Canada is undergoing a massive shift in wealth transfer, with Baby Boomers passing on assets to younger generations. This process isn't just about money - it's also about values, family governance, and philanthropy. Here's what you need to know:

- Wealth Transfer Trends: Over 4.4 million Canadian families have a net worth exceeding $1M, with $10M+ in assets for 108,000 families. Real estate, investments, and business equity form the bulk of these assets.

- Philanthropy Focus: Despite a national decline in charitable giving, high-net-worth families are increasing donations, prioritizing health, social justice, and education.

- Generational Differences: Older generations focus on legacy, while younger ones value measurable social impact and favour impact investing.

- Tax-Efficient Giving: Strategies like donating securities or using Donor-Advised Funds (DAFs) help families maximize giving while minimizing taxes.

- Family Governance: Open communication and shared goals are key to aligning wealth transfer and philanthropic plans across generations.

Planning early and working with private bankers in Alberta or other experts ensures your family's wealth and values are preserved for future generations.

Canada's Great Wealth Transfer: Key Stats & Philanthropy Trends 2023–2026

The Great Canadian Wealth Transfer: What the Data Shows

Scale and Timeline of Wealth Transfer

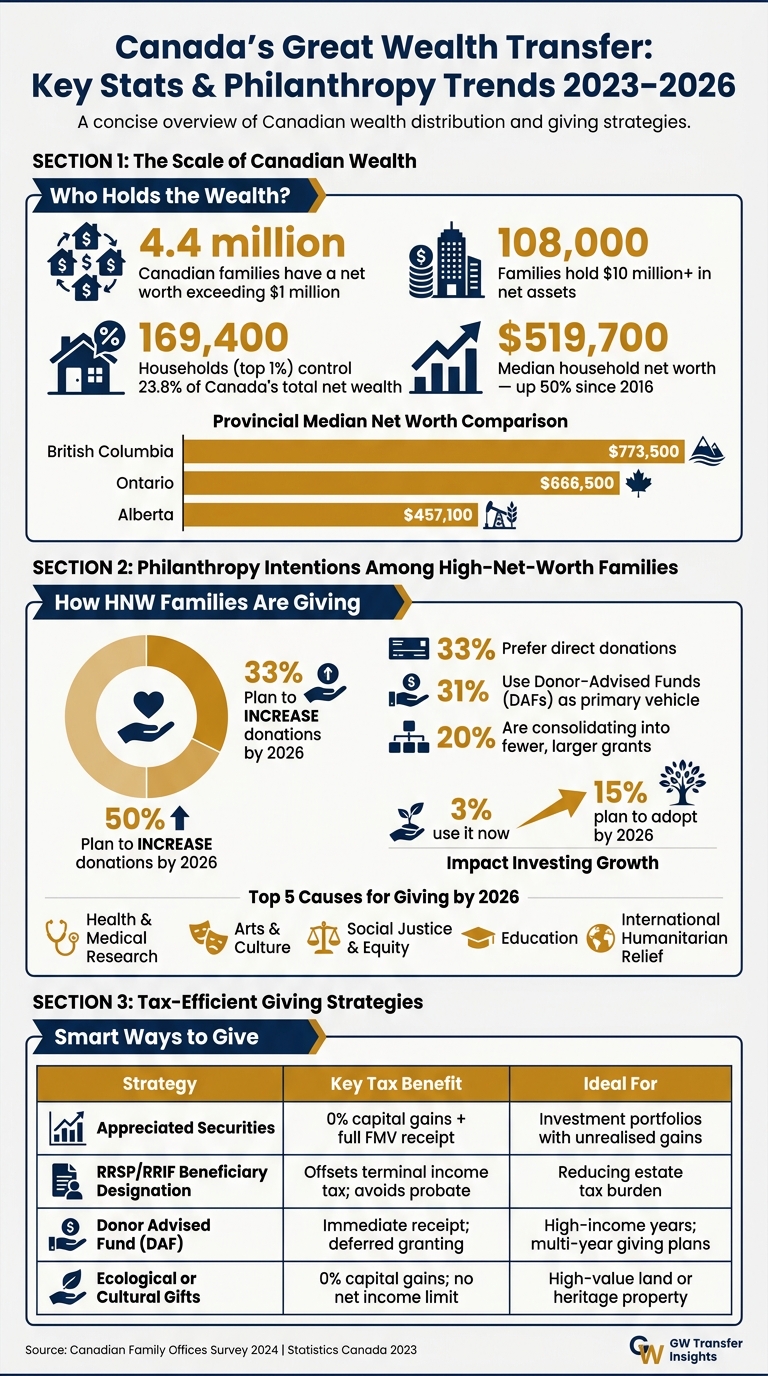

Canada is on the brink of a massive wealth transfer, with numbers that are hard to ignore. As of 2023, 4.4 million Canadian families had a net wealth exceeding $1 million. Meanwhile, the top 1% of economic families - around 169,400 households - held 23.8% of the nation’s total net wealth, with each family boasting at least $7.4 million in net assets. At the very top tier, approximately 108,000 families surpassed the $10 million mark in net wealth.

The median household net worth across Canada in 2023 stood at $519,700, reflecting a remarkable 50% increase in real wealth since 2016. As this wealth grows, a significant portion is already making its way to younger generations.

What Types of Wealth Are Being Transferred

When it comes to transferring wealth, the composition of assets varies significantly between families. For many established Canadian households, home equity makes up a large portion, averaging $283,400, or about 35% of total wealth. Similarly, private pension assets - including Registered Pension Plans (RPPs) and RRSPs - account for 36% of their wealth.

In contrast, high-net-worth families tend to hold a greater share of their wealth in business equity and non-pension financial assets, such as investment portfolios and private holdings. These asset types come with unique challenges, particularly when it comes to estate planning. Taxes and liquidity requirements differ depending on the asset, creating complexities that families must navigate. Regional factors and succession planning also add layers of consideration, as discussed further below.

Factors Specific to Canada

Canada’s geography plays a major role in shaping the scale and distribution of wealth transfers. British Columbia leads the provinces with a median household net worth of $773,500, followed by Ontario at $666,500 and Alberta at $457,100. This concentration of wealth, often tied to high real estate values, means urban centres in these regions will see the most significant impacts from wealth transfers.

