns also ripple through borrowing strategies.

Rising Borrowing Costs

For affluent Canadians leveraging debt, fluctuating rates can disrupt cash flow. Those with variable-rate products feel the pinch immediately, while borrowers nearing renewal face a steeper adjustment. For example, 5-year mortgage rates currently hover around 5.05%.

Higher borrowing costs also reduce the attractiveness of leverage-based strategies, such as the Smith Manoeuvre, by cutting into net returns. Chad Harmer, Founder of Harmer Wealth Management, explains:

"A mortgage is not just a rate decision. It is a cash flow decision, a flexibility decision and sometimes a risk-management decision."

Business owners face additional hurdles, as tighter lending conditions can restrict access to capital just when opportunities arise. These borrowing challenges inevitably influence long-term financial planning.

Effects on Retirement and Estate Planning

Interest rate changes also reshape retirement and estate strategies. For retirees, shifting yields can affect withdrawal plans, alter annuity pricing, and impact financing costs tied to estate freezes. Families relying on fixed income from their portfolios may need to revisit their assumptions more frequently to account for these changes.

Cross-border wealth strategies become even trickier due to the rate gap between countries. Differences in estate valuations, income streams, and asset distributions can complicate intergenerational transfers.

"For cross-border clients, ignoring the rate gap is the same as ignoring the foundation of your portfolio." - Shiraz Ahmed, CEO and Portfolio Manager, Sartorial Wealth

Real estate, often held as a legacy asset, faces its own set of challenges. Properties financed with debt must generate enough rental income to cover rising debt-servicing costs. If they don't, the broader estate plan could be at risk. Gloria DiGiovanni, Managing Director at RBC Private Banking, emphasizes:

"Decisions around real estate investing shouldn't be made in isolation. Viewing and co-ordinating these investments in the context of a family's total wealth picture helps ensure real estate complements rather than conflicts with long-term planning."

Ways to Protect Wealth When Rates Change

Protecting your wealth when interest rates fluctuate means staying ahead with smart strategies. Beyond managing investment returns and borrowing costs, there are several ways to safeguard and optimize your financial position.

Diversification and Asset Allocation

Diversifying your portfolio isn’t just about spreading risk - it’s about creating opportunities. Traditional 60/40 stock-and-bond portfolios may no longer cut it in today’s rate environment. Adding alternative assets like private credit, infrastructure, and liquid alternatives can help reduce your portfolio's sensitivity to rate changes. Infrastructure, in particular, stands out for its long-term, inflation-linked cash flows.

"A 60-40 portfolio still makes sense as a foundation. But diversification today means going beyond just stocks and bonds." - Yuko Girard, Portfolio Manager, Dynamic Funds

Expanding globally is another way to reduce rate sensitivity. As Dagmara Fijalkowski, Head of Global Fixed Income and Currencies at RBC Global Asset Management, explains:

"Investors can benefit from accessing global markets, as not all move in lockstep."

Here’s a practical example: In May 2026, RBC iShares advisors combined the RBC Core Bond Pool ETF (RCOR) with the iShares Flexible Monthly Income ETF (XFLX). This 50/50 mix delivered a 5.26% yield to maturity as of March 31, 2026 - about 40% higher than the FTSE Canada Universe Bond Index - while cutting volatility by 30% through diversification across Canadian, U.S., and international holdings. For those wary of capital risks tied to government bonds, structured notes are another option. In April 2026, TriVest Wealth Management replaced more than 50% of their Canadian government bond exposure with structured notes, including leveraged upside notes with strong downside barriers, to avoid the 10–12% capital loss risk tied to normalizing bond yields.

These diversification strategies naturally complement managing borrowing costs in an unpredictable rate environment.

Managing Borrowing Costs

When interest rates are unpredictable, how you manage your debt becomes just as important as your investments. For those with variable-rate loans - like HELOCs, personal lines of credit, or variable mortgages - prioritizing paying down principal on the most rate-sensitive balances is key. For instance, a 1% rate hike on a $400,000 variable-rate mortgage could mean an extra $200 per month in interest.

Switching to a fixed-rate loan is another option to consider. With Canada’s 5-year mortgage rate hovering around 5.05% in May 2026, fixed rates now offer competitive advantages. Locking in a fixed rate not only stabilizes your payments but also eliminates the stress of tracking rate announcements from the Bank of Canada.

Maintaining liquidity is equally important. Having accessible funds ensures you avoid high-cost borrowing when unexpected expenses or opportunities arise. Business owners, in particular, should review debt structures to maximize interest tax deductibility. A private banking advisor can often identify overlooked opportunities to restructure debt effectively.

Adjusting Retirement and Estate Plans

Changing rates also mean rethinking retirement and estate strategies. Fixed, long-term plans often need adjustments to stay aligned with current conditions. Incorporating laddered GICs and trust structures can provide the flexibility needed.

Laddered GICs are a straightforward way to adapt. By staggering maturity dates across one to five years, you can consistently reinvest a portion of your funds at potentially higher rates without locking everything in at once.

A Prescribed Rate Loan (PRL) is another tool for tax-efficient planning. As of early 2026, the CRA prescribed rate is 3%. Once set, this rate is locked for the life of the loan. For example, a high-income earner in Ontario (with a 53.5% marginal tax rate) lending $500,000 to a lower-income spouse at 3% could save around $2,850 annually in family taxes compared to holding the investments directly.

