Art advisory services help wealthy Canadians manage art collections as part of their financial plans. These services include acquiring art, valuations, estate planning, lending against art, and practical tasks like insurance and storage. For high-net-worth individuals, art often represents 10–15% of their portfolio but is usually the least structured. Advisors provide expertise to protect, value, and integrate these assets into broader wealth strategies.

Key insights:

- Why it matters: Art is both an investment and a legacy. It has financial, emotional, and tax implications, especially for private bankers in Alberta and other provinces, where capital gains taxes can impact estate planning.

- Services offered: Acquisition, management, valuations, lending, estate planning, and philanthropy.

- Art as an investment: Art diversifies portfolios and offers long-term returns, but it’s illiquid and requires careful planning.

- Tax benefits in Canada: Donations of Certified Cultural Property can exempt capital gains taxes, and specific rules apply for estate planning and charitable giving.

- Choosing advisors: Look for expertise in Canadian tax laws, valuation standards, and conflict-free advice.

Art advisory is now a key service in private banking, helping collectors align their art with financial goals and preserve it for future generations.

Art Advisory in Canadian Private Banking: Key Stats & Comparisons

Core Components of Art Advisory in Private Banking

The Role of Art Advisors

Art advisors occupy a unique space where the art world meets wealth management. They collaborate with private bankers, estate lawyers, and family office professionals to ensure that art collections are treated with the same precision and care as other financial assets.

Their main role is to act as independent advocates for their clients. As Citi Private Bank explains:

"Our Art Advisors offer independent and objective advice, serving as a client's advocate to identify, research, evaluate, and negotiate acquisitions and sales of art on their behalf."

This independence is crucial. Since art advisors don’t take commissions from galleries or auction houses, their advice is always client-centred. They also work with a network of experts like appraisers, insurers, conservators, and shippers to provide a fully integrated approach. This ensures that every aspect of managing an art collection is aligned with the client's overall financial strategy.

Collection Strategy and Planning

A strong collection begins with a clear plan. Art advisors help clients define their goals, whether that means identifying areas of interest for new collectors or organizing collections that have grown without structure over the years. For some, this process is about discovering a passion, while for others, it’s about bringing order to an inherited or long-standing collection.