Business succession is another critical factor. As Jock Finlayson, Chief Economist at ICBA, explains:

"Age is a key driver. As people grow older, they generally acquire assets such as homes and retirement savings, which rise in value over time. They also pay down debt, notably mortgages."

The numbers back this up: nearly 61% of Canadian small- and medium-sized business owners are aged 50 or older, and about one in five plans to exit their business within the next five years. Interestingly, more of these exits are now happening through third-party sales rather than traditional family transfers. This shift has significant implications for how business wealth is integrated into estate and philanthropic planning.

These trends highlight the importance of strategic planning as Canadian families prepare to pass on their wealth to the next generation. The integration of philanthropy into these plans is becoming an increasingly important consideration.

sbb-itb-e9c03dd

How Canadian Families Are Adding Philanthropy to Wealth Transfer Plans

Current Trends in Donor Intentions

As charitable giving declines across Canada, a notable trend emerges among high-net-worth (HNW) and ultra-high-net-worth (UHNW) families: half of them plan to increase their donations by 2026, with 10% expecting to make a substantial jump. This aligns with last year's findings, where 90% of respondents indicated no plans to reduce their contributions in 2025.

The focus of giving is shifting, too. By 2026, the top five causes expected to dominate donations include health and medical research, arts and culture, social justice and equity, education, and international humanitarian relief. Notably, social justice and equity have risen in importance, now ranking among the top three priorities. Meanwhile, support for climate and environmental causes has waned, with only 9% of respondents naming it a key focus.

Common Giving Structures Used in Canada

For 33% of HNW donors, direct donations remain the preferred method of giving. However, donor-advised funds (DAFs) are quickly gaining traction, with 31% of donors choosing them as their primary vehicle. Nearly one-third of donors also plan to expand their use of DAFs by 2026.

"Donor-advised funds (DAFs) have become among the largest and most important giving vehicles in the Canadian philanthropic landscape, and our survey confirms that reality." - Joe Chidley, Managing Editor, Canadian Family Offices

DAFs are especially appealing for their convenience, allowing families to make a single contribution while retaining the ability to allocate grants to various charities over time. Alongside DAFs and direct donations, unrestricted giving is growing in popularity. This approach entrusts organizations to use funds where they are most needed, rather than tying them to specific purposes.

Another trend is grant consolidation, with 20% of donors shifting towards making fewer but larger grants instead of multiple smaller ones.

"Among those who shifted strategy, there was a clear trend towards fewer, larger grants, cited by one in five respondents." - Joe Chidley, Managing Editor, Canadian Family Offices

These evolving giving strategies reflect deeper generational changes in how philanthropy is approached.

