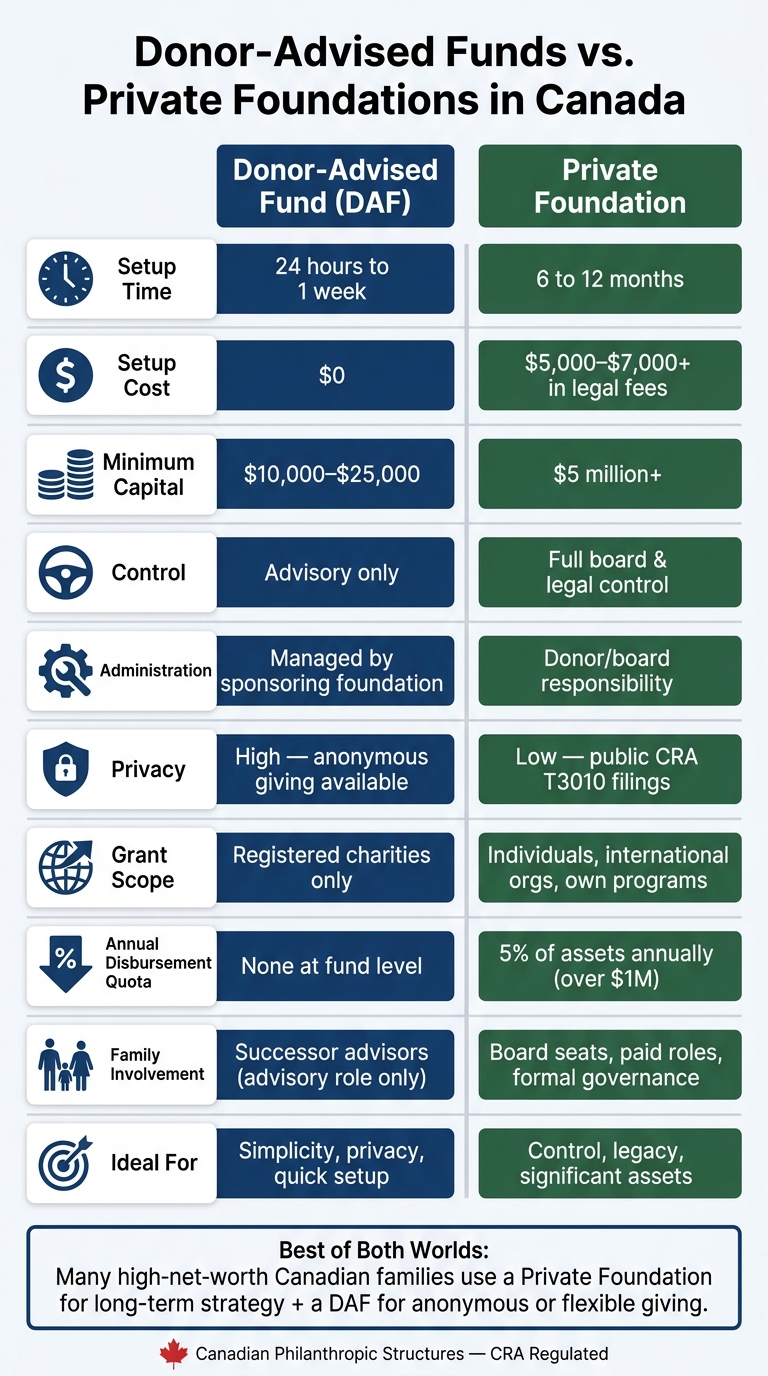

When deciding how to manage charitable giving in Canada, Donor-Advised Funds (DAFs) and Private Foundations are two popular options. Both allow you to support causes you care about while offering tax benefits, but they differ in control, costs, and complexity. Here's a quick breakdown:

- DAFs: Quick to set up (24 hours), lower cost, and managed by a sponsoring foundation. You recommend grants, but the foundation has final control. Ideal for donors seeking simplicity and privacy.