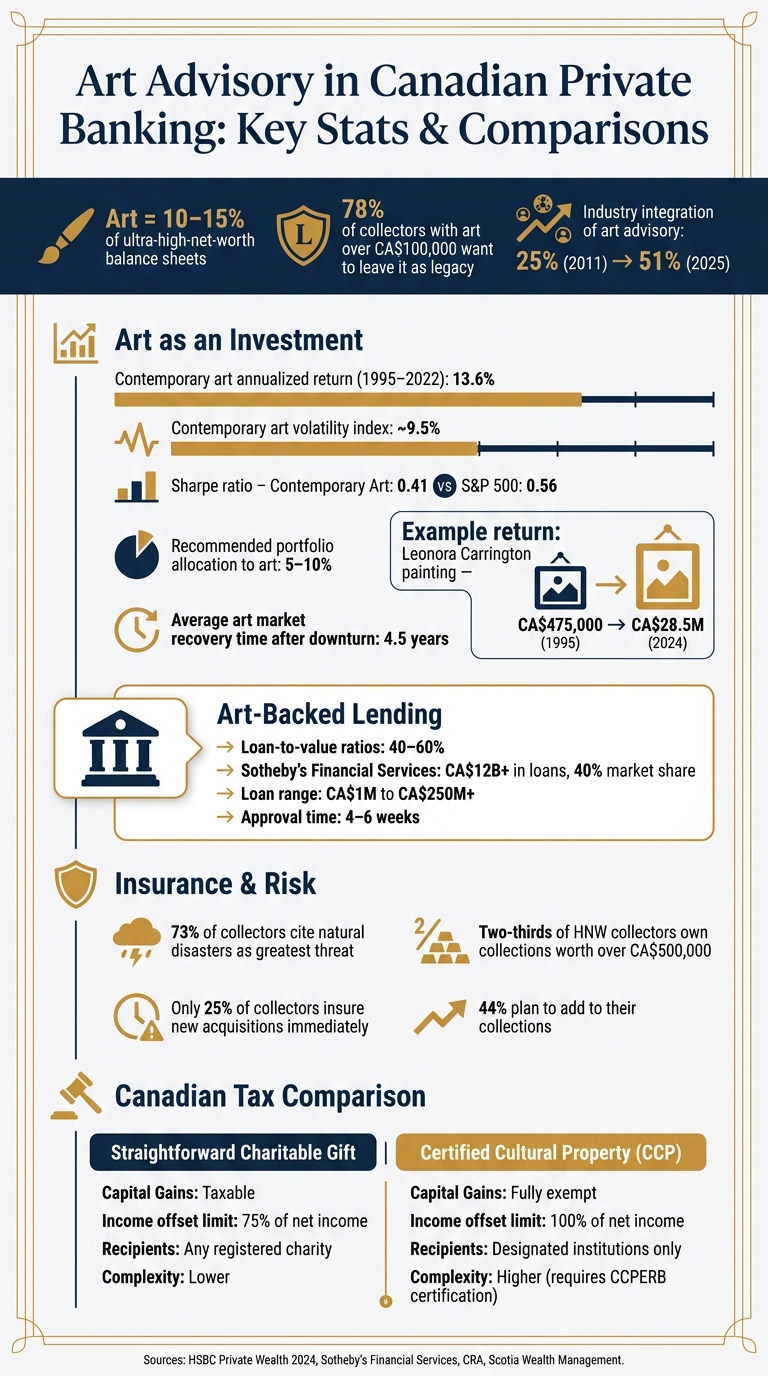

One tool that advisors often use is a Collection Charter. This document outlines the purpose of the collection, sets spending limits, assigns roles within the family, and establishes guidelines for storage and insurance. This is especially important for families who want to pass their collections on to future generations. In fact, 78% of collectors with art holdings over CA$100,000 are interested in leaving their collections as part of their legacy.

Elizabeth Thiessen, Head of Family Office Solutions at Bank of America Private Bank, highlights the broader impact of art on financial planning:

"A significant collection may affect a family's larger financial picture, from liquidity and credit to risk management and wealth transfer."

Advisors also focus on liquidity and estate planning, ensuring that the art collection aligns with the family’s long-term financial objectives. Accurate, up-to-date valuations are a key part of this process, helping to integrate art into overall wealth management.

Valuation, Appraisal, and Reporting

Once a collection strategy is in place, accurate valuations become essential. These valuations tie the art collection to the larger financial portfolio and support effective management. In Canada, valuations are typically conducted according to the Uniform Standards of Professional Appraisal Practice (USPAP). A common approach is the Sales Comparison Method, which uses at least three comparable sales to determine an object’s fair market value.

Valuations serve multiple purposes: ensuring proper insurance coverage, supporting estate planning, and integrating art into consolidated wealth reports. For families focused on passing wealth to the next generation, regular valuations are especially important. Many private banks now offer advanced reporting tools that provide clients with a unified view of their assets, including art. To maintain accuracy, regular internal or third-party valuations are highly recommended.

| Service Component | Activities |

|---|---|

| Acquisition | Developing strategies, conducting due diligence, negotiating prices, and researching provenance |

| Management | Tracking inventory, coordinating insurance, overseeing conservation, and managing logistics |

| Financial | Providing art-backed lending, conducting valuations, and integrating art into wealth reports |

| Disposition | Managing consignments, negotiating with auction houses, and advising on philanthropic gifting |

sbb-itb-e9c03dd

Art as an Investment in a Wealth Plan

Investment Characteristics of Fine Art

Art can play a fascinating role in a diversified wealth plan, offering both financial returns and a way to stabilize portfolios. One of art's standout qualities is its weak correlation with traditional assets, making it an effective tool for diversification. As HSBC Private Wealth highlighted in its 2024 Alternative Assets Briefing:

"Art offers counter-cyclical buffering when paired with gold and real estate - ideal for portfolio hedging with a long-term horizon of 7–10 years."

Contemporary art has shown impressive performance, delivering a 13.6% annualized return between 1995 and 2022, with a volatility index of about 9.5%. This makes it a strong performer, especially during inflationary periods, even outperforming the S&P 500 during such times. However, unlike stocks or bonds, selling a piece of art can take weeks or even months. This means art is better suited for long-term strategies rather than short-term liquidity needs.

Take the example of Leonora Carrington's Les Distractions de Dagobert. Purchased for CA$475,000 in 1995, it was resold by Sotheby's in 2024 for CA$28.5 million - a staggering return that outpaces most traditional investments over a comparable period.

These unique characteristics make art a compelling addition to portfolios, particularly for those focused on strategic planning and risk management.

