Estate settlement in Canada involves managing and distributing a deceased person’s assets, paying debts, and filing taxes. Executors (or liquidators in Quebec) oversee this process, which varies by province due to differences in laws and probate fees. Here’s what you need to know:

- Executor’s Role: Executors handle assets, settle debts, and manage taxes. In Quebec, this role is called a liquidator.

- Probate: Required to validate wills and authorize executors, except for some assets (e.g., joint accounts or designated beneficiaries). Costs differ by province, with Quebec and Manitoba charging no probate fees.

- Documents Needed: Includes the will, death certificate, financial records, and property deeds.

- Taxes: Executors must file a Final T1 Return and possibly a T3 Trust Return. A Tax Clearance Certificate from the CRA ensures all taxes are settled before distributing assets.

- Quebec Differences: Governed by the Civil Code, Quebec avoids probate for notarial wills and requires additional steps like family patrimony partition and public notices.

Key Tip: Always secure assets, notify financial institutions, and keep detailed records to avoid liability. Consulting professionals can simplify the process, and their fees are covered by the estate.

First Steps and Required Documents

Documents You Need to Gather

Start by collecting the key documents you'll need. Without them, banks, government offices, and courts won't process your requests.

| Document Category | Specific Items to Gather |

|---|---|

| Legal | Original will, codicils, marriage or divorce certificates |

| Identification | Deceased's SIN, birth certificate |

| Financial | Bank statements, investment records, credit card statements |

| Assets | Property deeds, vehicle registrations, appraisals for jewellery or art |

| Insurance | Life insurance policies, health and dental benefit details |

| Government | CPP/OAS records, tax returns for the past three years |

When it comes to death certificates, order multiple certified copies from the funeral home or your province's vital statistics office. Many institutions and agencies require originals, so having several ready will save time and hassle.

Once you've gathered everything, focus on the immediate administrative tasks.

Early Administrative Tasks

Start by locating the original will. Check the deceased's home, safety deposit box, or consult their lawyer or notary in Quebec. If the will is in a safety deposit box, you'll need the key, your ID, and a death certificate to access it.

Next, secure physical assets. Change locks and confirm that home and vehicle insurance policies are active. Letting insurance lapse, even briefly, can lead to major complications if anything happens before the estate is settled.

Notify banks and investment firms to freeze accounts, preventing unauthorized transactions. At the same time, cancel credit cards and recurring subscriptions to avoid fraud or unnecessary charges. Don’t forget to apply for the CPP death benefit as soon as possible; this requires a separate application and is often overlooked.

Keep a detailed record of all transactions, communications with beneficiaries, and expenses (like funeral costs). This log is critical for preparing the estate’s final accounts and protects the executor from potential liability.

"Without the Tax Clearance Certificate, distributions from the estate should not proceed." - Canada Revenue Agency

Staying organized, securing assets, and notifying the right parties early on will set the stage for smoother estate management later.

sbb-itb-e9c03dd

EP 11: The Canadian Guide to Estate Administration

Probate and Executor Authority

Canadian Provincial Probate Fees Compared

What Is Probate?

Probate is the legal process where a court confirms the validity of a will and grants the executor the authority to manage the deceased's estate. Essentially, it’s the court’s official approval that the will is legitimate. Without probate, institutions like banks, land registries, and insurance companies cannot verify the executor’s authority. Once granted, the executor (referred to as an estate trustee in Ontario) can access financial accounts, transfer property, and handle debts. Probate also offers the executor a layer of legal protection - if issues arise after a proper grant of probate, liability typically falls on the executor who misused their role, not on the institutions relying on the probate documentation.

"Probate is a procedure to ask the court to either: give a person the authority to act as the estate trustee... confirm the authority of a person named... and formally approve that the deceased's will is their valid last will." - Ontario.ca

When Is Probate Required?

Understanding when probate is necessary depends largely on the type of assets involved. Not all estates require probate; it’s usually determined by how the deceased held their assets.