- Private Foundations: Greater control over grants and investments, but require significant time, effort, and financial resources to establish and manage. Transparent reporting is mandatory, and they suit donors with $5M+ in assets aiming for long-term family involvement.

Quick Comparison

| Feature | Donor-Advised Fund (DAF) | Private Foundation |

|---|---|---|

| Setup Time | 24 hours to 1 week | 6 to 12 months |

| Setup Cost | $0 | $5,000–$7,000+ in legal fees |

| Minimum Capital | $10,000–$25,000 | $5 million+ |

| Control | Advisory only | Full control |

| Administration | Managed by sponsor | Donor/board responsibility |

| Privacy | High (anonymous giving) | Low (public CRA filings) |

| Grant Scope | Registered charities only | Individuals, international orgs |

| Family Involvement | Successor advisors | Board seats, paid roles |

DAFs are best for simplicity and privacy, while Private Foundations offer control and legacy-building for those with significant resources. Choose based on your goals, financial capacity, and desired involvement.

Donor-Advised Funds vs. Private Foundations in Canada: Side-by-Side Comparison

Structure and Governance: How Each Option Works

Donor-Advised Funds: How They Are Managed

A donor-advised fund (DAF) functions as a charitable account within a sponsoring public foundation, such as Canada Gives or the Jewish Community Foundation (JCF) Montreal. Donors in the region often work with private bankers in Quebec to coordinate these large charitable contributions. While the sponsoring foundation legally owns the assets you contribute, you, as the donor, play an advisory role. Typically, your recommendations for grants are followed, but the final say lies with the sponsoring foundation's board. As Bana Khoury from Northwood Family Office explains:

"The sponsoring foundation retains legal ownership of the assets and final authority over grant approvals. While donor recommendations are nearly always followed, ultimate control is more limited than with a private foundation."

The administrative responsibilities, including CRA reporting, issuing tax receipts, managing investments, and ensuring compliance, are handled entirely by the sponsoring foundation. This setup allows you to focus on the act of giving without dealing with the operational complexities.

Private Foundations: Control and Autonomy

Private foundations, on the other hand, offer complete control over their operations. Unlike the advisory nature of a DAF, a private foundation is an independent legal entity - either a corporation or a trust - with its own CRA registration number. As the founder, you appoint a board of directors or trustees to oversee all aspects, including investments, grant approvals, policies, and the overall direction of the foundation. However, this level of control comes with significant responsibilities.

Managing a private foundation requires a hands-on approach. The board must hold regular meetings, document minutes, establish bylaws, issue tax receipts, and file an annual T3010 return with the CRA. Additionally, private foundations can hire their own staff and even operate charitable programmes directly. David Ohayon, Philanthropic Advisor at JCF Montreal, highlights this balance between autonomy and responsibility:

"Private foundations require their own boards of directors, who are responsible for governance, grant approvals, and strategic direction. While this offers autonomy, it also demands a high level of involvement, time, and expertise."

One key consideration is the potential for shifts in board composition over time. This can pose risks to the foundation’s original mission, as Ohayon points out:

"Board of Directors change over time and have full power to change the foundation's orientation, granting policies or even its name."

Comparison Table: Structure and Governance

Here’s a side-by-side look at the structural and governance differences between donor-advised funds and private foundations:

| Feature | Donor-Advised Fund (DAF) | Private Foundation |

|---|---|---|

| Legal Status | Account within a public foundation | Independent legal entity (Trust or Corporation) |

| CRA Registration | Uses sponsor's registration number | Must obtain its own registration number |

| Governance | Managed by the sponsoring foundation's board | Governed by a donor-appointed board of directors |

| Donor Role | Advisory (recommendations only) | Full control (decision-making authority) |

| Staffing | Provided by the sponsoring foundation | Donor can hire staff |

| Setup Time | As little as 24 hours | 6 to 12 months for CRA approval |

| Administrative Burden | Handled by the sponsor | Managed by the donor or outsourced |

sbb-itb-e9c03dd

Costs, Administration, and Compliance

Costs of Running a DAF

Setting up a Donor-Advised Fund (DAF) in Canada is both quick and free. Most sponsoring foundations don’t charge any setup fees, and the process is typically completed within 24 hours to a week. Once the fund is active, donors pay annual fees ranging from 0.75% to 2% of the fund's value, along with standard investment management fees. These fees cover essential services like processing grants, issuing tax receipts, and ensuring compliance with Canada Revenue Agency (CRA) requirements.