Portfolio Construction and Risk Management

When incorporating art into a portfolio, wealth managers often suggest allocating 5–10% of the total value to this asset class. Diversifying across different artists, time periods, and types of media is critical to reducing concentration risk. That said, challenges like authenticity issues and shifting market trends require careful consideration. Historical data shows that, on average, it takes 4.5 years for the art market to recover after a downturn.

The Sharpe ratio for contemporary art, which measures risk-adjusted returns, stands at 0.41, compared to 0.56 for the S&P 500 from 1998 to 2023. While slightly lower, it still represents a reasonable balance of risk and reward.

Monica Heslington, Head of Goldman Sachs Family Office Art and Collectibles Strategy, emphasizes the importance of aligning art investments with personal identity and lifestyle:

"We don't primarily focus on questions of potential appreciation and future resale value. We determine why our clients want to start collecting and how it fits into their identity and lifestyle."

Institutional recognition can also significantly influence an artwork's value. For instance, after Lynette Yiadom-Boakye's 2020 retrospective at the Tate Modern, her market value surged. A painting that sold for CA$380,000 in 2019 reached CA$1.2 million by 2022 - a 300% increase. This phenomenon, often referred to as the "museum value multiplier", is a crucial factor for art advisors when crafting collection strategies.

Art-Backed Lending and Liquidity Options

While art is typically seen as a long-term investment, it can also serve as a source of liquidity through art-backed lending. These loans, which offer loan-to-value (LTV) ratios of 40–60%, provide a way to unlock the value of art collections without selling the assets. Loan approvals usually take four to six weeks to finalize.

Sotheby's Financial Services (SFS) is a major player in this space, having facilitated over CA$12 billion in loans and holding a 40% market share in the art lending sector. Their loans range from CA$1 million to more than CA$250 million, and the funds can be used for various purposes, including new acquisitions, estate tax payments, business expansions, or diversifying into other investments.

For example, in April 2026, a private food and beverage company owner used their art collection as collateral to secure a CA$30 million loan from SFS. The funds were used to complete a capital expansion project, with the expectation that the returns would exceed the cost of borrowing. In another scenario, a collector financed the "cashless acquisition" of a CA$50 million blue-chip artwork by borrowing against both the new piece and their existing collection.

Scott Milleisen, Global Head of Lending at Sotheby's Financial Services, sums up the appeal of this approach:

"Art-backed lending transforms that static value into strategic liquidity."

In Canada, this strategy offers an additional advantage: borrowing against a collection allows collectors to defer capital gains taxes that would be triggered by a sale. This keeps the asset - and its potential for future appreciation - secure on the balance sheet.

Managing an Art Collection: Practical Considerations

Risk Management and Insurance

Owning a high-value art collection comes with risks that standard homeowners' insurance often doesn't address. These policies frequently overlook issues like transit damage, accidental mishaps, or sudden market appreciation. To fill these gaps, specialized "all-risk" insurance policies are the go-to solution for protecting valuable collections. In fact, 73% of collectors view natural disasters as the greatest threat to their collections, and two-thirds of high-net-worth collectors own collections worth over CA$500,000.

When determining insurance coverage, Retail Replacement Value (RRV) is the preferred standard. Unlike Fair Market Value, RRV accounts for the full cost of replacing a piece quickly, including taxes, fees, and framing.

"Retail replacement value (RRV) should generally be relied upon because it accounts for the urgency of procuring a similar item in the event of a loss." - Noelle Valentino, Senior Fine Art & Collections Specialist, Chubb

One surprising statistic? Only 25% of collectors insure new acquisitions immediately, even though 44% plan to add to their collections. Regular reappraisals are crucial, especially for categories like ultra-contemporary art, where values can change rapidly.

"Collectors are passionate and knowledgeable, but insurance is often an afterthought. We help clients step back and look at how their collections are exposed at home, in storage, during transit or even while being worn." - Stefanie Capovilla, Vice President, Private Client Group, NFP

Beyond insurance, maintaining a collection involves proper conservation efforts and detailed documentation to safeguard its value.

Conservation, Logistics, and Documentation

Preserving and managing an art collection requires meticulous care and organization. Many private banks offer concierge services to connect clients with trusted networks for shipping, climate-controlled storage, and conservation services.