Probate is generally needed in cases where the deceased owned real estate solely in their name, had bank or investment accounts without a joint owner, or when financial institutions demand court-confirmed authority before releasing funds. It’s also required when there’s no will or if the will’s validity is challenged.

Certain assets, however, can avoid probate entirely. For instance, jointly held properties, registered accounts with named beneficiaries, and life insurance policies with designated beneficiaries pass directly to the named individuals, bypassing the estate.

"The only asset that absolutely requires probate is an interest in land (this includes mineral rights) registered in the name of the deceased alone." - Saskatchewan Law Courts

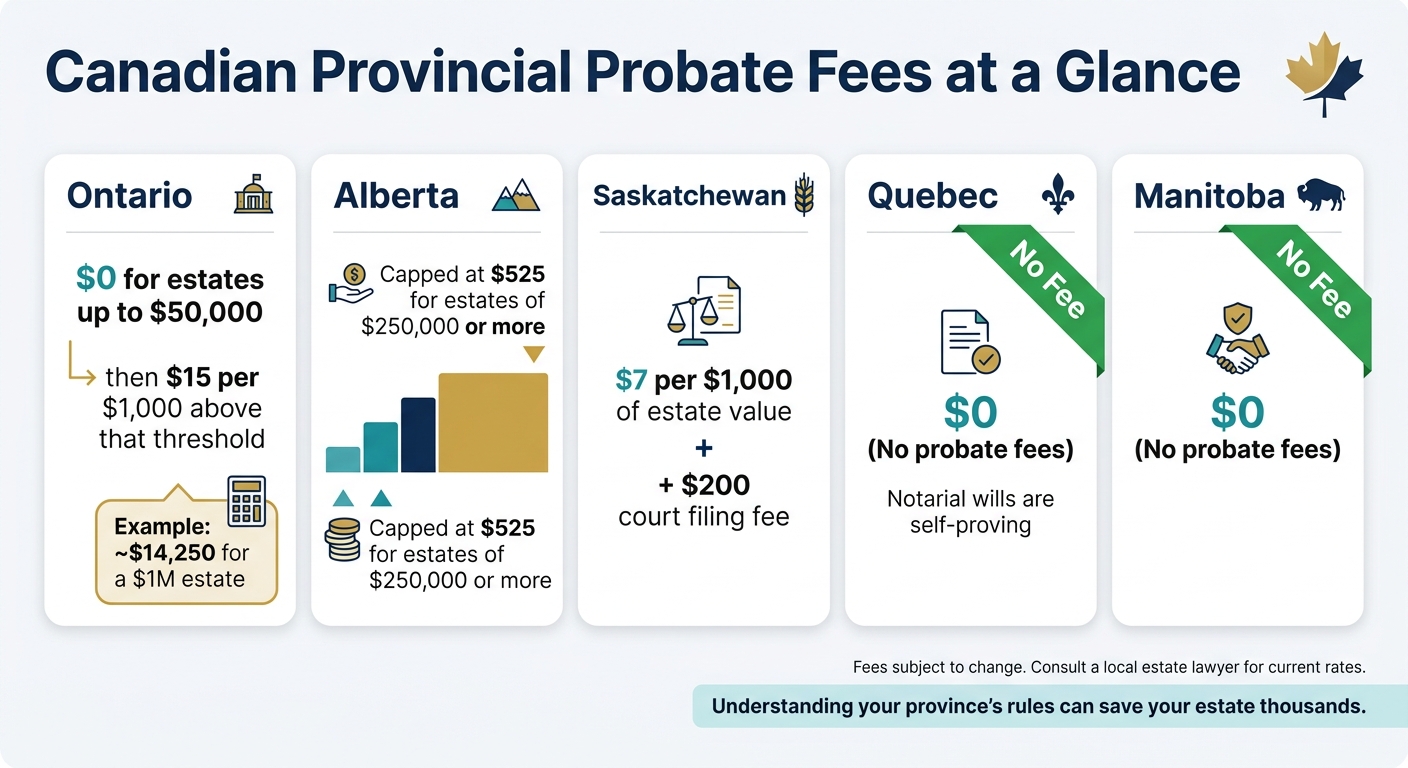

The timeline and cost of probate vary widely across provinces. While straightforward estates might be resolved within six weeks to six months, more complex cases - especially those involving businesses or foreign assets - can take 12–18 months or even longer. Below is a quick look at provincial probate fee structures:

| Province | Probate Fee Structure |

|---|---|

| Ontario | $0 for estates up to $50,000; $15 per $1,000 above that threshold |

| Alberta | Tiered flat fee, capped at $525 for estates of $250,000 or more |

| Saskatchewan | $7 per $1,000 of estate value, plus a $200 court filing fee |

| Quebec | No probate fees |

| Manitoba | No probate fees |

Before submitting a probate application, it’s a good idea to check with the deceased’s bank or credit union. Some institutions may release smaller account balances without requiring formal probate. These provincial differences and exceptions are key to navigating the next steps in settling an estate.

Assets, Debts, and Taxes During Estate Settlement

How to Inventory Assets and Liabilities

Once probate is complete, the executor's next job is to create a detailed inventory of everything the estate owns and owes. This includes assets like bank accounts, real estate, investments, vehicles, business interests, and even digital assets such as cryptocurrency or NFTs.

For each asset, gather any relevant documentation - title deeds, investment certificates, annuity records, or account statements. It’s also a good idea to check provincial unclaimed property registers, as forgotten or dormant assets sometimes surface there. Keep in mind that some assets, such as jointly held properties, registered accounts with named beneficiaries, and life insurance policies, are excluded from the probate inventory because they pass directly to the named individuals.

On the liabilities side, list all outstanding debts, including mortgages, loans, credit card balances, taxes, and municipal charges. To ensure all creditors are accounted for, it’s common practice in many provinces to publish a formal Notice to Creditors in a local newspaper - typically once a week for two consecutive weeks. This protects the executor from personal liability. Debts must then be paid in a specific order: secured creditors first, followed by funeral and administration costs, CRA tax debts, and finally unsecured creditors.

One key point for families to understand is that in Canada, heirs do not inherit the deceased’s debts unless they co-signed or guaranteed the loan.

"Debts of the deceased must be paid before any of the gifts provided for in the will are paid or transferred to the beneficiary." - Government of Saskatchewan

A thorough record of both assets and liabilities is essential for accurate tax reporting.

Tax Obligations During Estate Settlement

After completing the estate inventory, the executor must handle all tax filings - a critical part of their responsibilities. The first step is to file a Final T1 Return, which covers income earned from January 1 to the date of death. The deadline for this return depends on when the person passed away: April 30 of the following year for deaths between January 1 and October 31, or six months after the date of death for deaths between November 1 and December 31. Missing these deadlines can result in a penalty of 5% of the balance owing, plus an additional 1% per month for up to 12 months.

If the estate generates income after the date of death - such as interest or dividends from investments - the executor may also need to file a T3 Trust Return. Late filing of a T3 can lead to penalties of $25 per day, with a minimum of $100 and a maximum of $2,500, even if no taxes are owed. Additionally, an optional Return for Rights or Things can be filed to account for items like uncashed vacation pay or commissions. This return can help reduce the estate’s overall tax burden by allowing for additional credits.

Before distributing any assets to beneficiaries, the executor must obtain a Tax Clearance Certificate from the Canada Revenue Agency (CRA). This certificate confirms that all taxes, interest, and penalties have been paid. Skipping this step can have serious consequences. For instance, in the 2019 Alberta case Muth Estate v. Liesch (2019 ABQB 922), an executor was held personally liable for $60,000 in unpaid taxes after distributing gifts to beneficiaries without first securing a clearance certificate. This happened despite the executor receiving incorrect advice from two separate accountants.

"If the assets are distributed before obtaining a clearance certificate and amounts are owing to the CRA, the legal representative is personally liable for the debt, up to the value of the assets distributed." - Canada Revenue Agency

Distributing the Estate and Closing the File

How and When to Distribute Assets

After settling all debts and obtaining a Tax Clearance Certificate, the executor can begin distributing the estate's remaining assets. The distribution method varies depending on the type of asset. For example, real property is typically transferred by updating the title, investments are often converted into cash, and personal belongings are distributed as outlined in the will or according to intestacy laws if no will exists.