The Canada Gives team emphasizes the simplicity of the process:

"A Donor Advised fund at Canada Gives takes less than a day and costs nothing to set up, while we handle all CRA reporting, grant processing and management of all legal obligations."

By comparison, setting up a private foundation is more involved and costly.

Costs of Running a Private Foundation

Private foundations come with significantly higher setup and ongoing costs. Legal fees for incorporation and CRA registration typically range from $5,000 to $7,000. The entire process, which includes drafting bylaws and obtaining charitable status, can take anywhere from six months to a year.

Once the foundation is operational, recurring expenses like accounting, tax preparation, legal services, insurance, and possibly staff salaries add to the financial burden. Because of these costs, experts recommend a minimum asset base of $5 million to make a private foundation a viable option.

Reporting and Compliance Requirements

Compliance obligations differ significantly between DAFs and private foundations. With DAFs, the sponsoring foundation takes care of all CRA reporting, allowing donors to avoid direct filing responsibilities. This arrangement ensures that individual fund details remain private, as only aggregate activity is reported.

On the other hand, private foundations must adhere to more stringent requirements. They are required to hold regular board meetings, document minutes, and file an annual T3010 Registered Charity Information Return with the CRA. This information is publicly accessible, meaning private foundations are subject to full transparency. As David Ohayon of JCF Montreal explains:

"Despite their name, private foundations are not private and completely open to public scrutiny."

Additionally, private foundations must meet a mandatory annual disbursement quota of 5% of their assets (for assets over $1 million). DAFs, however, do not impose such quotas at the individual fund level.

Comparison Table: Costs and Administration

| Feature | Donor-Advised Fund (DAF) | Private Foundation |

|---|---|---|

| Setup Cost | $0 | $5,000–$7,000+ in legal fees |

| Setup Time | 24 hours to 1 week | 6 to 12 months |

| Annual Fees | 0.75%–2% of assets | Variable (legal, audit, staff, insurance) |

| CRA Reporting | Handled by the sponsoring foundation | Annual T3010 filing required |

| Disbursement Quota | None at the individual fund level | 5% of assets annually (if over $1M) |

| Public Disclosure | Private; reported in aggregate | Fully public on the CRA website |

| Recommended Minimum | $10,000–$25,000 | $5 million |

Tax Benefits and Funding Options

Tax Treatment for DAF Contributions

Donor-Advised Funds (DAFs) and private foundations both offer an immediate tax receipt in the year you make your contribution, even if the funds are distributed to charities at a later date. This can be particularly helpful during years of high income or after a major liquidity event, like selling a business.

One standout benefit of DAFs is that donating appreciated securities allows you to bypass capital gains tax while still receiving a tax receipt at their market value. As highlighted by the Toronto Foundation:

"A DAF can also offer greater flexibility for estate tax planning. For example, shares of a holding company can be donated to a DAF, whereas this is typically restricted with private foundations."

DAFs also accept a broader range of assets. For instance, shares of a holding company can often be contributed without triggering the strict self-dealing rules that apply to private foundations. Additionally, unused donation credits can be carried forward for up to five years.

Tax Treatment for Private Foundation Contributions

Private foundations also provide immediate tax receipts and capital gains exemptions for donations of publicly traded securities. However, they come with stricter rules for certain asset types. For example, the "80/20 rule" limits a private foundation's ownership in any single corporation to 20%, a restriction that DAFs do not face. While contributions of real estate or private company shares are allowed, they require independent valuations and careful compliance measures.

In Canada, the federal charitable tax credit can be as high as 33% of the donation amount, and corporations can deduct charitable contributions against up to 75% of their net income. While both DAFs and private foundations offer these tax advantages, the key differences lie in the types of assets they accept and the ease with which donations can be processed. These distinctions play a significant role in shaping long-term giving strategies and operational costs.