Thorough documentation is key. A detailed archive - including purchase agreements, provenance records, condition reports, high-resolution images, and shipping histories - serves multiple purposes. It satisfies insurance requirements, ensures legal ownership, supports appraisals, and simplifies estate planning. Using a Collection Management System (CMS) can help track pieces across multiple locations, reducing the risk of oversight.

International logistics add another layer of complexity. Moving artwork across borders involves navigating customs regulations, export restrictions, and tax implications. Collaborating with customs brokers and specialized insurers is essential, as is verifying provenance through stolen art registries and ownership history checks to avoid potential legal disputes.

"It's vital to bring a similar level of planning and strategy to art and collectibles as you do for other asset classes." - Elizabeth Thiessen, Head of Family Office Solutions, Bank of America Private Bank

With these practical measures in place, the next step is understanding the tax and legal considerations specific to Canada.

Tax, Legal, and Regulatory Considerations in Canada

In addition to physical and logistical protections, tax and legal planning play a critical role in managing art collections in Canada. The country's tax rules for art collections are intricate, making expert advice indispensable. For instance, selling or donating appreciated artwork typically results in a taxable capital gain, but there are strategies to reduce or eliminate this burden.

Donating art to a registered charity offers a tax receipt based on Fair Market Value (FMV), which can offset up to 75% of annual net income. For works designated as Certified Cultural Property (CCP) by the Canadian Cultural Property Export Review Board (CCPERB), the benefits are even better: capital gains are fully exempt from income tax, and the donation can offset up to 100% of net income. Here's a quick comparison:

| Aspect | Straightforward Charitable Gift | Certified Cultural Property (CCP) |

|---|---|---|

| Capital Gains Tax | Taxable (unless ACB exceeds FMV) | Exempt from income tax |

| Annual Income Limit | 75% of net income | 100% of net income |

| Eligible Recipients | Any registered charity or qualified donee | Designated institutions only |

| Complexity | Lower; direct transfer to charity | Higher; requires CCPERB certification |

Collectors should also be aware of the Deemed Fair Market Value rule. This rule prevents individuals from "flipping" art for tax benefits. If a piece is donated within three years of purchase - or within ten years if acquired with the intent to donate - the tax receipt is limited to the lesser of FMV or the original purchase price.

Estate planning introduces additional opportunities. In the year of death, the income limit for charitable tax credits rises to 100%, and unused credits can be carried back to the previous tax year. Donations through a Graduated Rate Estate (GRE) offer even more flexibility, allowing allocation across the year of donation, an earlier GRE year, or the deceased's final two tax returns, provided the gift is made within 60 months of death.

Consider this real-world example: In April 2026, Scotia Wealth Management helped a client who inherited a painting by a notable Canadian artist. The client had loaned the piece to an Ontario institution but later wanted to donate it after her husband's death. When the gallery declined due to collection limits, Scotia's advisors used the Aqueduct Foundation to sell the painting at auction and direct the proceeds to the gallery. This approach honoured the client's philanthropic goals while managing the estate's tax obligations effectively.

"These items have deep value, and not just financial value - cultural value, emotional value, they're often tied to identity, memory, and legacy." - Robyn McCallum, Director, Fine Art and Collectibles, Scotia Wealth Management

To ensure compliance with Canada Revenue Agency (CRA) rules, it's essential to engage an appraiser from a recognized professional association, such as the International Society of Appraisers or the Canadian Association of Professional Conservators. Legal counsel with expertise in Canadian art law should also review agreements related to sales, consignments, or loans to clarify responsibilities for insurance and potential damage during transport or exhibition.

How to Choose and Work with Art Advisors in Canada

Types of Art Advisory Providers

In Canada, art advisory services typically come from two main sources: private bank advisory desks and independent art advisors. Knowing the difference is key to finding the right fit for your needs.

Private bank advisory desks combine art advisory with broader financial services like estate planning, tax strategies, lending, and philanthropy. Erin Griffiths, Executive Vice President of Global Wealth Solutions at Scotia Wealth Management, explains:

"It was a natural evolution to begin offering this specialized service to clients who have meaningful collectibles, to both help manage and integrate them into their financial and estate planning."

On the other hand, independent art advisors specialize in areas such as Canadian Indigenous art or Old Masters. However, they usually don't offer the ability to incorporate art into financial or tax strategies. Some private banks take a hybrid approach, working with external experts to deliver tailored services. Société Générale Private Banking describes their model:

"Our aim is not to become an 'expert' in art. We have chosen to partner with external professionals... Selecting experts in this way allows us to provide bespoke services tailored to our clients' exact needs."