How Giving Goals Differ Across Generations

The shift in giving methods mirrors broader generational differences in wealth transfer and philanthropic values. Older donors often focus on leaving a legacy through structured bequests and estate gifts. On the other hand, younger generations, particularly those inheriting wealth during this period, are more interested in achieving measurable outcomes.

One area gaining traction is impact investing, which combines financial returns with social or environmental benefits. While only 3% of donors currently use this strategy, 15% expect to adopt it by 2026.

"Impact investing... was deployed infrequently among respondents to our survey (about three per cent), but the strategy was cited by 15 per cent of donors as one they expected to use this year." - Joe Chidley, Managing Editor, Canadian Family Offices

Family Dynamics and Generational Attitudes in Wealth and Giving

How Different Generations Manage Wealth and Philanthropic Activities

Generational differences play a big role in how families approach philanthropy. Baby Boomers often focus on creating a legacy through traditional giving methods. In contrast, Millennials and Gen Z lean towards supporting causes that align with their personal values, favouring initiatives with measurable social impact. In Canada, by 2026, social justice and international humanitarian aid have become increasingly important to high-net-worth families, while health and medical research continues to be a top priority. Interestingly, environmental causes have seen a drop in urgency among surveyed donors. Younger generations, while still aware of environmental concerns, are channelling their efforts into what they see as more pressing issues. These generational shifts highlight the need for effective family governance to ensure smooth wealth transfer and unified philanthropic strategies.

Family Communication and Governance

Different values across generations can make wealth transfer discussions challenging. Aligning family members on shared goals is often one of the toughest hurdles. Discovery meetings, led by advisors, can help uncover and address disagreements early on, preventing potential conflicts down the road. External facilitators are also invaluable in navigating sensitive topics like eldercare responsibilities or debates over which causes to fund. Their involvement helps reduce emotional tension and ensures discussions remain constructive.

"Unrestricted giving - donations made without specific limitations to how the funds will be used - has been called out among some philanthropy advocates as a way to enhance the efficiency and impact of giving." - Joe Chidley, Managing Editor, Canadian Family Offices

Unrestricted giving, which allows recipient organisations to allocate funds as needed, demands a high level of trust and alignment within the family. It also requires confidence in the organisations receiving the donations. Building strong communication frameworks well before wealth transfer is crucial to achieving this trust. When families successfully bridge generational differences, they can create a more cohesive approach to wealth and philanthropy, strengthening their overall planning efforts.

Planning Considerations for Philanthropy in Canada

Tax-Efficient Ways to Give

When it comes to charitable giving, how you give can be just as impactful as how much. Structuring your donations with tax efficiency in mind can play a significant role in transferring wealth across generations, while also maximizing the benefits for both you and the causes you support.

One standout approach is donating publicly traded securities directly to a charity instead of selling them first. Thanks to the Income Tax Act (ITA) s. 38(a.1), you benefit from a 0% capital gains inclusion rate. This means you avoid paying capital gains tax on the appreciated value of the securities and still receive a donation receipt for their full fair market value. As Nizam Shajani, CPA, explains:

"Under ITA s.38(a.1), the capital gain on donated publicly traded securities is exempt... Few provisions in Canadian tax law are this elegant."

Another effective strategy involves registered assets like RRSPs and RRIFs. By naming a charity or Donor Advised Fund (DAF) as a direct beneficiary, you can bypass probate fees and reduce the terminal tax on your estate.

For families with fluctuating income, a DAF can provide flexibility. You can claim an immediate tax receipt during a high-income year while spreading out donations to charities over time. With new Alternative Minimum Tax (AMT) rules coming into effect in 2026, advisors are already running detailed projections to ensure large charitable gifts don't inadvertently trigger AMT exposure.

| Strategy | Key Tax Benefit | Ideal For |

|---|---|---|

| Appreciated Securities | 0% capital gains + full FMV receipt | Investment portfolios with unrealised gains |

| RRSP/RRIF Beneficiary Designation | Offsets terminal income tax; avoids probate | Reducing estate tax burden |

| Donor Advised Fund (DAF) | Immediate receipt; deferred granting | High-income years; multi-year giving plans |

| Ecological or Cultural Gifts | 0% capital gains; no net income limit | High-value land or heritage property |

Aligning Giving Plans with Family Values

Tax efficiency is important, but philanthropy is most meaningful when it reflects your family's core values. To start, identify the causes that resonate with your family - whether it’s education, healthcare, or community development. From there, choose a giving structure that aligns with your goals. For example, DAFs offer simplicity and tax benefits, while private foundations provide greater control and a lasting public legacy, albeit with higher administrative costs.