Comparison Table: Tax Implications

| Donation Type | Donor-Advised Fund (DAF) | Private Foundation |

|---|---|---|

| Cash | Immediate tax receipt; flexible carry-forward up to 5 years | Immediate tax receipt; similar carry-forward rules |

| Publicly Traded Securities | 0% capital gains tax; tax receipt at fair market value | 0% capital gains tax; tax receipt at fair market value |

| Holding Company Shares | Generally accepted; avoids self-dealing rules | Typically restricted or subject to strict rules |

| Real Estate | Depends on the sponsoring foundation's capacity to accept | Possible, but requires independent valuation and compliance |

| Disbursement Requirement | No individual fund-level quota | Mandatory 3.5% (for assets ≤ $1M) or 5% (for assets > $1M) annually |

Donor-Advised Funds vs. Private Foundations | Ask the Experts Webinar

Flexibility, Privacy, and Long-Term Planning

When deciding between a Donor-Advised Fund (DAF) and a private foundation, it's essential to consider not just costs and structure but also how each option handles flexibility, privacy, and legacy planning.

Grant-Making and Investment Flexibility

One of the key differences between DAFs and private foundations lies in how they approach grant-making and investments. DAFs are quick and straightforward to set up, with the sponsoring charity taking care of all administrative responsibilities. However, donors only have advisory privileges - final decisions on grants and investments rest entirely with the sponsoring organisation.

Private foundations, on the other hand, grant donors full control. This means they can oversee investments, governance, and grant-making decisions. With this expanded authority, private foundations can do things DAFs cannot, such as awarding scholarships directly to individuals, making grants to international organisations, or even supporting certain for-profit ventures. However, setting up a private foundation is a more time-intensive process, requiring incorporation and registration as a charity.

As Steven Sommers, Philanthropic Solutions Area Manager at Regions Bank, explains:

"People choose private foundations when they want more responsibility and more control - over the assets, the investments, the governance and the long-term charitable strategy."

Privacy and Public Disclosure

Privacy is another area where DAFs and private foundations differ significantly. DAFs allow for anonymous giving, as only the name of the sponsoring organisation is disclosed, keeping donor identities confidential. By contrast, private foundations are subject to full public disclosure. In Canada, the CRA requires all charities, including private foundations, to file an annual T3010 return, which is publicly accessible. This includes details about grant amounts, grantees, and even officer salaries.

David Ohayon, Philanthropic Advisor at JCF Montreal, highlights this point:

"Despite the term 'private foundation', these structures are far from private. The CRA mandates that all Canadian charities including private foundations file an annual T3010 return... all of which is made publicly available."

For donors who value a public philanthropic identity, this transparency can be a benefit. However, those who prefer discretion may find the anonymity of a DAF more appealing.

Family Involvement and Legacy Planning

Family engagement and long-term legacy planning are also important factors to weigh. Both DAFs and private foundations can facilitate multi-generational giving, but they do so in different ways. With a DAF, donors can name successor advisors - typically family members - who can continue to recommend grants after the donor’s passing. This setup provides an accessible way for younger generations to get involved in philanthropy, though their role remains advisory and lacks formal authority.

Private foundations, by contrast, offer a deeper level of involvement. Family members can serve on the board and even receive compensation for essential services. This makes private foundations ideal for families looking to establish a lasting, branded institution with clear governance structures that span generations. Many high-net-worth families in Canada use a combination of both: a private foundation for strategic, long-term initiatives and a DAF for anonymous giving or to meet annual disbursement requirements when specific grantees haven’t been identified.

Comparison Table: Flexibility and Legacy Planning

| Feature | Donor-Advised Fund (DAF) | Private Foundation |

|---|---|---|

| Grant Recipients | Primarily registered public charities | Individuals, international organisations, and for-profits |

| Donor Privacy | Full anonymity is available | Public record via CRA T3010 filings |

| Family Involvement | Successor advisors can be named; advisory role only | Board seats and compensated roles |

| Institutional Permanence | Limited; depends on successor advisors | Built for perpetuity and strong branding |

| Legal Control | Retained by the sponsoring organisation | Managed by a donor-controlled board |

These differences highlight how donors can align their philanthropic approach with their priorities, whether that's ease and discretion through a DAF or control and legacy-building through a private foundation.