Choosing between these options depends on how closely your art collection ties into your overall financial picture. If your collection represents a significant part of your wealth, a private bank with integrated planning may be the better choice. This decision sets the stage for evaluating advisors' expertise and governance.

Assessing Expertise and Governance

When evaluating art advisors, look for credentials like membership in the International Society of Appraisers (ISA) and adherence to the Uniform Standards of Professional Appraisal Practice (USPAP), which are widely recognized across North America. Advisors with training from institutions like Sotheby's Institute of Art or Christie's Education, or those with experience in provenance research through programs like ARCA or HARP, bring additional depth to their expertise. For Canadian-specific needs, ensure the advisor understands the Canada Revenue Agency's (CRA) regulations and CCPERB standards for donations and tax planning. This level of knowledge is crucial for aligning your art collection with your financial goals.

Another important factor is avoiding conflicts of interest. Ask if the advisor is independent or affiliated with an auction house, as such ties could influence their advice on whether to sell, hold, or donate pieces from your collection.

Also, confirm that the advisor uses standardized documentation like Object ID and has access to trusted authentication resources, such as the Canadian Conservation Institute. As Liz Jacovino, Wealth Strategist at RBC Wealth Management–U.S., notes:

"The art world is fairly opaque with valuations and transactions, so having someone who understands the process of acquiring and caring for your collection can make it much easier."

Using Find Wealth Experts and Private Bankers in Canada

Finding private bankers with expertise in art can be a challenge. The directory "Find Wealth Experts and Private Bankers in Canada" simplifies this process. It organizes professionals by province, helping you locate advisors in your area who are skilled at managing fine art and other passion assets as part of a broader wealth strategy. This resource is invaluable for connecting with professionals who can integrate your art collection into your overall financial plan.

Conclusion

Key Takeaways

Art advisory has evolved into an essential part of wealth management, offering much more than just trading advice. It now intersects with estate planning, philanthropy, and risk management - making it particularly relevant for Canadian high-net-worth individuals who value a comprehensive approach to managing their assets.

As Robyn McCallum, Director of Fine Art and Collectibles at Scotia Wealth Management, explains:

"These items have deep value, and not just financial value - cultural value, emotional value, they're often tied to identity, memory, and legacy."

This perspective aligns with a significant industry trend: the integration of art advisory services by wealth managers has grown from 25% in 2011 to an expected 51% by 2025. Art and collectibles now account for an estimated 10–15% of an ultra-high-net-worth individual’s balance sheet, highlighting the need for professional guidance.

Expert art advisors bring numerous advantages: they integrate your collection into your overall financial strategy, facilitate art-backed lending to unlock liquidity without triggering capital gains, ensure proper documentation and insurance, and craft succession or philanthropic plans to preserve your legacy. These services demonstrate how professional oversight can elevate the management of art collections.

For Canadian collectors looking to align their art assets with a broader wealth strategy, resources like Find Wealth Experts and Private Bankers in Canada can help connect you with professionals who understand the unique needs of art collectors across the country.

Private Banks Boost Art Advisory

FAQs

How do I know if my art collection is big enough for private bank art advisory?

The scale of your art collection is less important than your broader financial situation. Many private banks provide art advisory services as an extra perk for high-net-worth individuals, usually catering to those with a net worth of $10 million to $25 million or more. These services can assist both newcomers to the art world and seasoned collectors with large portfolios. It's worth consulting with wealth advisors or private bankers to determine if these offerings fit your objectives.

What documents should I keep to protect my art’s value and support appraisals?

To protect your art's worth and simplify appraisals, it’s important to keep a detailed inventory of your collection. Key documents to organize include purchase records (like invoices and receipts), provenance information, title deeds, and any contracts or legal paperwork for inherited pieces. Additionally, maintain condition reports, exhibition histories, high-quality images, and updated appraisals for insurance purposes. These records not only support accurate valuations but also make it easier to align your collection with your overall financial plans.

When does donating art in Canada reduce or eliminate capital gains tax?

In Canada, donating art can offer tax benefits, particularly when it comes to capital gains. If you donate certified Canadian cultural property to designated institutions, a zero inclusion rate applies to any capital gains. For other types of property, this zero rate might also apply if the donation is made to a qualified donee and no advantage is received in return. Additionally, donors have the option to choose a gift value between the cost base and the fair market value, which can help in optimizing their tax situation.