"Durable giving decisions begin with judgment, not tactics." - Shea Sanche, Founder, Insight Planning

Incorporating philanthropy into estate and succession planning, rather than treating it as a separate endeavour, can create continuity across generations. For family-owned businesses - which make up over 70% of small and mid-sized private companies in Canada - this might involve embedding charitable commitments directly into shareholder or trust agreements. A prime example of this approach is the bequest of all shares in a privately held business valued at $500 million to The Winnipeg Foundation - the largest individual gift ever made to a Canadian charity.

Careful internal planning lays the groundwork for seamless professional guidance.

Working with Canadian Wealth Experts

Philanthropy at the wealth transfer level is complex, requiring a blend of tax expertise, estate planning, and family governance. Often, it’s not the technical rules that cause problems but a lack of coordination among advisors.

"Technical rules rarely cause damage alone. Lack of coordination does." - Shea Sanche, CFP

To avoid such pitfalls, it’s essential to work with professionals who understand both the financial and relational aspects of giving. This means ensuring your wealth manager, estate lawyer, and tax advisor collaborate on asset sequencing, document alignment, and timing. For families balancing business succession with charitable goals, integrated advice is even more critical.

Philanthropy as a Strategy: Optimizing charitable giving and legacy building for HNW Canadians

Conclusion: Key Takeaways

Canada is already experiencing a significant wealth transfer. Since 2016, seniors have outnumbered children, emphasizing the growing importance of legacy planning.

The numbers tell an interesting story: only 33% of Canadians who received an inheritance knew about it in advance. This disconnect between intention and communication often leads to missed opportunities to preserve and pass on values. Starting these discussions early, while the wealth-holder can provide context and share their vision, can make all the difference.

Philanthropy is more than just financial - it’s deeply tied to family values. Leanne Kaufman, President and CEO of RBC Royal Trust, highlights this beautifully:

"The act of giving is often a statement of one's values. But as we all know, what's important to you or me can be vastly different from those around us, including our closest family members."

Engaging the next generation in giving decisions - whether through a Donor Advised Fund, a family foundation, or simply selecting charities as a family - can strengthen both financial literacy and a shared sense of purpose. This collaborative approach helps align family values with professional guidance to ensure a legacy that lasts.

Effective legacy planning requires a team effort. Tax advisors, estate lawyers, and wealth managers each play a critical role. If you’re seeking local expertise tailored to your family’s needs, the Find Wealth Experts and Private Bankers in Canada directory provides a province-specific guide to connect you with the right professionals.

FAQs

When should my family start planning for a wealth transfer?

Planning for a wealth transfer is something that should start sooner rather than later. Take the time to have open conversations about your family’s values, long-term goals, and overall structure. By addressing these topics early and preparing for unforeseen circumstances, you can help create a smoother process that benefits everyone involved.

Should we use a DAF, a foundation, or direct donations?

When deciding how to approach charitable giving, it’s essential to weigh your goals, tax benefits, and how much time and effort you can dedicate to managing the process.

- Donor-advised funds (DAFs) are a popular choice for their flexibility and streamlined management. They allow you to make contributions, receive immediate tax benefits, and recommend grants to charities over time.

- Foundations give you more control over how funds are distributed and used. However, they come with more complex setup requirements and ongoing administrative responsibilities, making them better suited for those prepared to invest significant time and resources.

- Direct donations are straightforward and deliver immediate support to causes you care about. This option works well for those seeking simplicity and instant results.

If you're unsure which route aligns best with your goals, a wealth advisor can provide tailored guidance to shape your philanthropic strategy.

What’s the most tax-efficient way to donate in Canada?

When it comes to donating in Canada, one of the smartest ways is to give appreciated securities directly to a registered charity. Why? Because this not only eliminates capital gains tax but also qualifies you for a charitable donation tax credit - a win-win for both you and the cause you care about.

Another option is donating assets from your RRSP or RRIF into a Donor Advised Fund (DAF). This approach can help offset taxes, sidestep probate fees, and align perfectly with your philanthropic plans. It’s a practical way to make your giving more impactful while managing your financial goals.