Choosing Between a DAF and a Private Foundation

Key Factors to Consider

When deciding between a donor-advised fund (DAF) and a private foundation, it's essential to weigh factors like control, complexity, and the financial resources you have available. Each option offers distinct advantages depending on your goals and situation.

A DAF is a great choice if you're looking to start giving quickly, minimize costs, and avoid ongoing administrative headaches. With a DAF, setup is fast, fees are minimal, and the sponsoring organization takes care of CRA reporting and compliance. For example, after a major liquidity event, such as selling a business, a DAF can immediately issue tax receipts, making it a practical solution for donors seeking efficiency.

On the other hand, a private foundation is better suited for donors with substantial assets - typically $5 million or more - who want greater control. A foundation allows for formal family governance and the ability to manage charitable programs, fund international organizations, or directly award scholarships. However, it comes with more administrative responsibilities and public disclosure requirements. If privacy is a concern, it's worth noting that DAFs offer complete anonymity, while private foundations must disclose financial details, grants, and board information through CRA T3010 filings.

How Wealth Experts Can Help

Philanthropic planning isn't just about giving back; it's also a key part of your broader wealth strategy. It intersects with estate planning, tax considerations, and long-term financial goals. A private banker or wealth advisor can help you navigate these options and determine which structure - DAF, private foundation, or even a hybrid approach - best fits your needs.

For Canadian donors, the Find Wealth Experts and Private Bankers in Canada directory is a helpful resource. It connects you with professionals specializing in philanthropic planning, DAFs, private foundations, and wealth management. The directory is organized by province, making it easy to find local expertise.

Final Comparison Table: DAFs vs. Private Foundations

| Feature | Donor-Advised Fund (DAF) | Private Foundation |

|---|---|---|

| Setup Time | Within 24 hours | 6 to 12 months |

| Setup Cost | Low to $0 | $5,000+ in legal fees |

| Minimum Capital | $5,000–$25,000 | Typically $5 million+ |

| Control | Advisory only | Full board and legal control |

| Administration | Handled by sponsoring organisation | Donor/board responsibility |

| Privacy | High - anonymous giving available | Low - public CRA T3010 filings |

| Grant Scope | Qualified donees (registered charities) | Individuals, international orgs, own programmes |

| Family Involvement | Successor advisors; advisory role only | Board seats, paid roles, formal governance |

| Ideal Donor Profile | Donors seeking simplicity, privacy, or immediate tax benefits | Donors with significant assets wanting control and legacy |

FAQs

Can I move money from a DAF to a private foundation later?

Transferring assets from a donor-advised fund (DAF) to a private foundation is generally not an option. DAFs are overseen by sponsoring organizations, and their rules typically block such transfers. While it is possible to convert a private foundation into a DAF, the reverse process is not allowed. For personalized advice on aligning your charitable goals with the right structure, it’s a good idea to consult with wealth advisors or private banking professionals.

How do I choose a sponsoring foundation for a DAF in Canada?

To find the right sponsoring foundation for a donor-advised fund (DAF) in Canada, take a close look at their policies, fees, and support services. It's also important to consider their track record in offering guidance, their ability to connect donors with charities, and how they assist with grant-making strategies. For example, community foundations often provide valuable local knowledge, while some sponsors focus on managing assets directly. If you're unsure where to start, consulting with wealth advisors or private bankers can help you identify a sponsor that matches your philanthropic objectives.

Which option is better after selling a business or other liquidity event?

A Donor-Advised Fund (DAF) can be a smart option after selling a business or going through a liquidity event. It offers immediate tax advantages in the same year and allows for flexible, long-term charitable giving. Compared to private foundations, DAFs are simpler and less expensive to establish. They also skip the heavy administrative and legal hurdles, letting you concentrate on your personal and financial priorities.