It's wise to hold back a portion of the estate as a residual fund to cover any unexpected liabilities until the Canada Revenue Agency (CRA) officially closes the file. Keeping beneficiaries in the loop regarding timelines and next steps helps prevent misunderstandings or disputes. Additionally, maintaining detailed records during this phase simplifies the preparation of final accounts. By handling distribution in stages, the executor ensures everything is done transparently and efficiently.

Final Accounts and Formal Closure

Once assets have been distributed, the executor's next step is to wrap up the estate’s financial records. This involves preparing a final account, which outlines all assets collected, debts settled, expenses paid, and the amounts distributed to beneficiaries. Sharing this document with beneficiaries allows them to review the administration process, ensuring everyone is on the same page and helping to avoid future conflicts.

To secure the Tax Clearance Certificate (issued on Form TX21), the executor must submit Form TX19 to the CRA. This includes the will, probate documents, a detailed list of assets, the names and SINs of beneficiaries, and Form AUT-01 if professionals are representing the estate. While the CRA usually acknowledges receipt within 45 days, the full review process may take up to 120 days.

"The estate trustee or executor becomes personally liable for any unpaid taxes or other amounts owed by the deceased or the estate, up to the value of the assets distributed [if a clearance certificate is not obtained]." - David J. Rotfleisch, Canadian Tax Lawyer

Throughout this process, it’s crucial for the executor to document all transactions and communications. This not only provides protection for the executor but also ensures transparency for everyone involved in the estate.

Estate Settlement Rules Specific to Quebec

How Civil Law Shapes Estate Settlement in Quebec

Quebec stands apart from other provinces when it comes to estate settlement, thanks to its reliance on civil law rather than common law. Governed by the Civil Code, Quebec uses a different framework for managing estates. For instance, estates in Quebec are referred to as "successions", and the person responsible for managing them is called a "liquidator", not an executor or estate trustee.

One key difference is the requirement to partition the family patrimony before distributing any assets to heirs. This involves allocating 50% of the value of family residences, vehicles, and the growth on RRSPs or pensions accumulated during the marriage to the surviving spouse. Additionally, the matrimonial regime - whether it's a Partnership of Acquests or Separation of Property - must also be liquidated at this stage. Only after these steps can the liquidator proceed with distributing the remaining assets.

Quebec's approach to probate also sets it apart. A $2 million estate in Ontario might face probate fees of approximately $29,500, but in Quebec, notarial wills, which are used by about 70% of residents, avoid these fees entirely. Prepared by a notary, these wills are self-proving and enforceable immediately without requiring court validation. These distinctions highlight how Quebec's estate settlement process is tailored by its legal system.

Quebec-Specific Requirements

Beyond the broader differences, Quebec imposes additional formalities on the liquidator. For starters, the liquidator must complete a detailed inventory of assets and debts within six months of the death. Failing to do so could result in personal liability for the estate's debts.

The liquidator is also required to register their designation in the RDPRM (Register of Personal and Movable Real Rights) and publish a Notice of Closure of Inventory in both the RDPRM and a local newspaper. Once the estate is fully settled, a Notice of Closing of the Estate's Final Account must also be published in the RDPRM to officially close the file.

Another unique aspect is the need for tax clearance from both the Canada Revenue Agency (CRA) and Revenu Québec. This additional requirement can increase accounting fees, typically ranging from $500 to $1,500.

| Requirement | Quebec | Other Provinces |

|---|---|---|

| Probate for notarial wills | Not required | N/A (no equivalent) |

| Asset inventory | Mandatory within 6 months | Recommended, not codified |

| Public notices (RDPRM) | Required | Not required |

| Tax authorities | CRA + Revenu Québec | CRA only |

| Family patrimony partition | Mandatory before distribution | Not applicable |

Finding Wealth Experts and Private Bankers in Canada

Why Work with a Professional During Estate Settlement?