"The wealthiest Canadian families don't pay more tax than necessary. They structure their affairs thoughtfully using legitimate tools available under the law. Prescribed rate loans are one of those tools." - Canaccord Genuity Wealth Management

One crucial detail: the annual interest payment on a PRL must be made by January 30 each year without exception. Missing this deadline - even by a day - voids the income-splitting benefits. Automating the transfer can eliminate this risk entirely.

Finally, tools like trust structures and permanent life insurance can help wealth grow tax-free and transfer to the next generation outside of probate. These strategies are most effective when integrated into a comprehensive plan, rather than treated as standalone solutions.

Why Working with a Private Banking Expert Matters

Laddered bonds, prescribed rate loans, and trust structures only reach their full potential when they function together seamlessly. That’s where the expertise of a private banking professional becomes invaluable.

Coordinating with Financial Specialists

A private banker serves as your go-to person, bringing together portfolio managers, credit advisors, and estate planners to create a well-rounded financial plan. For example, when the Bank of Canada adjusts its policy rate - set at 2.25% as of April 29, 2026 - the changes can ripple through your mortgage, bond investments, business loans, and estate planning. Without someone monitoring the overall picture, an adjustment in one area could unintentionally disrupt another. A unified approach helps avoid these pitfalls while strengthening your financial strategy as a whole.

For clients dealing with cross-border finances, the 125-basis-point gap between the Bank of Canada and the U.S. Federal Reserve (3.50%) as of May 2026 adds an extra layer of complexity. This difference impacts not only bond allocations and mortgage structures but also the purchasing power of cross-border income and the valuation of estates. Shiraz Ahmed, CEO and Portfolio Manager at Sartorial Wealth, highlights the importance of addressing such challenges:

"For cross-border clients, ignoring the rate gap is the same as ignoring the foundation of your portfolio."

Private banking teams operate under a fiduciary duty, meaning their advice must align with your best interests - not tied to specific products or sales targets. This impartiality is crucial when navigating complex financial decisions influenced by fluctuating rates.

Finding Local Expertise in Canada

Rate changes don’t affect all parts of Canada equally. For instance, an energy sector slowdown in Alberta creates different challenges than a real estate dip in Vancouver or Toronto. Local private banking professionals are well-versed in these regional nuances and can adapt your plan to reflect your area’s unique conditions.

Canada’s major banks have regional leadership teams across British Columbia, the Prairies, Ontario, Quebec, and Atlantic Canada to address these local differences. For example, Alberta’s Small Business Deduction grind presents challenges for incorporated professionals that require advisors with an in-depth understanding of provincial regulations, not just national policies. By tapping into local expertise, you ensure your financial strategy isn’t just solid on paper but also tailored to the realities of your region.

If you’re ready to connect with a professional in your area, Find Wealth Experts and Private Bankers in Canada provides a directory of specialists organized by province. This is a great resource for finding someone who understands both your financial goals and your local context.

Conclusion: Managing Rate Volatility with a Clear Plan

Interest rate changes don’t have to throw your financial plans off track, but they do call for deliberate action. The strategies discussed - like laddered bonds, diversified asset allocation, and prescribed rate loans - are only effective if you revisit and adjust them regularly.

With Canadian households carrying $1.77 in debt for every dollar of disposable income, even small rate changes can significantly affect cash flow, debt repayment, and long-term financial goals. Neglecting a structured review process can lead to portfolios veering off course, rising debt costs, and missed tax-saving opportunities.

DO Financial Canada emphasizes the importance of this approach:

"Lasting wealth security is not achieved by chance - it is the result of deliberate, strategic action. One of the most critical actions you can take is to conduct a thorough annual investment review."

To stay ahead of rate volatility, it’s crucial to make regular reviews a habit. Evaluate your risk-adjusted returns, debt structure, tax strategies, and liquidity needs at least once a year. With the Bank of Canada's overnight rate sitting at 2.50% as of May 2026, and monetary policies diverging from those in the U.S., financial conditions can shift quickly, making even a year-old plan feel outdated.

FAQs

Should I switch my mortgage from variable to fixed?

Deciding between a fixed and variable mortgage comes down to your comfort with risk and your financial circumstances. Fixed-rate mortgages offer predictable payments, making them a safer option if you’re on a tight budget or prefer stability. On the other hand, variable-rate mortgages tend to have lower rates historically but come with the possibility of payment increases, requiring a bit more financial flexibility.

If you’re unsure, you might consider a shorter fixed term, like three years. This gives you the security of stable payments for a while, while still leaving room to reassess your options sooner. For personalized guidance, it’s always a good idea to speak with a financial advisor.

How can I reduce bond losses when rates rise?

To reduce the risk of bond losses when interest rates climb, it's wise to concentrate on shorter-duration bonds, as they react less to rate fluctuations. A laddered bond strategy can also help by allowing you to reinvest proceeds from maturing bonds into new ones with higher yields. Look into high-quality corporate bonds with shorter terms, and make sure the bond durations match your cash flow requirements. This approach can help you avoid selling bonds at a loss during periods of market uncertainty.

What should I change in my retirement or estate plan when rates move?

When interest rates shift, it's a good time to review your retirement and estate plans to make sure they still align with your goals. Test your financial strategy against different rate scenarios to see how changes might affect your cash flow, income, and any outstanding debts.

For fixed-income investments, rising rates could make options like GICs or bonds more appealing, while lower rates might reduce borrowing costs. In terms of estate planning, consider how fluctuations in rates can influence the value of your assets and liabilities, and adjust your plans to reflect the current financial landscape.