Settling an estate comes with a host of legal and financial challenges. Professionals play a crucial role in ensuring that all legal clearances are obtained before distributing assets. For instance, when someone passes away, their capital property is considered sold at fair market value, which can lead to substantial capital gains taxes. Experts can also assist with filing an optional Rights or Things return to help reduce the tax burden associated with these gains.

Managing estate funds responsibly is another key aspect. Under Ontario's Trustee Act, executors are required to invest estate assets prudently. A financial advisor can guide executors in reallocating funds into suitable short-term investments like Guaranteed Investment Certificates (GICs) or high-interest savings accounts. These steps highlight the importance of having professional support throughout the estate settlement process.

"The executors who run into serious trouble are the ones who try to shortcut the process: paying beneficiaries before CRA clearance, investing estate cash carelessly, or missing tax filing deadlines." - LifeMoney.ca

Having a professional on board can help avoid these pitfalls. Additionally, fees for financial advisors, accountants, and lawyers are considered legitimate estate expenses. This means they are paid from the estate’s assets, not out of the executor's pocket.

How Find Wealth Experts and Private Bankers in Canada Can Help

The Find Wealth Experts and Private Bankers in Canada directory is a valuable resource for locating private banking professionals and wealth management experts across the country. Whether you're an executor in British Columbia managing real estate in multiple provinces or a liquidator in Quebec dealing with Revenu Québec requirements, this platform connects you with local experts equipped to handle your specific needs.

The directory is free to use and serves as a convenient starting point. Once you’ve identified your requirements, you can connect with advisors who specialize in areas like tax filings, investment strategies, and trust services.

Key Takeaways on Estate Settlement in Canada

Estate settlement in Canada is no small task - it can take anywhere from 12 to 24 months and involves navigating legal, tax, and administrative hurdles. Even the most diligent executors can find themselves overwhelmed by the process.

One crucial step is obtaining a CRA Clearance Certificate (Form TX19) before distributing any assets. This certificate protects the executor from personal liability by confirming that all taxes owed by the estate have been paid. Keep in mind that the Canada Revenue Agency (CRA) usually takes 4 to 6 months to issue this certificate after all returns are filed and taxes settled. Be sure to factor this timeline into your planning.

Another key consideration is probate fees, which vary significantly across provinces. For example:

- Ontario charges approximately $14,250 for a $1 million estate.

- Alberta caps probate fees at around $525.

- Manitoba doesn’t charge probate fees at all.

Understanding your province’s rules is essential. Additionally, proactive estate planning can reduce both time and costs. By naming beneficiaries on RRSPs, TFSAs, and life insurance policies, you can bypass probate for these assets. Similarly, jointly held assets with the right of survivorship transfer directly to the surviving owner, avoiding the estate process entirely.

"Your role in settling an estate is more than a legal obligation - it is an opportunity to honour the legacy of the deceased." - Eirene.ca

Finally, engaging professionals like an estate lawyer and tax accountant early in the process is a wise move. Their expertise can help you avoid costly mistakes, and their fees are typically covered by the estate.

FAQs

How do I know if probate is needed for this estate?

Probate is typically necessary when an estate contains assets that are solely in the deceased’s name - like real estate or investments. It serves to confirm the will’s validity, grants the executor the legal authority to act, and ensures that any outstanding debts are addressed. Since requirements can vary, it’s important to review the specific regulations in your province.

When can I safely pay beneficiaries without personal liability?

Once you’ve obtained a CRA Clearance Certificate and confirmed that all estate debts and taxes are fully paid, you can safely distribute funds to the beneficiaries. This step ensures you’re protected from any personal liability in your role as an executor.

What makes estate settlement different in Quebec?

In Quebec, estate settlement takes a slightly different turn compared to other provinces. Here, the individual responsible for managing the process is referred to as a liquidator. Their role is clearly outlined in the Civil Code of Québec. Key responsibilities include preparing a detailed inventory of the deceased's property, ensuring all debts are paid, and distributing the remaining assets to the rightful heirs. The process is governed by a set of legal steps that are unique to Quebec's legal framework.